When the money breaks

The Infrastructure of Trust: Why great crisis eras always end in a monetary redesign.

Have you noticed what the dollar is doing?

Just when the consensus was lining up for its decline, the greenback has been strengthening again, the latest twist in a year that keeps punishing comfortable narratives. That, of course, is exactly the kind of setup that interests us.

This post comes from March’s issue of VMF’s Strategic Asset Allocation, and it is the first installment of a two part series. In that issue, we make what may be our most contrarian monetary claim yet: that this Fourth Turning’s reset may be digital, blockchain based, and crypto in nature, not as a rebellion against the system, but as the next infrastructure through which trust, settlement, and monetary power move.

But before making that leap, we need to start where serious investors always should: with history.

Because Fourth Turnings are not just eras of political rupture, war, and institutional stress. They are also, again and again, eras of monetary reset. The Continental collapse. The Greenback experiment. The break with gold and the birth of Bretton Woods. In every great American Crisis era, the money eventually breaks, and then gets redesigned.

That is what this first part is about.

Below, in “When the Money Breaks,” we go deep on the historical precedent for Fourth Turnings as monetary turning points, because if you want to understand what may come next, you first need to understand the pattern America keeps repeating.”

There is a pattern in American history that most investors never stop to notice.

In every great national crisis, the fighting is never confined to battlefields, cabinets, or elections. Sooner or later, it reaches the money. The old unit of trust gets stretched, discredited, devalued, or redesigned. And by the time the crisis has run its course, the country is no longer operating under the same monetary logic it had before. That is one of the great recurring signatures of a Fourth Turning: when the nation breaks, the money changes with it.

Start with the Revolutionary War1 (1775-1783).

