Toward the Reset

A clean break? No. The infrastructure of trust might simply be migrating to digital rails.

In Part 1 , we did the hard work first.

We took our Fourth Turning framework and stress-tested it against Ray Dalio’s Big Cycle. Different lenses. Different starting points. One rooted in demography, generations, and institutional decay. The other in debt, money, power, and incentives. And yet both pointed to the same uncomfortable place: a late-stage crisis era in which the old order is becoming harder and harder to sustain.

Now we move to the question that matters even more.

If the system is breaking, what comes next?

That is what Part 2 is about.

This second installment comes from March’s issue of Alpha Tier, “The Monetary Endgame”, and here we move beyond diagnosis and into the real debate: the form of the reset itself. Is it analog? Is it gold-led? Is it some new version of financial repression? Or does this Fourth Turning take a more modern path, built on digital rails, tokenized trust, and a monetary architecture that may prove far more crypto-friendly than the crowd still imagines?

That, of course, is where things get interesting.

Because most investors are still trapped in the old script. They can imagine disorder. They can imagine debasement. They can imagine pressure on the dollar. What they struggle to imagine is that the next reset may not simply destroy the old infrastructure of trust.

It may rebuild it in a new form.

And that is precisely where we go next.

In “Toward the Reset,” we move from vulnerability to architecture. From why systems break to how a new monetary order may begin to take shape.

Here is Part 2 - Toward the Reset.

If Dalio helps us understand why systems become vulnerable, his staging of the Big Cycle helps us understand something else that is equally important: where we are inside the process.

That matters enormously.

Because one of the easiest ways to misunderstand long-cycle frameworks is to treat them as interesting historical abstractions rather than as attempts to identify a position in time. And although Dalio is somewhat more cryptic about the actual shape of monetary resets, he is much clearer about the sequencing of the Big Cycle’s stages.

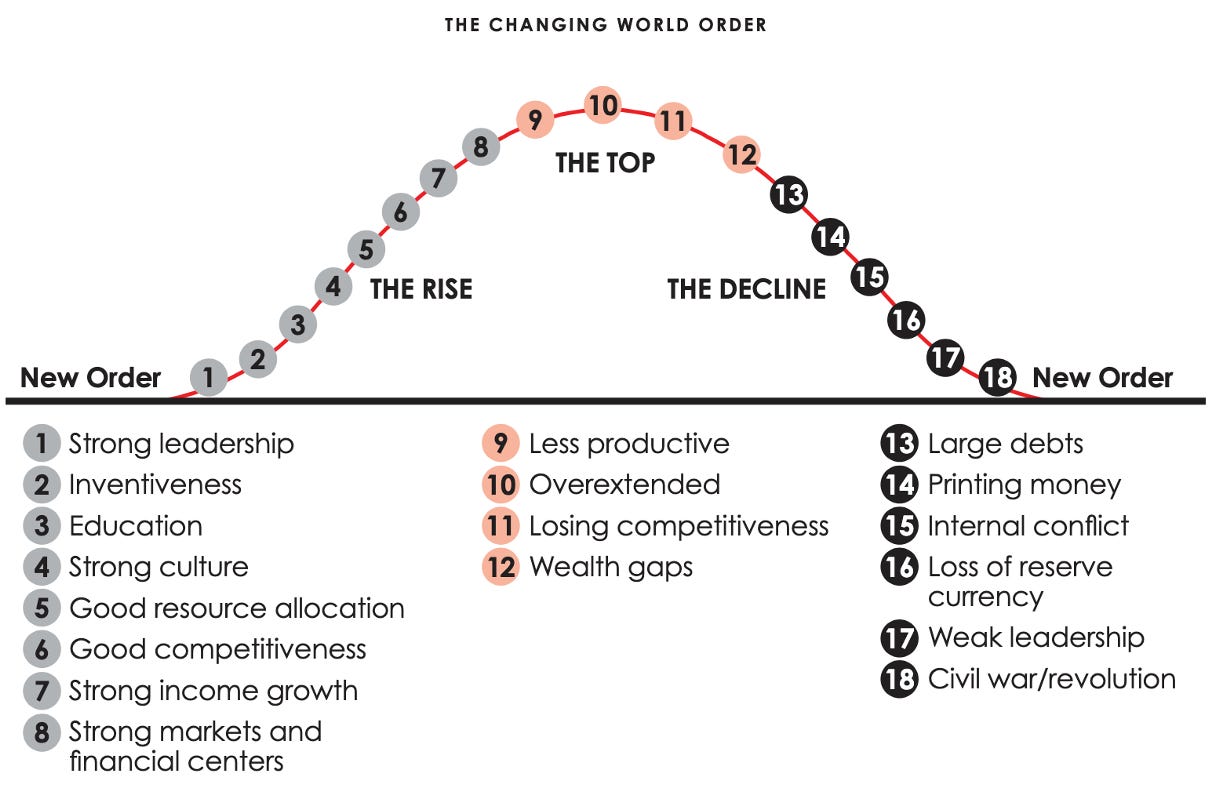

In his own six-stage telling of the Big Cycle, the progression is roughly as follows:

