A Fourth Turning Goes On-Chain

How Treasury-backed stablecoins are co-opting the blockchain to save the dollar.

In Part 1 - When the money breaks, we made the historical case.

America’s great Crisis eras have a habit of ending the same way: the monetary order comes under stress, the old constraints break, and a new architecture of trust takes shape.

Now comes the more controversial part.

What if this time the reset does not begin by changing the dollar itself, or even what stands behind it, but by changing the rails through which it moves?

That is the argument we make in March’s issue of VMF’s Strategic Asset Allocation, and it is why this second installment matters so much.

Most investors still imagine the next monetary reset in the old language of gold, devaluation, and dollar decline.

We are asking a different question. What if this Fourth Turning’s reset turns out to be digital, blockchain based, and crypto in nature? What if the next phase of monetary power is not built against the dollar, but around new rails that extend its reach?

And what if Washington is already telling you exactly that?

After all, they called it the GENIUS Act.

Almost as if the name itself were trying to give the game away.

Because that law may prove to be far more than a crypto footnote. It may one day be remembered as an early blueprint for the next monetary architecture: private-sector innovation, Treasury-backed stablecoin rails, and a distinctly American attempt to digitize trust without surrendering control.

Yes, that is a contrarian claim.

But then again, so was our view that energy stocks were the quintessential contrarian trade at the start of 2026. We’re comfortable standing apart from consensus, because that is usually where the asymmetry is greatest and where the crowd is slowest to look.

That is what this section explores.

In “A Fourth Turning Goes On-Chain,” we move from historical pattern to modern mechanism. From the recurring logic of monetary reset to the possibility that this one may unfold through stablecoins, blockchain rails, and a new infrastructure of trust.

Here is Part 2.

If the previous Fourth Turnings rewrote what stood behind the money, this one may end up rewriting how the money moves.

That is the leap.

And yes... it is a big one.

Most investors still imagine monetary resets the old way. They think in terms of devaluations, gold confiscations, fixed exchange rates, reserve-asset changes, and central-bank decrees. Fair enough. History gives them plenty of reasons to think that way.

But what if this time the reset does not begin by changing the unit of money... but by changing the rails through which that money circulates, settles, and extends its reach?

That, in essence, is our working hypothesis.

Last summer, in Alpha Tier, we argued that the GENIUS Act1 was historic.

We said it wasn’t “just about crypto.” We said it was about money. About power. About the United States choosing, quite deliberately, to bless private-sector stablecoin innovation rather than pursue a central bank digital currency.

At the time, that argument may have sounded bold. Today, with the benefit of a few more months of reflection, we believe it may have been even more important than we first realized.

Because in the context of this issue’s broader theme, the GENIUS Act looks less like a niche digital-asset bill... and more like a possible early blueprint for this Fourth Turning’s monetary reset.

That’s a serious claim. So, let’s build it carefully.

To begin with, what exactly is the United States doing here?

It is not launching a CBDC. It is not asking the Federal Reserve to issue retail digital dollars directly to the public. And it is not trying to smother blockchain-based money under an impossible regulatory burden. Quite the opposite.

Washington has chosen a distinctly American path: let the private sector build the infrastructure... but make sure the infrastructure is dollar-based, Treasury-backed, regulated, auditable, and fully embedded within the broader U.S. financial system.

That choice matters enormously.

It means the United States is not trying to defeat private digital money. It is trying to harness it.

