Who Gets Paid When Trust Moves

Beyond the Exchange: Why Coinbase is evolving into the regulated financial operating system of the Fourth Turning.

Over the last few weeks, if you’ve been reading this Substack, you’ve already seen the pieces of the puzzle:

In “A Fourth Turning Goes On-Chain,” I argued that the next monetary reset may not begin with gold, devaluation, or some theatrical Bretton Woods sequel. It may begin by changing how trust moves.

In “The Agentic Era,” I argued that once software becomes a doer, blockchains stop looking like a speculative sideshow and start looking like the rails for identity, settlement, and machine-to-machine commerce.

Fine.

But ideas, by themselves, do not pay.

Businesses do.

That is why this new post matters.

What follows is an excerpt from March’s issue of VMF’s Security Selection, and in my view it is one of the most actionable pieces of work we’ve published in some time.

Because it takes the broader research we’ve been building across our entire product roster and pushes it one level deeper, from macro thesis to business model, from “how trust moves” to the only question investors should really care about:

Who gets paid?

Our answer is COIN 0.00%↑

Yes, Coinbase.

Most investors still look at it and see what they expect to see: a cyclical crypto exchange tied to sentiment, speculation, and trading volumes. We think that lens is already stale.

The market is still pricing the old business while the company is trying to become something much larger: the regulated financial operating system of the on-chain dollar, what Brian Armstrong calls the “Everything Exchange.”1

That is the leap this thesis makes.

If our work across VMF’s Strategic Asset Allocation, VMF’s Security Selection, and Alpha Tier is right, then Coinbase is not merely a levered bet on the next crypto bounce. It may be one of the clearest public-market tollbooths on a much bigger shift: Treasury-backed stablecoin rails, blockchain-based settlement, and even the early financial plumbing of the agentic internet.

That is not the consensus view.

But then again, that is usually where the asymmetry is greatest.

Here’s the excerpt:

If last week’s Tier One issue was about how trust moves, this one is about who gets paid when it does.

That is the leap.

Because once you accept the possibility that this Fourth Turning’s monetary reset may not arrive first through a dramatic devaluation, a new gold peg, or some new Bretton Woods-style conference... but instead through new rails for moving, settling, and extending trust... the exercise changes.

You stop asking which token might catch the next speculative wave.

You stop asking which blockchain narrative sounds the most futuristic.

And you begin asking a much more practical question... and, in our view, a much more investable one: which businesses are positioned to own, monetize, and defend the new infrastructure of trust?

We believe Coinbase - COIN 0.00%↑ may be one of the clearest answers in the entire public market.

That may sound odd at first, because most investors still look at Coinbase and see what they expect to see: a crypto exchange. A cyclical, sentiment-driven business that booms when trading is hot and suffers when speculation cools.

That caricature is not entirely wrong. But it is increasingly incomplete.

The market is still looking at Coinbase through the old lens. But make no mistake, even if Coinbase were nothing more than a crypto exchange, it would still be an increasingly bigger and more dominant one.