Stage 1 begins with the creation of a new order after the breakdown of the old one;

Stage 2 is the period of productive building, rising competitiveness, and institutional strengthening;

Stage 3 is the phase of prosperity, confidence, and broadening wealth;

Stage 4 is when excesses begin to accumulate, debt rises, imbalances widen, and the system starts to live increasingly off financial engineering rather than productive strength;

Stage 5 is the dangerous pre-breakdown phase, when debt burdens, internal conflict, and geopolitical rivalry intensify sharply;

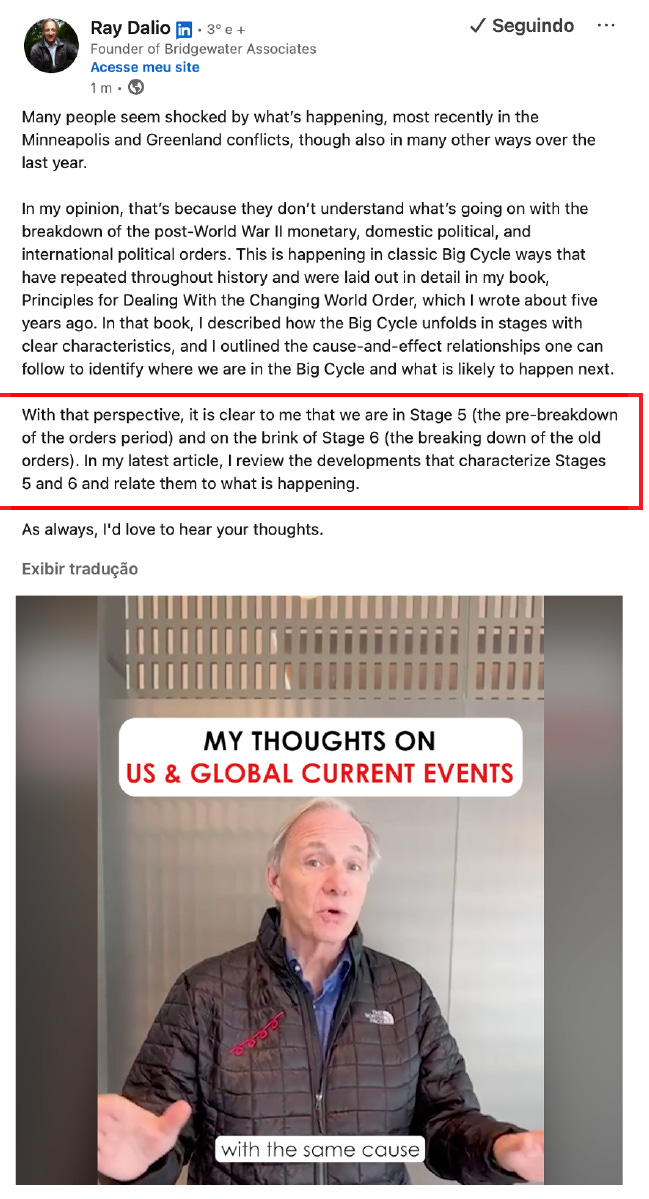

and Stage 6 is the actual breakdown phase, the period of great disorder in which the old rules no longer hold and a new order struggles to emerge. Dalio has now said plainly that we are in Stage 5.

That should sound very familiar to readers of this publication. Because while Dalio does not use Howe’s language, his diagnosis places us in much the same historical neighborhood: not in the early or middle innings of the cycle, but in its dangerous closing stretch. A stretch in which the old order is visibly weakening, the next one is not yet formed, and the monetary architecture itself becomes increasingly contestable.

And that brings us directly to the real debate.

What matters now is to understand what typically happens as systems move from Stage 5 into Stage 6... or, in the language of the Fourth Turning framework, what tends to happen in the final innings of a crisis era.

That is the transition that concerns us.

Not the comfortable middle of the cycle. Not the phase in which imbalances are still manageable and policymakers can plausibly pretend that the old rules remain intact. But the phase in which those imbalances begin to force resolution... one way or another.

If we are indeed in this late-stage transition then the important question is no longer whether the old system is under pressure.

It is: what happens next? And, more specifically for the Market View we are testing: what form does the monetary reset now take?

The instinctive answer, for many investors, is to look backward.