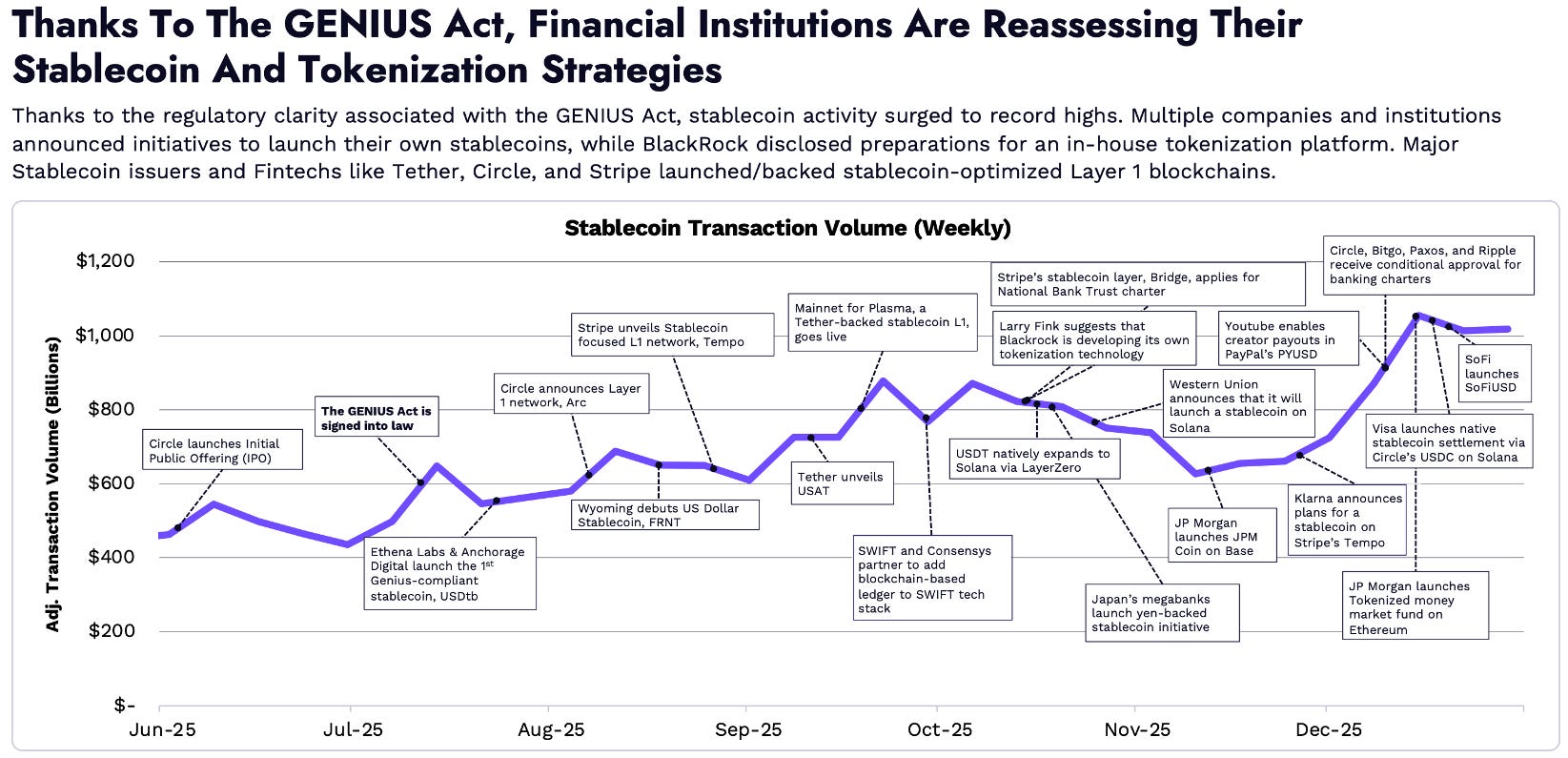

This chart, taken directly from ARK Invest’s Big Ideas 2026 presentation, highlights some of the most important milestones in the adoption of stablecoins:

And that is where Brent Johnson’s recent work becomes so interesting.

Johnson has made the case that stablecoins may prove as transformative as Bretton Woods or the move off the gold standard. In his framing, the market still treats stablecoins as a crypto side-show, when in reality they may be the embryo of an entirely new monetary architecture.

His key insight is that the private market has already built a parallel system... and now the state is moving to co-opt it, regulate it, and scale it.

In other words, what began as an experiment outside the walls of the traditional system may now become one of the mechanisms through which the traditional system renews itself.

That is a very Fourth Turning idea.