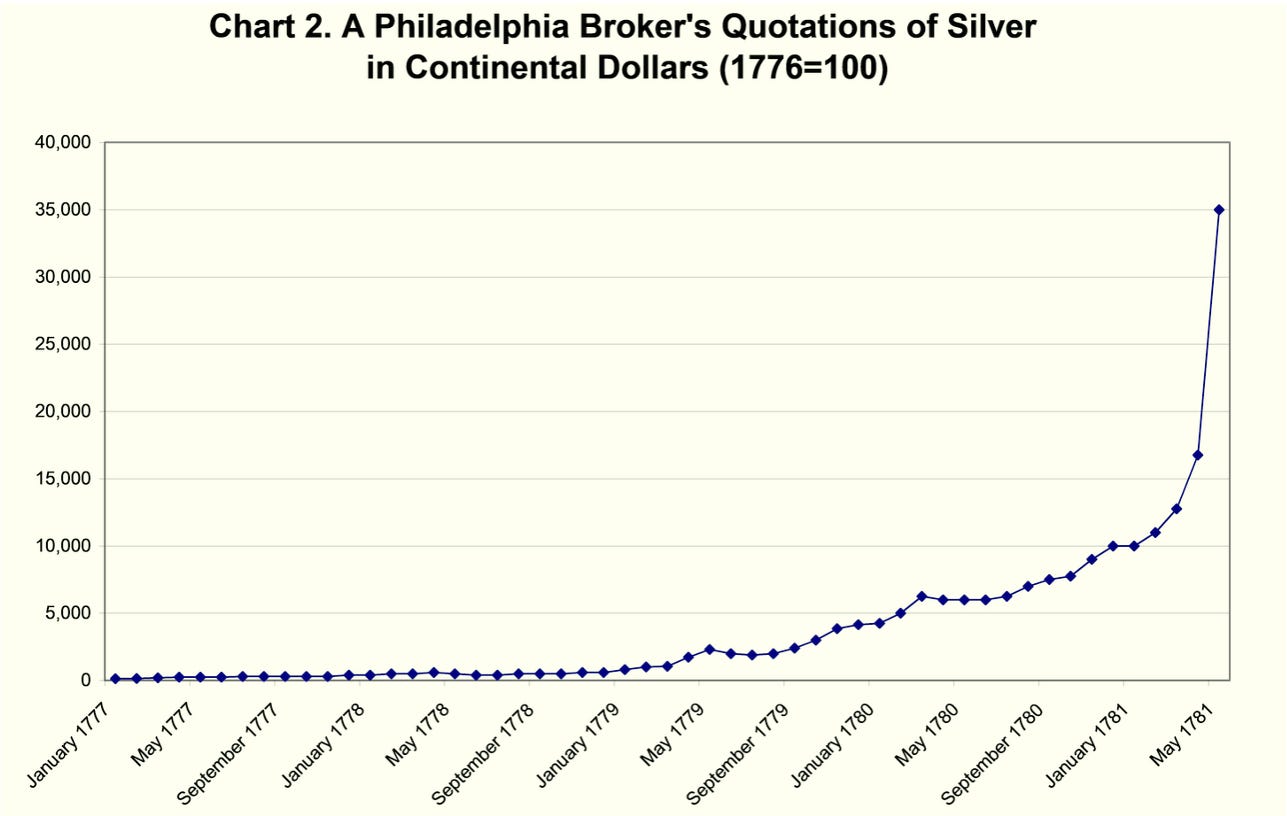

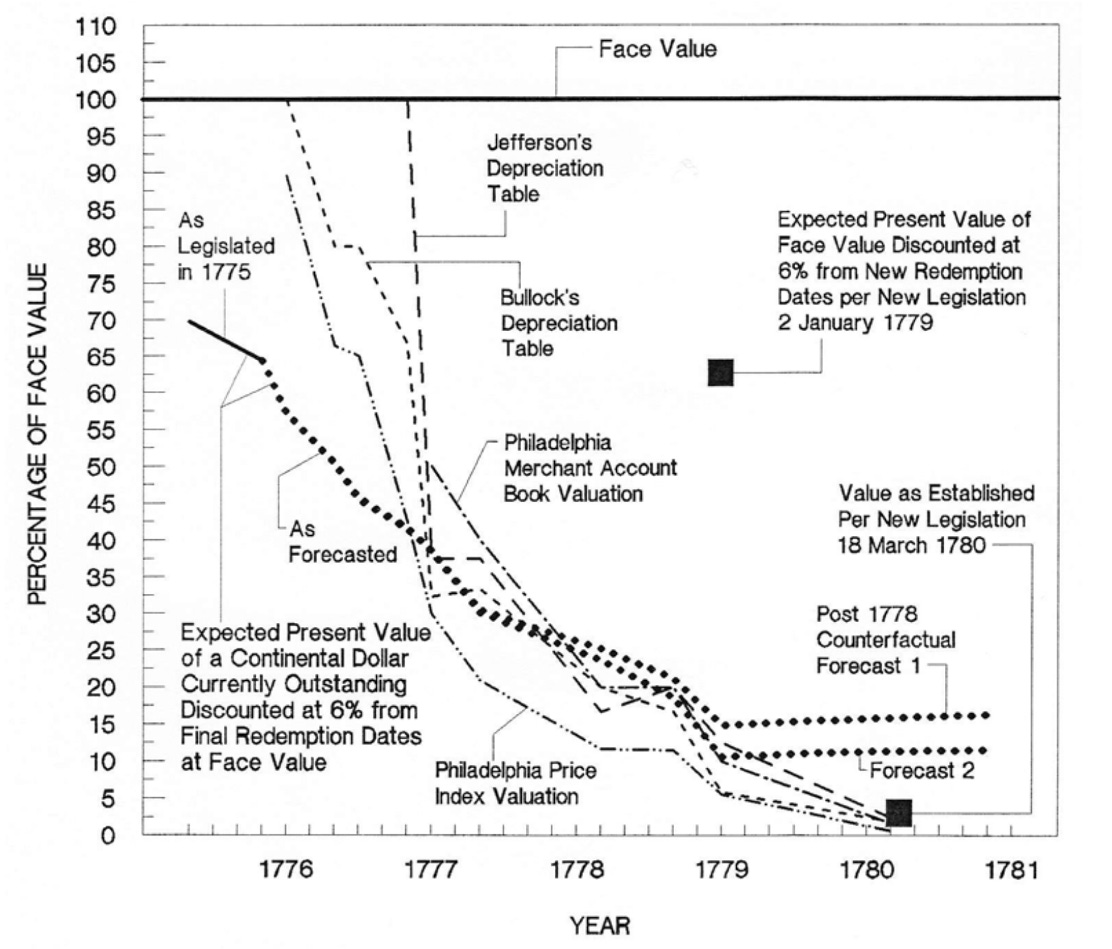

Most people know the phrase “not worth a Continental,” but too few appreciate how violent the underlying monetary collapse really was. To finance the war, the Continental Congress relied heavily on paper emissions because it lacked a strong independent taxing power.

In the first years of the conflict, Continental dollars funded the overwhelming bulk of Congressional spending. As more notes were issued and confidence in future redemption weakened, their value eroded badly. By the end of 1777, the specie value of the Continental had fallen to about 20% of its original value, and by the end of 1779, one paper dollar was worth only about one or two cents in silver...