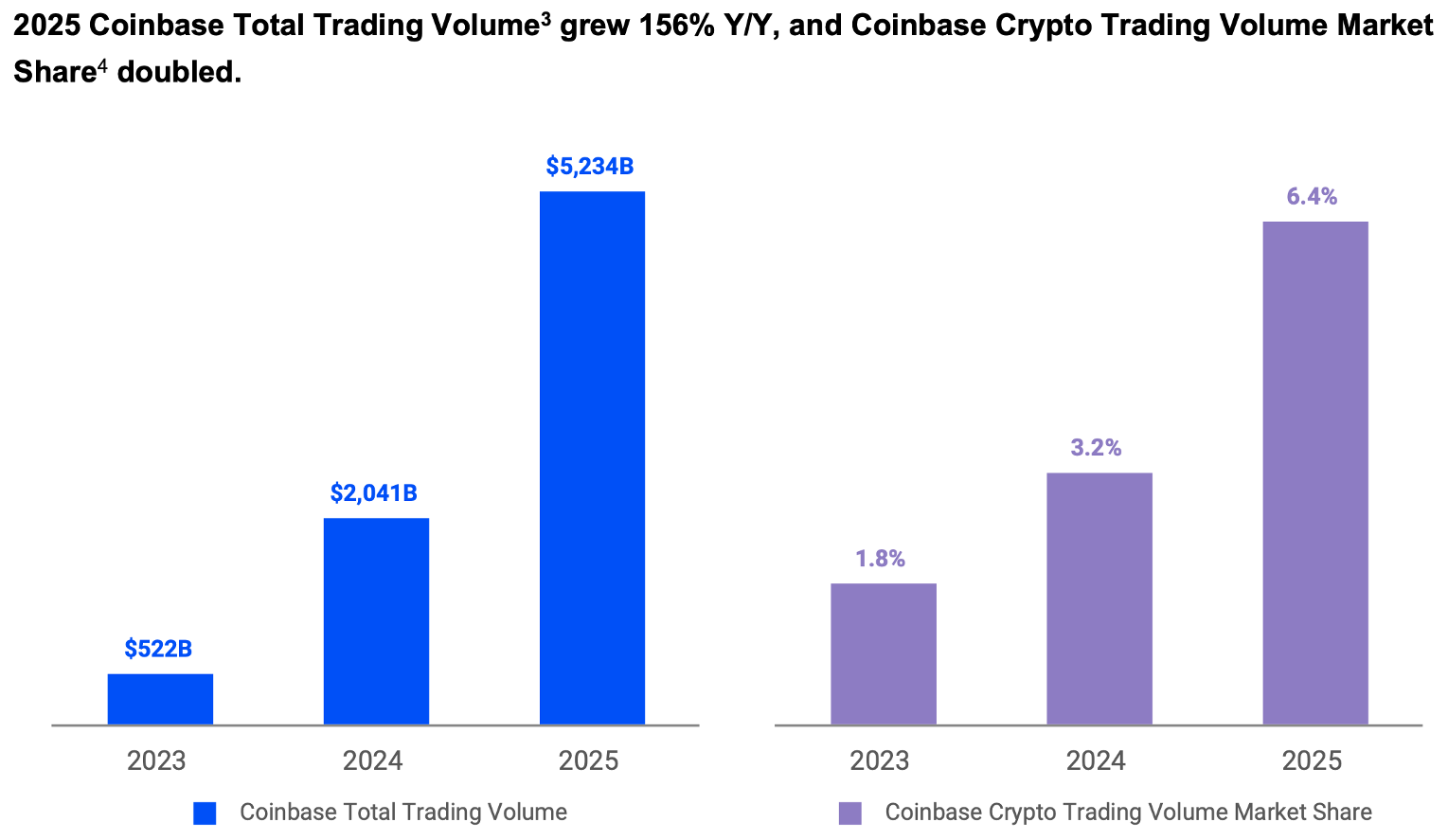

The chart above makes that hard to ignore. Total trading volume has surged from $522 billion in 2023 to $2.0 trillion in 2024 and then to $5.2 trillion in 2025.

At the same time, Coinbase’s crypto trading volume market share has climbed from 1.8% to 3.2% and now to 6.4%. So yes, the market may still be looking at Coinbase through the old lens... but even that “old” business is scaling fast and taking meaningful share.

Still, we think the more important perspective is this: Coinbase is trying to become the regulated financial operating system of the on-chain dollar.

Or, in Brian Armstrong own words, the “Everything Exchange.”

That ambition matters enormously.

Because the Everything Exchange is not simply a bigger crypto venue. It is an attempt to make Coinbase the single trusted place where customers can hold assets, move money, earn yield, access custody, use stablecoins, trade spot and derivatives, and, over time, manage a much broader universe of financial products inside one compliant ecosystem.

Coinbase has explicitly made the expansion of the Everything Exchange one of its three key priorities for 2026, alongside scaling stablecoins and payments and bringing more of the world on-chain through Base, a topic we will address in just a moment.

And it is precisely here that we believe the market’s business-model misdiagnosis is most severe.

An exchange, at least in the way the consensus still thinks about Coinbase, earns fees when people trade. A financial operating system does something far more valuable than that.

It becomes the place where assets sit, where trust accumulates, and where more and more economic activity can be layered on top. It provides custody. It embeds compliance. It distributes stablecoins. It connects wallets. It settles transactions. It monetizes balances. It finances activity. It gives institutions, merchants, developers, and increasingly even AI agents2 a way to interact with the system without needing to understand every layer beneath it.

That is a far better description of what Coinbase is trying to build. And if that is the right description, then the stock belongs in a very different category from the one the market still seems intent on assigning to it.

The clearest proof that the Everything Exchange is more than a clever slogan is the sheer amount of gravity Coinbase has already built.