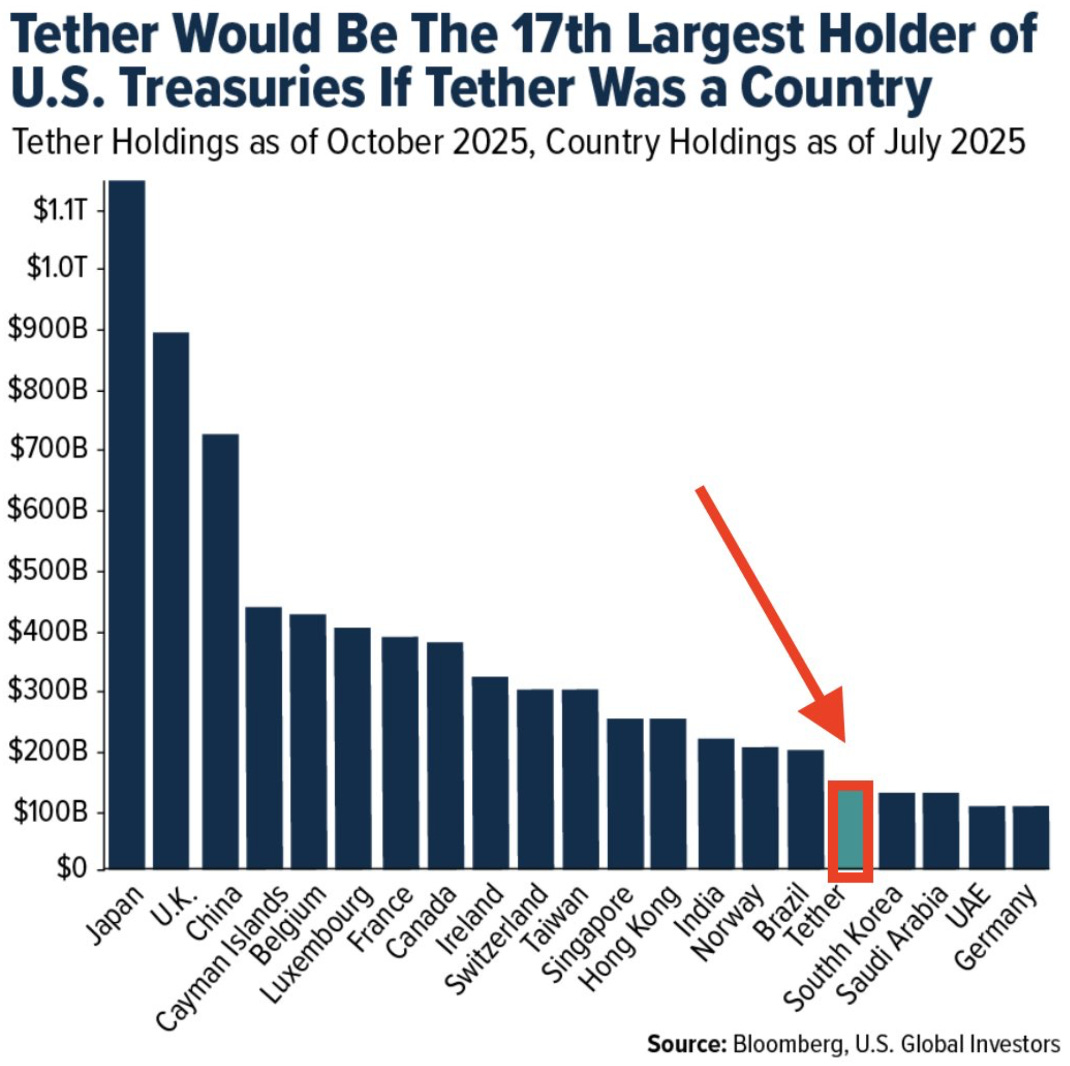

A crisis era does not merely destroy institutions. It forces them to adapt, absorb, and reassert themselves through new forms. Johnson’s stablecoin thesis fits that pattern perfectly. In his view, stablecoins are not just a source of incremental Treasury demand.

They are potentially the next rail of dollar hegemony: a digital infrastructure layer through which the dollar can travel faster, farther, and more efficiently than before... perhaps even reaching millions of people globally who cannot access traditional dollar banking today.

Pause there for a second.

If that sounds like a kind of monetary renewal, that’s because it is.

But Johnson is not the only one thinking in these terms.

