Hormuz and the Imperial Test

Suez Echoes and the Geopolitics of Chokepoints

By the time our last Alpha Tier issue was published, on March 27, 2026, the Iran war was already nearly a month old.

That matters.

Because this was not a first-reaction note written in the heat of the initial shock. It was written after the market had already had time to digest the obvious implications: oil, inflation, rates, risk-off. What interested us was the less obvious question.

What if this war mattered not only because of what it might do to commodities, global growth, or monetary policy... but because of what it might reveal about American power?

That is the frame for this final excerpt from March’s Alpha Tier that I’m sharing here. The more actionable portfolio implications, as always, remain with subscribers.

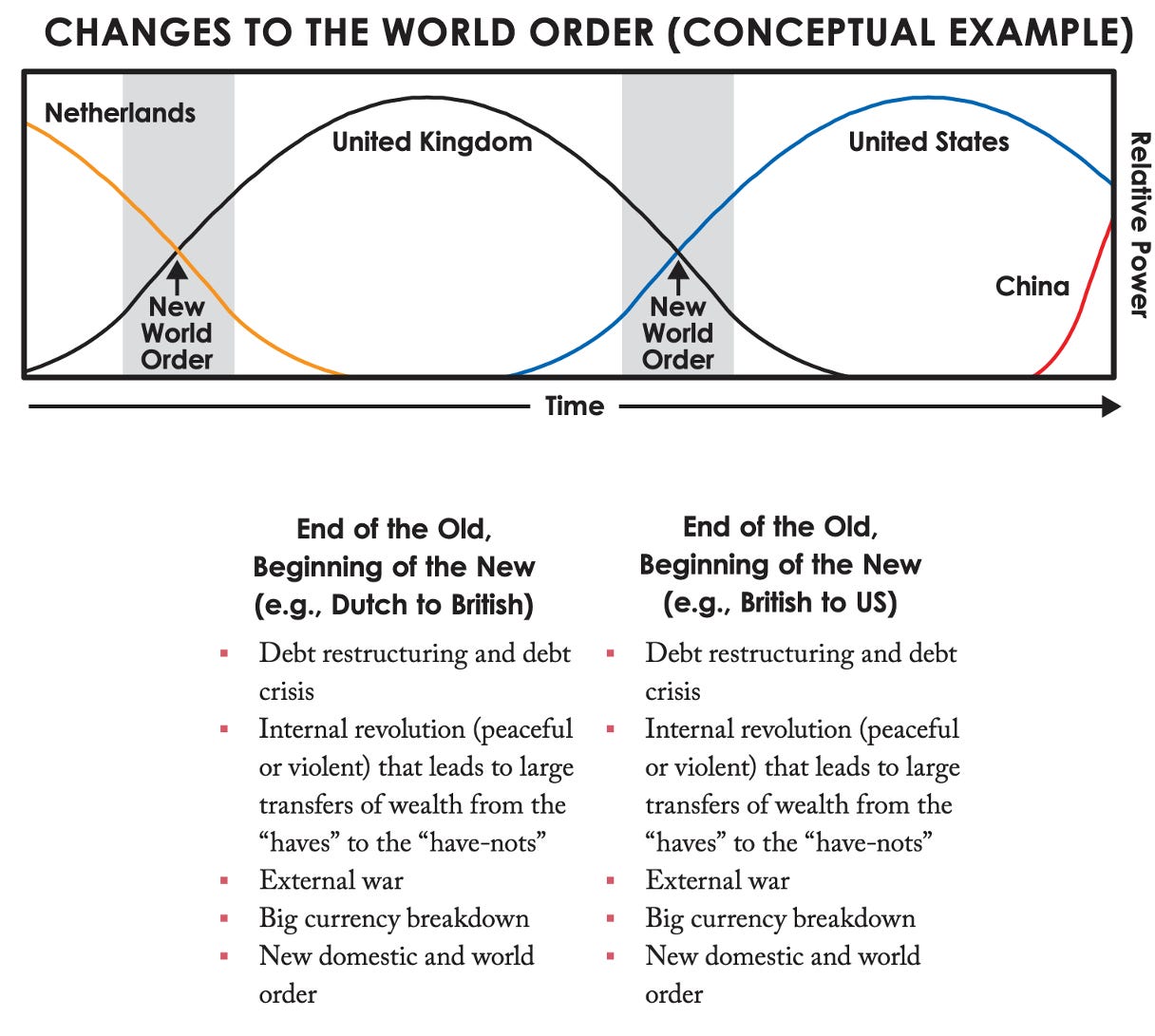

In Part 1 - Howe, Dalio, and the Stress Test, we stress-tested our Fourth Turning framework against Ray Dalio’s Big Cycle.

In Part 2 - Toward the Reset, we pushed further and asked what a late-stage monetary reset might actually look like. Now the lens shifts again. Away from money itself and toward the thing that ultimately sits behind every monetary order: ...imperial credibility.

That is why this section turns to Suez.

In 1956, Britain, France, and Israel moved against Egypt after Nasser nationalized the Suez Canal. Militarily, the operation looked feasible. Strategically, it was a disaster. The crisis exposed a simple but devastating truth: Britain could still project force, but it could no longer sustain imperial freedom of action once financial and geopolitical pressure turned against it. Suez did not merely mark a foreign-policy humiliation. It marked the moment the world saw that the empire’s reach no longer matched its image.

That is what makes the analogy worth studying.

Not because Hormuz is “the new Suez” in some cheap, one-line sense. And not because history repeats on command. But because chokepoints have a way of exposing realities that markets, politicians, and empires would rather postpone.

The excerpt below asks whether Hormuz may be that kind of test for the United States and for Trump in particular.

The portfolio actions remain where they belong. But the framework for understanding the stakes begins here.

Here is “Hormuz and the Imperial Test.”

If the previous section was about the form a late-stage monetary transition might take, this one is about the kind of event that can force that transition to accelerate.

And that is why the war with Iran matters...

Not simply because oil is rising.

Not simply because markets are volatile.

And not simply because another war has erupted in an already unstable world.

