Howe, Dalio, and the Stress Test

What if this war in Iran is about more than oil?

What if it is about credibility?

Over the last few months, across VMF Research, we have been building a large thesis. In VMF’s Strategic Asset Allocation, we argued that this Fourth Turning may culminate in a monetary reset. In VMF’s Security Selection, we pushed that thesis down to the company level and asked who gets paid as trust moves through new rails. And now, in March’s issue of Alpha Tier, “The Monetary Endgame,” we take the next step: we stress-test the framework itself against Ray Dalio’s Big Cycle and then force it through the hardest proving ground of all, a live geopolitical rupture.

This post unfolds as a three part series.

Part 1 is “Howe, Dalio, and the Stress Test”

Part 2 is “Toward the Reset”

Part 3 is “Hormuz and the Imperial Test”

That structure matters because what is at stake here is not just another market squall or another “oil up, stocks down” episode. In the issue itself, we argue that the war with Iran may be something much bigger: a live test of imperial credibility, monetary confidence, geopolitical power, and the fragility of the postwar order. In plain English, this may turn out to matter not only for markets, but for the United States, for Trump, and for the credibility of the system he is trying to command in the middle of a late-stage crisis era.

And yes, we go there.

Because one of the central historical analogies in this issue is the Suez Crisis of 1956. Not because history repeats neatly. And not because we are lazily declaring this “America’s Suez.” But because Suez captured something far more important than a failed military episode. It captured a moment when the world suddenly understood that an incumbent imperial power no longer had the freedom of action, coalition strength, or financial autonomy its reputation still implied. In the issue, we make the case that Hormuz may pose that kind of test for Washington now.

That is the frame for what follows.

This series is about the stress test. First of the theory. Then of the monetary order. And finally of the empire itself.

Here is Part 1.

By now, you are already familiar with the core hypothesis we have been developing across our entire product roster.

That roughly every 70 to 90 years (approximately the span of an average human life) during what Neil Howe and William Strauss describe as Fourth Turnings, the system is not merely stressed... it is renegotiated. Institutions lose credibility. Political cohesion weakens. Old assumptions break down. And, crucially for our purposes, the monetary order itself becomes vulnerable.

History does not repeat mechanically. But the pattern is difficult to ignore.

As you saw in this month’s issue of VMF’s Strategic Asset Allocation, the Revolutionary crisis gave us the collapse of the Continental and the birth of a more credible federal financial architecture. The Civil War suspended specie, introduced the Greenback, and accelerated the centralization of the monetary system. The Great Depression and World War II shattered the old gold constraint and gave rise to Bretton Woods and the dollar-centered global order.

Different contexts. Different mechanisms. Same underlying dynamic:

When the system breaks, the money changes with it.

That is the hypothesis.

But now comes the real question.

Is this pattern robust... or are we simply imposing narrative structure on a set of historical coincidences?

That objection should be taken seriously. After all, this is a small sample from which to infer what comes next. And even if we widened the lens (going back another two or three Fourth Turnings or casting a broader global net across other great crisis eras) we would still run into the same methodological problem. The parallels may remain striking, but the sample would still be limited, and limited samples are a fragile basis on which to draw definitive conclusions about recurring historical patterns.

It is precisely this fragility that we will now put to the test.

If this thesis is going to do more than sound elegant... if it is going to keep shaping how we allocate capital across our Model Portfolios... then it has to survive a more demanding test than historical analogy alone.

That is why we now turn to Ray Dalio

Dalio does not speak the language of generations.

He does not frame history in terms of archetypes, social moods, or civic cycles. Instead, he builds from something more mechanical... and, in many ways, more unforgiving: debt, money, power, and incentives.