That is not mere inflation.

That is a collapse in monetary credibility so severe that the currency’s name entered the language as a synonym for near-worthlessness.

There is one important nuance here: the Continental was not originally conceived as a pure fiat note in the modern sense, but as something closer to a zero-interest bearer bond whose present value would naturally trade below face value ahead of final redemption. In other words, some early decline reflected discounting, not outright debasement.

But that nuance does not rescue the larger picture... once Congress altered redemption terms in 1779 and 1780 in ways that were not fiscally credible, the public’s trust snapped. Depreciation turned into collapse.

The Revolutionary monetary reset, then, was brutal but foundational: the old wartime paper failed, and the lesson it burned into the American mind was that durable money required a stronger fiscal state and a more credible public-credit architecture.

That is why the true reset after the Revolution was not simply that the Continental disappeared. It was that the United States gradually moved toward a more coherent national financial order, one built on stronger federal institutions and, eventually, Hamiltonian public credit2. The crisis destroyed one form of money and forced the young republic to think much more seriously about what had to stand behind the next one. The phrase “not worth a Continental” was the scar tissue left behind by that lesson.

Then, roughly eight decades later, the country broke again.

The Civil War (1861-1865) created another moment when the old monetary discipline could not survive the emergency.

In late 1861, specie payments were suspended... that is, the financial system stopped honoring the old hard-money promise that paper could be turned into gold or silver coin on demand. From that moment on, the dollar was no longer anchored in the same way to precious metals.

The public could still hold paper, spend paper, and receive paper... but the right to walk in and demand redemption in specie had effectively been cut off. Then came the Legal Tender Act3 of 1862, which authorized $150 million in non-interest-bearing notes that became known as greenbacks.

By the end of the war, the stock of greenbacks had risen sharply, and the federal

government had crossed a line it had long been reluctant to cross: issuing a true

national paper currency that was not convertible into gold or silver on demand. The

old money had not merely been supplemented. Its discipline had been suspended.

And what happened to purchasing power?

It eroded... fast. As the war progressed, prices expressed in greenbacks roughly doubled, meaning the paper in people’s hands was steadily losing real value.

But this was not a simple one-way story of wartime inflation. The greenback also became a live barometer of the war itself, rising and falling with battlefield developments and with the market’s confidence in the Union cause. Once redemption in gold had been cut off, the dollar no longer rested on metal alone. It rested on politics, military success, and the perceived survival of the state.

The greenback was emergency money for an emergency state, and it traded like one. But here again, the debasement story is only half the story. The deeper reset was institutional. The Civil War did not just cheapen the old money... it helped create a new monetary architecture. The National Banking Acts of 1863 and 1864 established a federally chartered banking system and pushed the country toward a more uniform national currency, reducing reliance on the chaotic patchwork of state-bank notes that had defined much of antebellum America. Then, after years of political conflict, the U.S. resumed specie payments in 1879.

So, once again, the sequence was unmistakable: suspend convertibility, issue emergency paper, suffer inflation and depreciation, then rebuild around a stronger and more centralized national monetary order.

That was the Civil War reset.

Then, roughly another three quarters of a century later, America and the world entered the next great crisis era: the Great Depression and World War II (1929-1945). Here the pattern changes form, but not substance.

In the early 1930s, the problem was not that the dollar was collapsing in domestic purchasing power. Quite the opposite: the gold standard’s rigidity was helping produce a deflationary squeeze. Banks failed, output imploded, and adherence to

gold acted less like a badge of discipline than a monetary straitjacket. Roosevelt’s response in 1933 was to break that constraint. In April of that year, he formally suspended the gold standard, halted gold exports, and stopped the Treasury and financial institutions from converting currency and deposits into gold.

Then came the decisive monetary rewrite.

The Gold Reserve Act of 1934 transferred ownership of monetary gold to the U.S. Treasury, prohibited redemption of dollars for gold, and redefined the official gold price from $20.67 per ounce to $35.

That amounted to a roughly 41% devaluation of the dollar against gold.

So, while the Depression-era reset did not begin as a classic inflationary debasement like the Continental or the Greenback episodes, it still involved a deliberate reduction in what the dollar promised in gold terms. The old gold-backed dollar lost value against its anchor, and that was no accident. It was policy.

And yet even that was not the final settlement.

As with the earlier Fourth Turnings, the true reset only became clear after the broader crisis reached its climax. Near the end of WWII, in 1944, delegates from 44 nations met at Bretton Woods4 and designed a new international monetary order.