Michael Every2 takes the same core phenomenon and pushes it into even more explicitly geopolitical territory. His argument is not simply that stablecoins are new plumbing. It is that they may become a new instrument of economic statecraft. He does not see the endgame as a CBDC either.

In fact, he sees something closer to a revival of private money operating under the shadow and protection of imperial power... much like the old sterling-bill system before the First World War.

In that world, private instruments carried the monetary influence of the hegemon far beyond its borders, lubricating trade and finance while reinforcing the center’s dominance.

That analogy is powerful.

Because if Every is even partially right, then dollar stablecoins are not just about modernizing payments. They are about extending the dollar zone itself.

A user in an unstable local currency converts savings into a dollar stablecoin. The issuer of that coin, in turn, holds cash and short-dated U.S. government paper. The demand for the coin becomes demand for dollars. The demand for dollars becomes demand for Treasury bills. And the rails carrying those claims increasingly sit within a U.S.- regulated architecture.

That is more than innovation.

That is monetary gravity.

And this is why we keep returning to the phrase Infrastructure of Trust.

In every previous reset we examined, the ultimate question was some variation of: what stands behind the money? In the Continental era, the answer was too little. In the Greenback era, the answer became the fiscal and military capacity of the Union state.

In the Bretton Woods era, the answer was the full weight of American balance-sheet strength, gold reserves, and postwar power.

Now the question may be evolving.

Not away from trust... but toward a different layer of it.

In this Fourth Turning, the decisive question may become: through what infrastructure does trust move?

And that is exactly where stablecoins enter the picture.

They do not replace the dollar. They may re-embed it.

They do not overthrow the existing order. They may help extend it.

They do not necessarily create a new reserve asset. They may create a new settlement architecture for the existing one.

That distinction is everything.

Because if this thesis is right, the next monetary reset may not come through the “death of the dollar,” as so many now assume... but through the digitization of its distribution.

A new layer gets built on top of the existing system. A parallel set of rails emerges. At first it looks niche. Then useful. Then strategic. Then indispensable...

And by the time the crowd recognizes what has happened, the architecture of the system has already changed.

Now, let’s be clear: none of this means we should abandon nuance. There are legitimate objections, and we should state them plainly. Jim Bianco, for example, has pushed back against the simplistic version of the stablecoin story.

He is right to do so. Not every dollar that migrates into a stablecoin is necessarily “new” demand for Treasuries in a meaningful macro sense. Some of it may simply be money rotating out of banks or money market funds and into another wrapper.

He is also right to note that stablecoins, today, still serve a heavily crypto-native function.

Much of the activity remains tied to trading and on-chain liquidity rather than mainstream payments.

Fair points.

But those objections, in our view, refine the thesis more than they destroy it.

Because great monetary transitions never arrive all at once, fully formed, with unanimous approval and perfect adoption metrics. They begin at the margin. They grow through utility. They attract regulation once they become too important to ignore. And then, under the pressure of a larger crisis, they can be elevated from innovation to necessity.

That is precisely why this story belongs in a Fourth Turning framework.

The GENIUS Act did not guarantee that stablecoins become the next monetary order. But it did something very important: it moved them out of the realm of regulatory ambiguity and into the realm of national strategy. It effectively said: if these rails are going to exist, they will exist in a form that serves the dollar, supports Treasury demand, and keeps the United States at the center of the system rather than at its margins.

That is not a trivial choice.

That is a strategic one.

And it is made even more interesting by contrast. Europe’s instinct is more centralized, more bureaucratic, more defensive of the official currency. China’s instinct is more overtly state-led, more surveilled, more command-and-control. The American instinct, by contrast, is to unleash private builders... but direct them toward public objectives.

That may prove to be an extraordinarily powerful model in a world where speed, innovation, and geopolitical leverage increasingly matter more than technocratic neatness.

So, where does that leave us?

Our working hypothesis is this: the monetary reset of this Fourth Turning may not arrive first through a formal devaluation, a new gold peg, or a Bretton Woods style conference. It may arrive through the rise of regulated, Treasury-backed stablecoin rails that extend the reach of the U.S. dollar into the next era of global finance.

If that happens, the implications are profound...