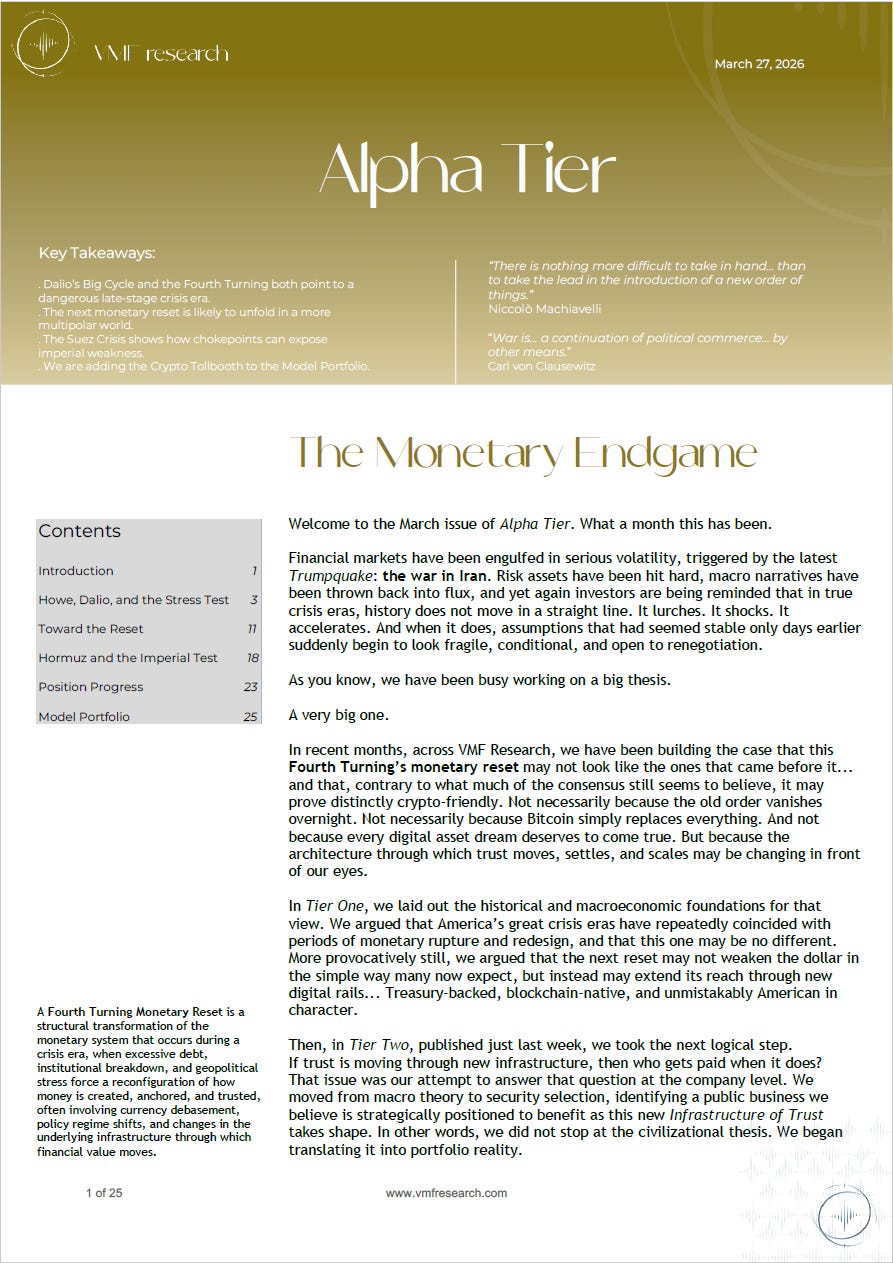

At the core of his work sits what he calls the Big Cycle, a multi-decade to multicentury process that governs the rise and decline of nations, empires, and monetary systems. In his more recent public framing, Dalio has described that Big Cycle as typically lasting about 80 years, give or take 25 years... in other words, roughly one lifetime. That timing alone makes the comparison with the Fourth Turning framework hard to ignore.

And within that Big Cycle, one dynamic stands above all others:

...the long-term debt cycle.

It begins, as these things often do, in strength.

A rising power establishes internal order, builds credible institutions, and develops a productive economy. Its currency becomes trusted. Its debt is considered safe. Capital flows toward it. Innovation flourishes. Military strength grows. The system reinforces itself.

Credit expands, but in the early stages, that expansion is productive. Debt finances growth. Growth supports income. Income supports debt service. The cycle feeds on itself in a virtuous loop.

Over time, however, the character of that debt changes.

What begins as productive borrowing gradually becomes consumptive borrowing. Debt grows faster than income. Financial assets inflate. Inequality widens. The gap between the real economy and the financial economy expands. And increasingly, stability itself becomes dependent on the continuation of credit growth.

This is where the system becomes fragile.

Because once debt levels reach a certain threshold, the rules change.

The system can no longer tolerate normal economic downturns without intervention. Central banks are forced to cut rates more aggressively. When rates approach zero, they are forced to print money. When money printing becomes politically sensitive, fiscal policy takes over. And gradually, the boundary between monetary and fiscal policy dissolves.

Dalio calls this phase monetization. In short, the system begins to sustain itself by creating money to support debt that cannot be supported organically.