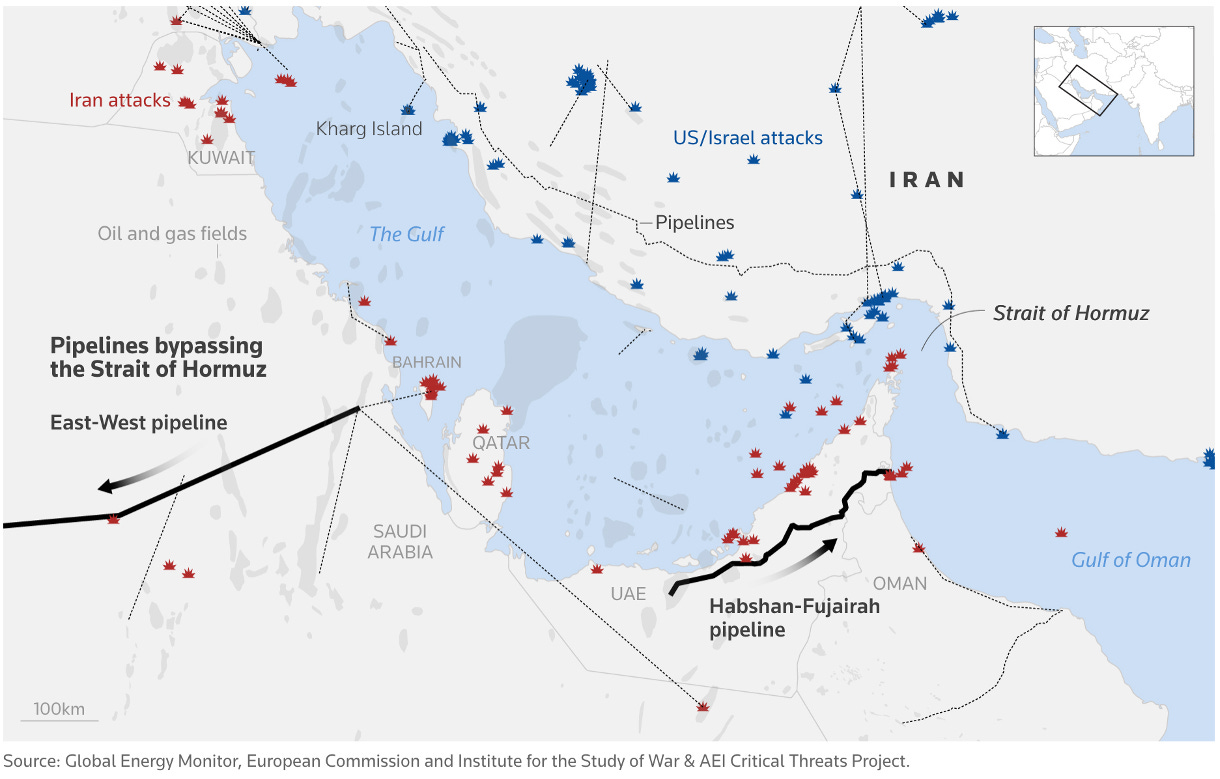

It matters because the Strait of Hormuz is not just another patch of water on the geopolitical map. It is one of the great arteries of the global system. Roughly a fifth of global oil and LNG flows normally move through it, and the conflict has already disrupted those flows materially enough to push crude back toward or above $100, force central banks to revisit inflation assumptions, and rattle markets well beyond the Middle East.

That is what makes this episode qualitatively different from a standard geopolitical flare-up.

A normal regional war can move oil for a few days and then fade into the background. A war that places Hormuz at the center of the contest does something else entirely...

It tests the credibility of the hegemon.

It tests the willingness of allies to align. It tests whether the old order can still secure the trade routes on which it rests. And, by doing so, it begins to test not just military power, but monetary confidence.

This is precisely why the Suez analogy1 is worth taking seriously.

Not because history repeats neatly. And not because we can already declare this America’s Suez. That would be premature. But because Suez captured a very specific type of imperial revelation: a moment when the world begins to understand, all at once, that the incumbent power may no longer possess the freedom of action, coalition power, or financial autonomy that its reputation had previously implied.

That is the deeper significance of 1956.

Britain and France did not simply fail to get their way in Egypt. They launched military action to retake control of a strategic waterway, only to be forced into retreat under intense political and financial pressure. Britannica’s summary is blunt: Britain and France lost most of their influence in the Middle East as a result of the episode.

The monetary dimension matters just as much.

IMF research describes Suez not only as a geopolitical crisis but as a financial one for Britain, with sterling coming under speculative pressure, reserves being drained, and Britain’s need for U.S. and IMF support giving Washington enormous leverage over the outcome.

In other words, Suez was not merely a battlefield embarrassment. It was a public demonstration that Britain’s imperial reach was already dependent on a financial architecture it no longer fully controlled.

That is the risk here...

If the United States ultimately fails to guarantee secure passage through Hormuz in a durable way, this war could come to be seen not merely as another costly conflict, but as a visible test of imperial limitation. And when such tests go badly, the consequences extend far beyond the battlefield. Allies begin to reassess. Rivals grow bolder. Capital starts to ask harder questions. And the old order, while not collapsing overnight, begins to look less unquestionable than it did before.

That is a very Dalio-style danger.

And it also fits the logic of the Fourth Turning rather well.

Because in Howe’s framework, the climax of a crisis era is not simply a matter of social stress at home. It is the point at which institutional fragility, political fracture, external conflict, and hard choices begin to converge.

The war in Iran may be one of those convergence points. In Dalio’s language, it looks like exactly the kind of late-Stage-5 shock that can push a system closer to Stage 6. In Fourth Turning language, it looks like the sort of event that can accelerate the final innings of the crisis.

That is why so much is at stake here. Not only for the great generational and civilizational cycles we have been discussing... but also for the much shorter economic cycle now trying to survive inside them.

The first-order consequences are easy enough to see.