It would mean that the United States had found a way, once again, to turn crisis into renewal.

It would mean that in an era of rising debt and open challenges to dollar hegemony, Washington had engineered a market-friendly mechanism to create more demand for its own liabilities while strengthening the global utility of its currency.

It would mean that blockchain technology, far from overthrowing the system, had been partially absorbed into the service of the system.

And it would mean that this Fourth Turning, like those before it, was once again pushing monetary authority toward a more centralized and more expansive form... only now through digital rails rather than through bank charters, gold decrees, or treaty conferences.

That is why we believe this topic matters so much.

Not because stablecoins are fashionable.

Not because “crypto” sounds exciting.

And not because every tokenized dream will come true.

But because, for the first time, we can plausibly sketch the anatomy of what a modern monetary reset might actually look like.

And it doesn’t look like the last one.

It looks digital.

It looks private-sector driven.

It looks Treasury-backed.

It looks blockchain-native.

And, above all, it still looks unmistakably... American.

That, of course, is not the consensus view.

The consensus today is furiously rotating out of U.S. assets, questioning dollar hegemony with renewed conviction, and crowding ever more aggressively into the obvious beneficiaries of monetary disorder... precious metals above all. We understand why. Gold has earned that respect.

Our own Model Portfolio has benefited handsomely from that reality.

But if our working hypothesis is correct, then the next monetary reset may not be nearly as straightforward as the crowd imagines. It may not weaken the United States as decisively as many now expect. And it may not bypass crypto rails in favor of a purely analog hard-money response.

That is what makes this view so contrarian.

It is contrarian because it suggests that, in the middle of a broad consensus turn against the U.S., America may yet find a way to reassert monetary power through a new architecture of trust.

It is contrarian because it suggests that blockchain rails (far from being peripheral to the next reset) may sit close to its very core.

And it is contrarian because it asks investors to look past today’s crowded winners and consider whether some of tomorrow’s biggest beneficiaries still sit in the less loved corners of the field.

As you know, we have seen this movie before. Many of the theses we have shared in these pages over the past two years looked premature, eccentric, or outright unfashionable when first introduced... only to be validated later, and often violently, by the market itself.

So, what does this mean for our Model Portfolio?