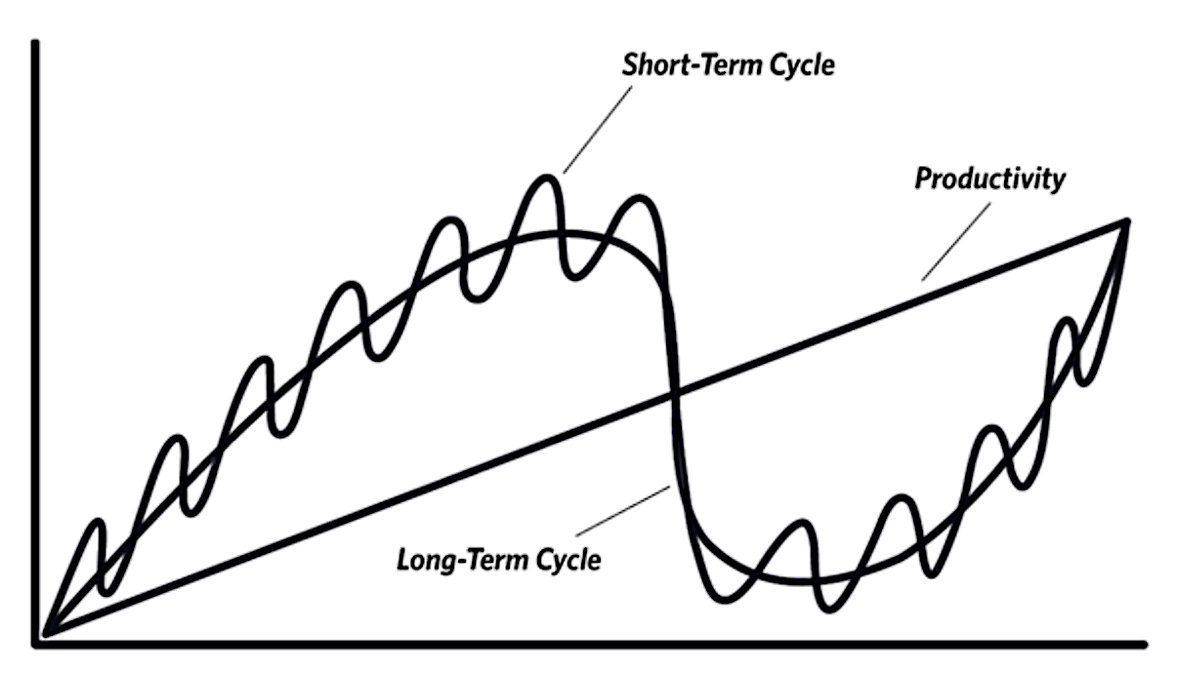

And importantly, Dalio does not treat this as some distant theoretical endpoint. In How Countries Go Broke, he writes that the monetary-policy regime in which central banks create money and buy debt to compensate for insufficient private demand began in 2008, the first time such a policy had been used since 1933, and he is explicit that these moves are “symptomatic of being in the late phase of the long-term debt cycle.”

By Dalio’s own framework, this cycle did not merely begin to look tired recently... it entered a recognizably late-stage phase nearly two decades ago.

His more recent public comments have pushed the point even further. Earlier this month, Dalio said that we are now in Stage 5 of the Big Cycle, the stage immediately preceding breakdown and great disorder.

Whether one agrees with that exact staging or not, the message is unmistakable: in Dalio’s view, we are no longer in the benign middle innings of the cycle. We are in its dangerous closing stretch.

That interpretation is also consistent with the harder cross-country indicators he has published. In his 2024 Great Powers Index, Dalio ranked the United States indebtedness position 33rd out of 35 countries, noting that, based on current debt levels and debt-service costs, the country has very little room to lever up further.

That is not how he describes a system early in its debt cycle... it is how he describes one already deep into its mature and vulnerable phase.

At this stage, the problem is no longer cyclical.

It is structural.

And this is where Dalio’s framework begins to intersect, in a very direct way, with the world we have been describing.

Because as debt burdens rise and monetary tools become exhausted, the system is pulled into a series of increasingly difficult trade-offs:

between inflation and growth,

between creditors and debtors,

between financial stability and political stability,

between internal cohesion and external projection of power.

These tensions do not remain confined to balance sheets.

They spill into politics.

This is where Dalio introduces the second critical dimension of his framework: The internal political cycle.