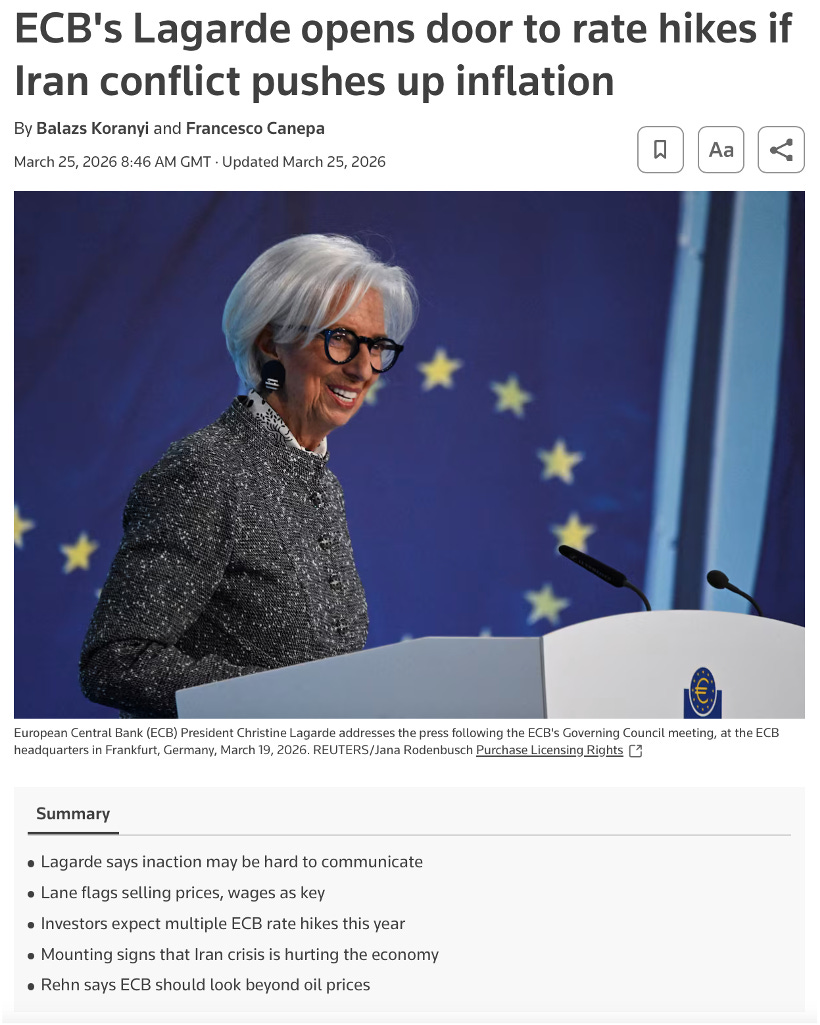

Higher oil and gas prices act like a tax on growth. They squeeze households, pressure margins, lift transport and input costs, and complicate central-bank decision making. The ECB has already raised its inflation forecast because of the energy shock while also cutting growth assumptions, and the Bank of England has signaled that war-related energy pressures could push inflation materially higher in the coming quarters.

That alone is serious.

But the second-order consequences are where the real danger begins.

A sustained Hormuz disruption does not simply raise energy prices. It starts to alter behavior across the entire system. Firms delay investment. Consumers retrench. Freight and insurance costs rise. Credit spreads can widen as recession risk increases. Rate expectations become harder to anchor because central banks are forced to choose between tolerating inflation and protecting growth. And if energy stays high long enough, the initial inflation shock can morph into something more stagflationary and more corrosive to confidence.

This is also where the long-term rates picture becomes critical.

Have you check Our latest leaderboard? It tells the story better than any intro, showing our total returns since publication, including multiple triple-digit winners and a consistent record of beating the market while managing risk.

Because the real macro danger is not merely that inflation moves up. It is that long duration borrowing costs start to reprice a more disorderly combination of inflation, fiscal strain, and geopolitical risk. Reuters has already framed the conflict as trapping Treasury investors in a “stagflationary oil dilemma,” noting that oil in the $100–$130 range for any length of time could wipe out the case for rate cuts and even reopen the door to rate hikes.