Under that system, other currencies were fixed to the U.S. dollar within narrow bands, while the dollar itself was fixed to gold at $35 per ounce.

The old interwar gold regime had failed. In its place emerged something very different: a dollar-centered system in which American state power, American finance, and American gold reserves together formed the new infrastructure of global monetary trust.

That was the postwar reset.

Now step back and look at the pattern:

The Revolutionary crisis.

Then the Civil War.

Then the Great Depression and World War II.

Each separated by roughly the span of a long human life. Each coinciding with profound institutional stress. Each forcing the United States to confront the same question in a different form: what exactly stands behind the money? And each, in its own way, ending with a different answer than the one that existed before the crisis began.

But there is an even bigger pattern hiding inside that one. Each reset did not merely wound the old money. It also concentrated monetary power more heavily than before.

After the Revolutionary debacle, the answer was a stronger federal fiscal state.After the Civil War, it was a more centralized national banking and currency architecture. After the Depression and World War II, it became something larger still: a dollar-centered international order, with the United States sitting at the core of the world’s new monetary system. In other words, the arc was not just from one kind of money to another. It was from weaker and more fragmented monetary authority to stronger and more centralized monetary authority... first nationally, and ultimately globally.

That is the real claim we want to make in this issue.

Not that history repeats mechanically.

Not that every crisis produces the same monetary outcome.

And not that Fourth Turnings are “about money” in some narrow sense.

The deeper point is more powerful than that. When the nation enters an existential crisis, the monetary order becomes vulnerable. Old anchors fail. Emergency measures appear. Political imagination expands. And what once seemed permanent suddenly becomes negotiable.

But the resolution of the crisis tends to move in a recognizable direction: toward a new monetary settlement backed by greater state capacity, greater centralization, and, at times, a wider sphere of power than the one that existed before. That was true of the Continental. It was true of the Greenback. It was true of gold backing and Bretton Woods.

And it may prove true again. Which brings us to the most important leap of this issue: our working hypothesis for the possible anatomy of this Fourth Turning’s monetary reset... arriving, not coincidentally, roughly 80 years after the last one.

Read the latest:

The American Revolutionary War, fought from 1775 to 1783, was not only the birth of the United States... it was also the country’s first great monetary crisis. To finance the war, the Continental Congress issued large amounts of paper currency, but under the Articles of Confederation it lacked a strong independent taxing power to support that money credibly. As issuance grew and confidence weakened, the Continental dollar collapsed in value, giving rise to the phrase “not worth a Continental.” The deeper lesson was lasting: a nation could win its independence and still lose control of its money. That monetary trauma helped shape the push for a stronger federal financial order in the years that followed.

Hamiltonian Public Credit refers to the financial system Alexander Hamilton built in the 1790s to restore the young republic’s credibility after the Revolutionary War. Its core idea was simple but transformative: the United States would honor its debts in full, fund them reliably, and use that credibility to create a deeper market for government securities. By combining federal taxation, debt assumption, and the creation of a national bank, Hamilton turned public debt from a symbol of weakness into a foundation of state power. In practical terms, he gave the United States something it had previously lacked: a credible financial architecture behind its money and its sovereignty.

The Civil War, fought from 1861 to 1865, became the second great monetary rupture in American history. Faced with soaring wartime costs, the Union suspended specie payments in late 1861, meaning paper claims could no longer be redeemed for gold or silver on demand. Congress then passed the Legal Tender Act of 1862, authorizing the first true national paper currency: the Greenback. These notes were not convertible into gold, and as issuance expanded their purchasing power fell sharply, with prices in greenbacks roughly doubling during the war. But the deeper legacy was institutional: the crisis pushed the United States toward a more centralized national banking and currency system, replacing a fragmented monetary order with a stronger federal one.

Bretton Woods was the postwar monetary settlement designed in July 1944 by 44 Allied nations to prevent a repeat of the currency chaos, competitive devaluations, and financial nationalism that had helped deepen the Great Depression. The system placed the U.S. dollar at the center of the world monetary order, fixed to gold at $35 per ounce, while other major currencies were pegged to the dollar. At the same time, the conference created two major institutions: the International Monetary Fund, meant to oversee exchange-rate stability and provide balance-of-payments support, and the International Bank for Reconstruction and Development, later known as the World Bank, to help finance reconstruction and development. Closely related to this broader postwar architecture was the creation of the United Nations in 1945, which aimed to provide the political and diplomatic framework for the new order. In that sense, Bretton Woods was not just a currency arrangement. It was part of a wider attempt to rebuild global stability under American leadership.