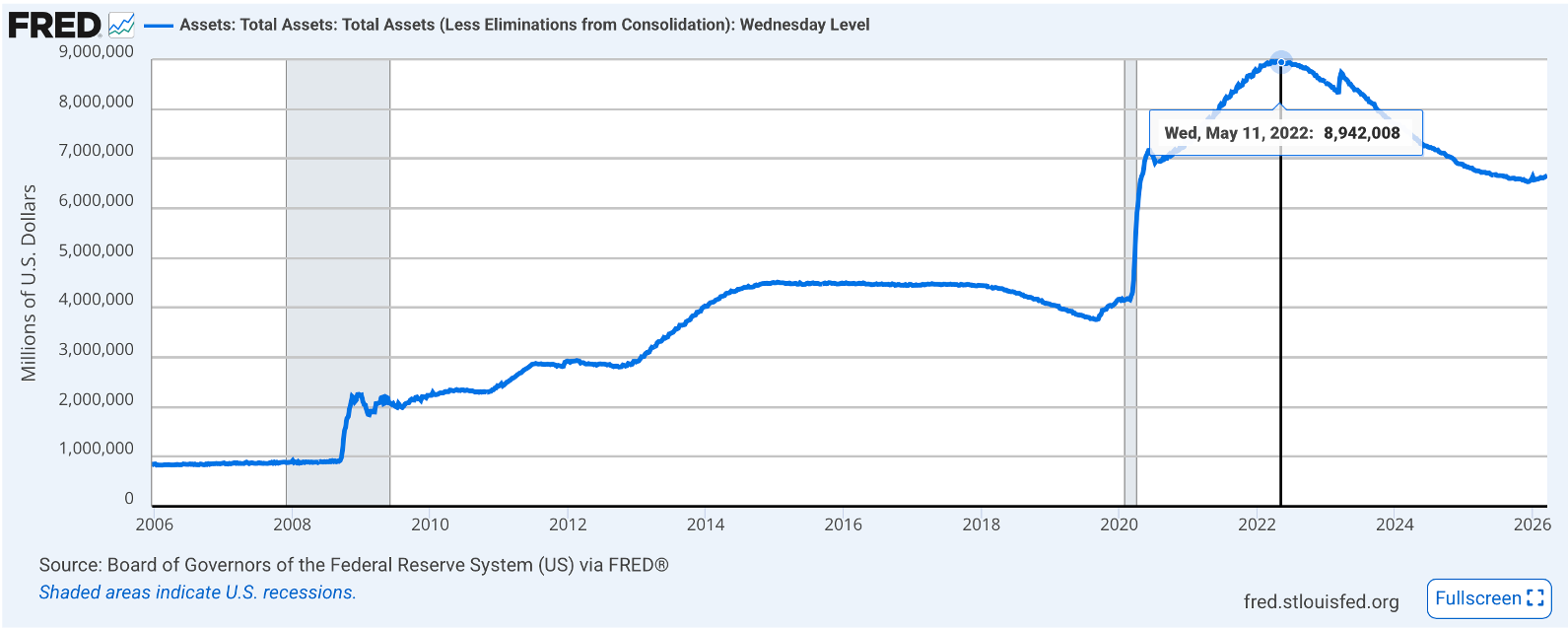

As wealth gaps widen and economic conditions become more uneven, societies tend to move from cooperation toward conflict. Political polarization increases.

Populism rises. Institutional trust erodes. And the willingness to accept painful adjustments declines. In other words, the system becomes less capable of reforming itself through orderly means.

Sound familiar?

It should.

Because this is precisely the terrain Fourth Turning theory describes, albeit through a different lens. Howe sees generational dynamics driving institutional breakdown.

Dalio sees financial imbalances and inequality driving political conflict.

Different starting points.

Same destination.

But Dalio does not stop there.

Because internal disorder rarely remains internal. As domestic pressures rise, countries become more sensitive to external threats and more willing to project power abroad. At the same time, rival powers (often with stronger balance sheets, rising productivity, and growing geopolitical ambition) begin to challenge the incumbent.

This is the third pillar of the Big Cycle: The external geopolitical cycle.

Historically, this is the phase where rising powers test declining ones, often over control of trade routes, resources, or spheres of influence. These confrontations do not always begin as full-scale wars. They often start as economic competition, trade disputes, regional conflicts, or coercive probes designed to test the resolve of the incumbent and the credibility of the order it oversees.

That is the broader context in which so many of today’s flashpoints need to be

understood...

The Russia-Ukraine war is not merely a brutal regional conflict. The long-running violence around Israel and Gaza is not merely a local tragedy. The renewed strategic focus on Venezuela, the pressure politics surrounding Greenland, and now the war with Iran all belong, in different ways and with different intensities, to a world in which geography, resources, chokepoints, spheres of influence, and alliance credibility are once again being contested more openly.

You might also like reading

They are not identical episodes, of course. But they are increasingly legible as symptoms of the same larger transition: a world order moving from presumed stability toward explicit tests of power.

And under the surface, something more fundamental is at stake: who sets the rules of the system, and whose money those rules are denominated in.