And fair enough. History offers a familiar playbook.

As systems move from late-stage strain into outright breakdown, the menu of outcomes tends to narrow. Policymakers and states usually fall back on some combination of:

currency debasement,

financial repression

debt restructuring,

and, at times, a return (partial or explicit) to harder anchors such as gold.

These mechanisms are not theoretical curiosities. They are the classic tools through which overextended systems attempt to survive.

Currency debasement reduces the real burden of debt by allowing inflation to outrun nominal obligations. Financial repression channels savings into government liabilities, often through regulation, captive domestic investor bases, or persistently negative real rates. Debt restructuring, whether overt or disguised, redistributes losses across creditors, debtors, and institutions. And gold, historically, has served as the external anchor of last resort... the asset to which systems return, explicitly or implicitly, when fiat credibility has been stretched too far.

In other words, when Stage 6 arrives, the issue is rarely whether the system changes.

It is how disorderly the adjustment becomes... and which mechanisms are used to restore trust, discipline, or merely temporary stability.

There is no reason to believe these tools will disappear.

In fact, we have been seeing signs of several of them for years. Real interest rates remain politically sensitive. Fiscal dominance is no longer a fringe concept. And the boundary between monetary and fiscal policy continues to blur.

But there is a risk in relying too heavily on this historical template alone. Because this time, the system is not evolving in a vacuum. It is evolving alongside two realities that make this transition meaningfully different from prior ones.

The first is that we are living through a period of remarkable technological innovation. The second is that the world appears to be becoming more fragmented, more contested, and more multipolar.

Both matter.

For the first time in modern monetary history, the infrastructure through which money moves is itself being reinvented in real time.

We believe that is a gamechanger.

Because if previous monetary transitions were largely about changing the unit (gold to fiat, fixed to floating, domestic to global reserve) this one may also be about changing the rails.

Consider what is already emerging:

Central bank digital currencies (CBDCs), designed to give states more direct control over money and payments;

Stablecoins, which extend sovereign currencies into digital ecosystems with near-instant settlement;

Tokenized assets, which allow traditional financial instruments to move across blockchain-based infrastructure;

and crypto-native assets, most notably Bitcoin, which exist outside the traditional system altogether and offer an alternative store of value.

These are not theoretical constructs.

They are active, competing architectures.

And importantly, they are not mutually exclusive.

This is where the debate becomes more nuanced.

The next monetary adaptation is unlikely to be a clean break in which one system replaces another overnight.

More likely, it will be layered.

The existing fiat system may persist, but with greater reliance on financial repression and balance-sheet expansion. Gold may reassert itself as a neutral reserve asset, particularly in a more fragmented geopolitical landscape. CBDCs may emerge as tools of state control and efficiency, especially in domestic contexts. And at the same time, stablecoins and blockchain rails may extend the reach of existing currencies (particularly the dollar) into new domains of economic activity.

,In that sense, the next system may not be defined by a single dominant form. It may be defined by the interaction between multiple layers of money and multiple layers of infrastructure.

And this is precisely where our thesis begins to diverge from the conventional narrative...

The dominant expectation today tends to frame the future in binary terms:

either the dollar system persists... or it is replaced.

either gold returns... or fiat systems collapse.

either crypto disrupts the system... or it remains marginal.

We think this framing is too simplistic. Because it ignores a more subtle, and, in our view, more likely path.

A path in which the existing system adapts not by rejecting new technologies, but by absorbing them.

A path in which the dollar does not disappear, but is increasingly extended through new digital infrastructure.

A path in which blockchain-based systems do not replace sovereign currencies, but become part of the way those currencies move, settle, and scale.

And that point becomes even more important once we confront the question of multipolarity...

Yes, the world is clearly becoming more contested. Yes, rival power centers are asserting themselves more openly. Yes, the unipolar moment is fading. But from that, many investors jump too quickly to the conclusion that the dollar must therefore be on the verge of losing its hegemonic role.

We think that leap is premature.

This cover reflects the current consensus view toward the US dollar, and we see it as a valuable contrarian indicator, often signaling that positioning and sentiment may already be stretched in one direction.

Because whatever its vulnerabilities, the dollar still sits at the center of the system.