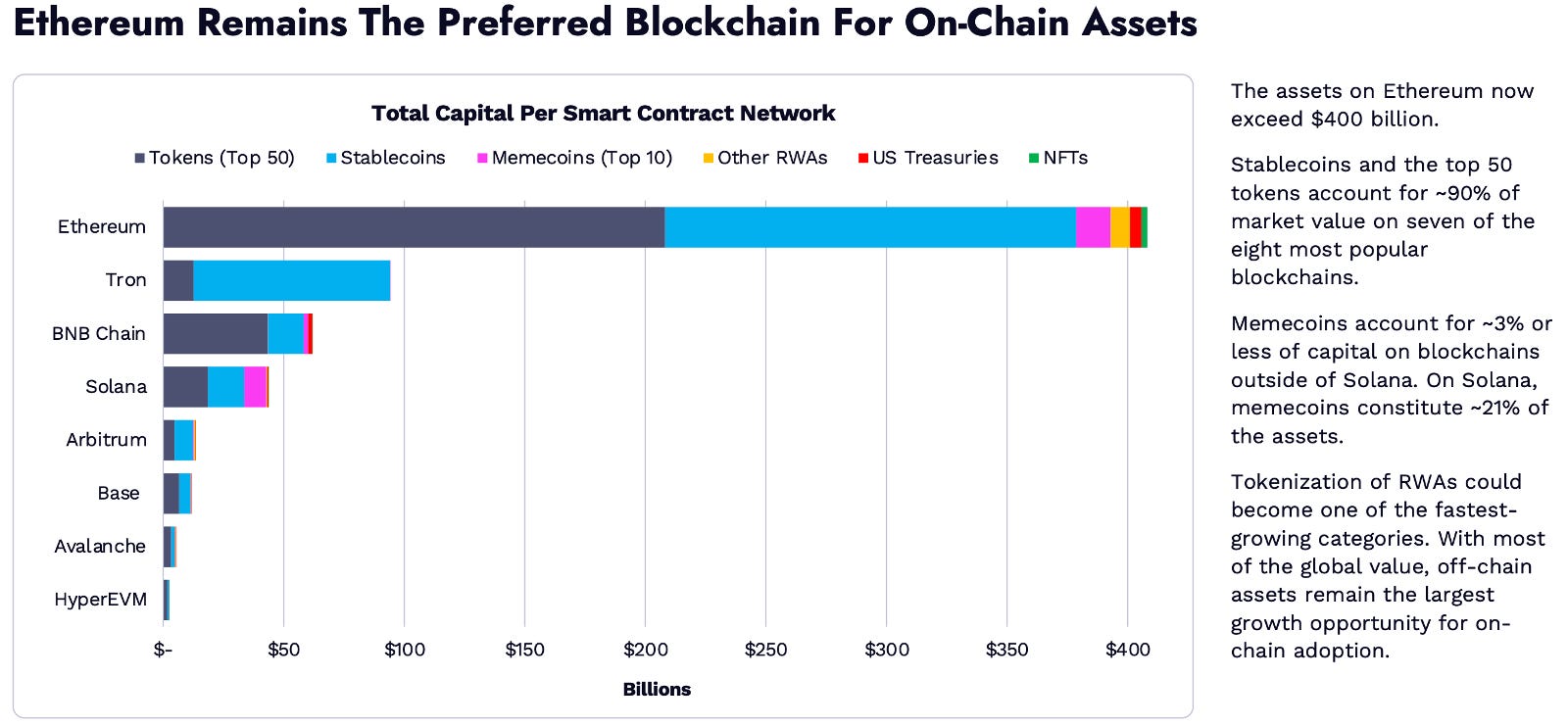

Above all, it reads as a powerful endorsement of crypto rails... and of Ethereum in particular. Just revisit the charts from the last few pages, especially the one on page 10: the message is hard to miss. When it comes to stablecoins, the market is already showing a clear preference for Ethereum’s ecosystem.

And that matters enormously. If stablecoins are indeed emerging as the compliant, Treasury-backed bridge between the old financial system and the next one, then the networks most leveraged to tokenization, settlement, and on-chain financial infrastructure deserve renewed attention.

In that sense, this is not just a macro thesis. It is also a thesis update on one of the few pockets of relative weakness in our current Model Portfolio. And let us be very clear: our conviction there has not faded. If anything, after the work we have just done in this issue, it is stronger than ever.

But this section was never only about crypto.

It was also about extending our understanding of where we stand in the Fourth Turning itself. Because if we are right that this Crisis era is moving closer to its monetary climax, then there may also be room to align the Model Portfolio even more precisely with the phase of the generational cycle we are now entering.

In other words, the implications of this framework do not end with stablecoins, Ethereum, or blockchain rails. They stretch into the broader question of how a portfolio should be positioned when history begins to accelerate, when old anchors weaken, and when the infrastructure of trust starts to shift beneath our feet.

And that is exactly what we will do next.

You might also like reading:

Looking for where to start?

The GENIUS Act, signed into law on July 18, 2025, created the first federal regulatory framework for payment stablecoins in the United States. At its core, the law requires stablecoins to be backed one-to-one by highly liquid assets such as U.S. dollars and short-term Treasuries, while imposing reserve, disclosure, and supervisory standards designed to make those digital dollars more trustworthy and scalable. In practical terms, it marked Washington’s decision to embrace private-sector stablecoin innovation rather than pursue a central bank digital currency, while also reinforcing the global role of the U.S. dollar. We dedicated the July 2025 issue of Alpha Tier to this milestone because we believed, even then, that it was not just a crypto story... but a monetary one.

Michael Every is a global strategist at Rabobank and one of the more distinctive macro thinkers writing today on geopolitics, monetary fragmentation, and economic statecraft. His work goes well beyond traditional economics, focusing instead on how trade, sanctions, industrial policy, reserve currency politics, and strategic rivalry are reshaping the global financial order. In practical terms, he is especially useful for investors trying to understand the world not as a frictionless market system, but as a contest for power in which money, trade, and geopolitics increasingly overlap.