Because embedded within all of this is Dalio’s fourth and perhaps most important layer: The reserve currency cycle.

A currency does not become dominant by decree.

It becomes dominant because it is trusted.

And it is trusted because it is backed (explicitly or implicitly) by:

a strong economy,

deep and liquid capital markets,

a credible legal system,

and, crucially, the geopolitical and military power to enforce the system in which it operates.

But as the long-term debt cycle matures, and as internal and external pressures mount, that trust can begin to erode.

Not all at once.

Not in a single dramatic collapse.

But gradually, then suddenly.

Foreign holders begin to question whether their claims will be honored in real terms. Domestic policymakers become more willing to prioritize internal stability over external credibility. Money creation accelerates. Real returns compress. And alternative stores of value (historically gold, but potentially other assets like Bitcoin) begin to attract attention.

Dalio has been very explicit about this.

When a dominant power becomes overextended financially and then reveals weakness (militarily, economically, or politically) confidence can shift.

And when confidence shifts, so do capital flows.

And when capital flows shift, so does the monetary order.

Now step back and look at the structure we have just outlined:

A long-term debt buildup.

Followed by monetary accommodation and eventual monetization.

Accompanied by rising internal conflict.

Intersecting with external geopolitical rivalry.

And culminating in pressure on the reserve currency system itself.

This is not a generational theory.

This is a macro/financial one.

And yet, the overlap with the Fourth Turning framework is striking. Because what Howe describes as a crisis of institutions, Dalio describes as the inevitable consequence of accumulated financial imbalances. What Howe frames as a generational climax, Dalio frames as the late stage of a long-term debt and power cycle. And what Howe observes historically as periods of rupture, Dalio explains mechanistically as periods when the system can no longer sustain itself under the existing rules.

Two different lenses.

One from sociology.

One from macroeconomics.

But both pointing to the same uncomfortable conclusion: there are periods in history when the existing order becomes unsustainable.

So, where does that leave our hypothesis?

Does Dalio confirm that Fourth Turnings coincide with monetary resets?

Not exactly...

But before answering that question too quickly, it is worth pausing on just how much overlap we have already uncovered.

As we have now seen, Dalio’s framework and the Fourth Turning framework share some striking similarities, even if they approach long cycles from very different angles. Howe begins with generations, social mood, and institutional legitimacy. Dalio begins with debt, incentives, capital flows, and power. One is more sociological. The other is more macro.

But that difference, in our view, makes the overlap more compelling, not less. If two very different lenses point toward a similar underlying rhythm, the thesis becomes harder to dismiss as mere narrative convenience.

And the similarities are not trivial ones.

Both frameworks, for instance, point to a cycle lasting roughly 80 years... approximately the span of an average human life.

That detail matters more than it may seem. Because for societies to make the same broad mistakes again, it helps if the people who vividly remember the last disaster are no longer in positions of power... or are no longer alive at all. That is part of what gives these long cycles their recurring character. They are not mechanical in the sense of a clock. They are human. They capture the way memory, complacency, overreach, and institutional decay unfold across generations.

There is another important overlap.

Both frameworks also point, in different ways, to 2008 as the beginning of the current system’s terminal phase. For Howe’s framework, the Global Financial Crisis (GFC) marked a decisive escalation in institutional breakdown and public distrust. For Dalio, it marked the point at which the old playbook ceased to function cleanly and the authorities were forced into a new regime of extraordinary intervention: zero rates, balance-sheet expansion, and large-scale money creation. In other words, both frameworks see the post-2008 era not as a normal continuation of the old order, but as the beginning of its more unstable and improvisational endgame.

That is a remarkable convergence.

What, then, does Dalio actually confirm?

He does not confirm our hypothesis (that Fourth Turnings climax with monetary resets) in any neat or formulaic sense. But he does something just as important.

He provides a framework that explains why monetary systems become vulnerable in the first place. He shows how debt, money creation, political conflict, and geopolitical rivalry interact to push systems toward a breaking point. He shows why the old rules stop working. And he shows why, at certain moments, policymakers are forced to choose between outcomes that all carry significant costs.

What he does not do, at least not explicitly, is tell us what the next system must look like.

His work points toward outcomes such as:

currency debasement,

financial repression,

debt restructuring,

and, at times, a return to harder anchors such as gold.

But it leaves open a critical question. A question that, in our view, may define this Fourth Turning more than any previous one: through what infrastructure will the next system of trust actually operate?

Because if Dalio helps us understand when systems break... and why they break... he is far less explicit about how they are rebuilt.

And that is precisely where we now turn.

Read Part 2:

You might also like reading:

Looking for where to start?