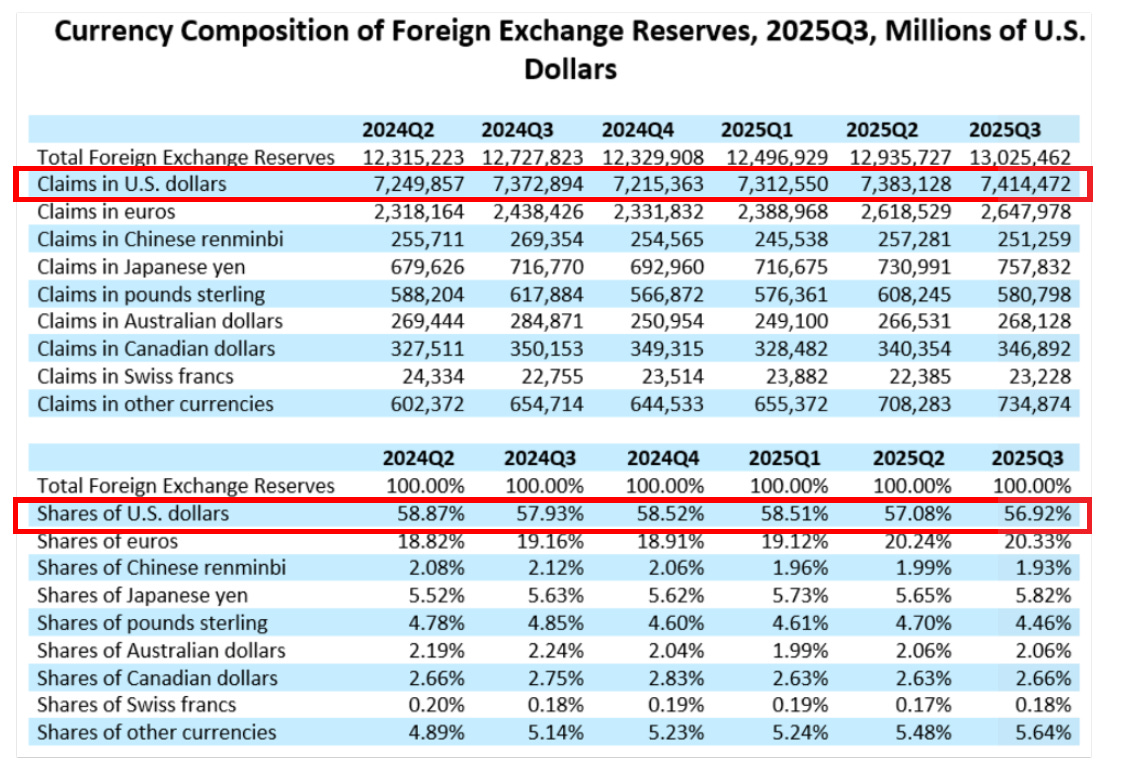

And if you look at what stands in second place, the contrast is hard to ignore.

The euro remains the nearest challenger by share, but does anyone seriously believe it is better positioned than the dollar to anchor the next era of global trust?

A currency backed by a politically fragmented monetary union, with no single fiscal sovereign behind it, hardly looks like the obvious successor.

And the yuan? It may belong to a rising power, but it remains embedded in a system of capital controls, opaque policymaking, and limited convertibility. That is not the natural foundation of a truly global reserve alternative either.

No... our view is more subtle than that.

We do believe multipolarity is increasing. We do believe the world is fragmenting. We do believe that reserve diversification is likely to continue at the margin. But we do not think that automatically implies a clean post-dollar world.

What we think it implies is something more complex... and, perhaps, more interesting.

A world in which the dollar likely remains hegemonic for longer than many now assume... but one in which the architecture surrounding that hegemony changes materially. A world in which technological innovation plays a much larger role in how trust is transmitted. A world that becomes more digital, more programmable, more tokenized, and, in that sense, more crypto-friendly than the conventional reserve-currency debate usually allows.

In other words, the monetary reset (if that is indeed what we are approaching) may be less about replacing the dollar than about rebuilding the infrastructure through which dollar-based trust operates.

That distinction is critical.

Because it shifts the focus of the debate.

From: what is the next form of money?

To: how is trust going to move?

And once you ask that question, a different set of implications begins to emerge.

The winners are not necessarily those assets that simply benefit from monetary disorder. They are those positioned at the intersection of:

trust,

custody,

compliance,

distribution,

and settlement infrastructure.

They are the tollbooths, not just the commodities.

But before we translate that into Model Portfolio positioning, we need to confront the present. Because these transitions do not occur in clean, theoretical environments.

They occur in moments of stress.

Moments in which geopolitical conflict, economic fragility, and policy constraints collide in ways that force the system to reveal its underlying weaknesses.

And that is exactly what we may be witnessing now.

The question, then, is whether the current Iran shock is simply another episode of geopolitical volatility... or whether it is something more consequential: a live test of the very fractures that define this stage of the cycle.

That is where we now turn.

Are you ready for a reset ? To see our full, position-by-position trading plans and the technical triggers we’re watching for the next rotation, subscribe to VMF Research today.

You might also like reading:

Looking for where to start?