Since the conflict escalated, the 10-year Treasury yield has moved materially higher, mortgage rates have climbed to their highest since October, and concern has grown that any decisive breakout in the long end would tighten financial conditions across housing, corporate borrowing, private credit, and government finance all at once.

That is not a trivial risk.

A breakout in long-term yields would not simply be a bond-market story. It would be a system-wide repricing. Housing would feel it immediately. Leveraged borrowers would feel it quickly. Equity valuations (especially for long-duration growth assets) would come under renewed pressure. Private-credit stress could worsen. Fiscal arithmetic would deteriorate further as governments refinance at more punitive levels.

And perhaps most importantly, policymakers would find themselves cornered: unable to celebrate higher yields because of the growth damage, but unable to ease policy cleanly because the very shock pushing yields higher would also be keeping inflation elevated.

Then come the unintended consequences.

These are often the most important ones in moments like this...

A prolonged disruption to Hormuz can force changes that outlast the war itself. It can accelerate reserve diversification at the margin. It can deepen distrust between allies. It can push governments toward industrial policy, energy nationalism, and more overt economic coercion. It can strengthen the political case for financial repression, for larger fiscal deficits, for balance-sheet intervention, and for emergency state involvement in strategic sectors.

It can also, paradoxically, increase the appeal of both old hard-money hedges and new digital rails at the same time...

That last point matters.

Because if the old order begins to look more brittle, the world does not need to leap immediately into a new reserve currency for the monetary debate to change. It only needs to become more interested in alternatives at the margin... more gold, more local-currency settlement, more bilateral workarounds, more stablecoin usage, more tokenized collateral, more experimentation with digital forms of trust transmission. In other words, a shock like this does not have to overthrow the dollar to start reshaping the architecture around it.

That is why this war may prove so consequential for the shape of the reset.

A successful reassertion of control by the United States would reinforce one version of the world: a stressed but still durable American order, one in which the dollar remains central and adaptation occurs through extension, improvisation, and renewal. A failure, by contrast, would strengthen a different version: one in which allies hedge more aggressively, rivals press harder, and confidence in the old architecture weakens more visibly.

Either way, the event matters. And it matters not only for the long cycle, but for the shorter one too.

If the shock fades quickly, markets may be forced to reprice how pessimistic they became, particularly if policymakers lean toward renewed liquidity support to prevent a broader financial tightening. But if the disruption proves more persistent, the growth hit, inflation pressure, bond-market stress, and confidence effects could become mutually reinforcing.

That is the real message. The Iran war is not just a headline risk. It is not just an oil shock. And it is not just another excuse for volatile markets...

It is a live test of whether the existing order can still absorb a strategic chokepoint

shock without revealing deeper weakness.

And that is why it belongs in this issue. Because if both the Fourth Turning framework and Dalio’s Big Cycle are even directionally right, this is exactly the kind of event we should expect near the climax: an event in which external conflict, monetary fragility, inflationary pressure, alliance credibility, and questions about the future shape of trust all begin to collide.

Now... what does this mean for our Model Portfolio? Subscribe our premium tiers at VMF Research to get the answer.

Choose your edge:

The Alpha Tier: Our highest conviction. Unlocks tactical trading ideas, market-timing strategies, and full access to both Tiers 1 and 2.

Tier Two: Security Selection: The “What to Buy.” High-conviction model portfolios focused on Value, Quality, and secular themes like the tokenization boom.

Tier One: Strategic Asset Allocation: The “Big Picture.” 12 monthly issues mastering the macro rotations that actually move the needle.

You might also like reading:

Our leaderboard tells the story better than any intro. It shows our total returns since publication, including multiple triple-digit winners and a consistent record of beating the market while managing risk.

You might also like reading Part1 and Part2 of this edition:

The Suez Crisis of 1956 was the failed British and French attempt to retake control of the Suez Canal after Egypt nationalized it, and it became a defining moment in Britain’s imperial decline because it exposed the gap between military ambition and financial independence. It matters today because the current war with Iran raises a similar question for the United States: if a dominant power cannot secure a critical global chokepoint such as the Strait of Hormuz, allies, rivals, and capital markets may begin to reassess the credibility of the order it leads.