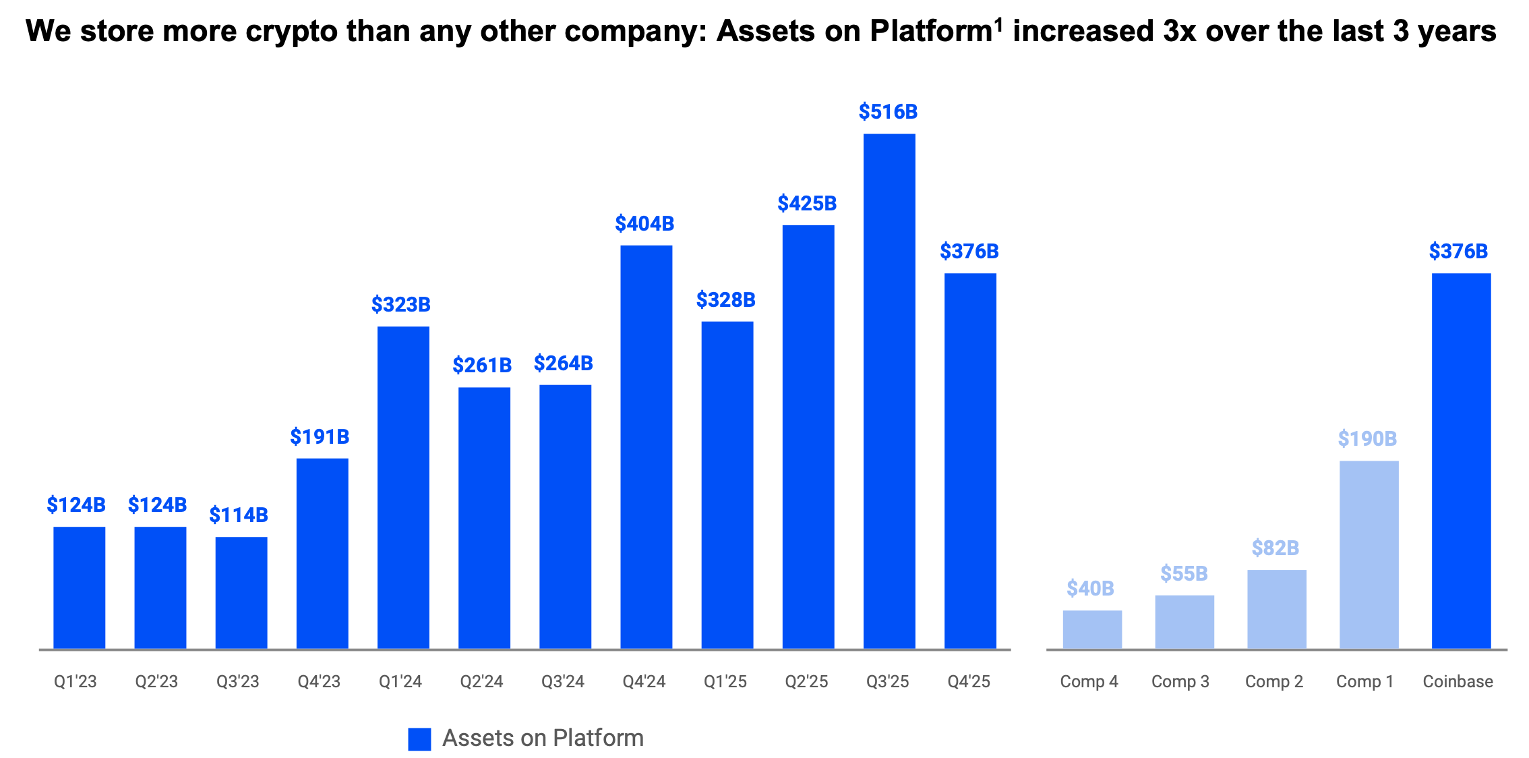

Even after a brutal drawdown in crypto prices, with Bitcoin roughly halved from its late 2025 peak and many other major assets hit even harder, Coinbase still finished the fourth quarter with assets on platform close to $380 billion. And that figure is not just large in absolute terms.

It is enormous in relative terms...

As the company’s own chart makes clear, Coinbase now holds roughly twice the assets of the next-largest rival. Management went even further on the latest earnings call, stating that Coinbase stores more crypto than any other company in the world, roughly 12% of all crypto globally, and more than the next four competitors combined.

That is not what a commodity exchange looks like. That is what platform-level trust looks like.

And this is precisely why the flywheel matters so much.

Coinbase is not simply trying to maximize fee extraction on trading volume. It is trying to become the place where assets accumulate first, because once the assets are there, everything else becomes easier. Trading becomes easier. Borrowing against those assets becomes easier. Staking becomes easier. Stablecoin usage becomes easier. Payments, subscriptions, custody, derivatives, and, over time, a much broader universe of financial services all become easier.

That is the real strategic logic behind what management calls the “asset accumulation flywheel.” Build trust. Attract assets. Layer more utility on top of those assets. Reinvest the economics into better products, broader distribution, and even more trust.

It is a simple idea. But when it works, it is extremely powerful.

This is where Base becomes so important.

Base is Coinbase’s Layer 2 network built on top of Ethereum. That means it is designed to inherit Ethereum’s security and settlement layer while making onchain activity faster, cheaper, and easier to use. That matters because if Ethereum is the base monetary and settlement substrate, then Base is Coinbase’s attempt to sit much closer to the application layer where real usage, developer activity, and customer relationships actually form.

The latest shareholder letter makes clear that Base is not a side project. Coinbase says it has made the network materially faster and cheaper, with roughly 200 millisecond block times and very low median fees, while also bundling wallet, onchain trading, payments, messaging, identity, mini apps, and Base Pay inside the broader Base App experience.

That is not what a company does when it wants to remain “just an exchange.” That is what a company does when it wants to own more of the stack.

And once you see Base in that context, the whole business starts to look different.

The market still tends to think about Coinbase as if the company’s economic relevance begins and ends with trading activity. But Base levels the company up into something much broader. It gives Coinbase a direct claim on the growth of onchain applications, onchain payments, embedded wallets, consumer identity, developer tooling, and the wider ecosystem forming on top of Ethereum.

In other words, it turns Coinbase from a venue into a platform. And platforms, when they work, are worth much more than venues.

You can also see this evolution in the number of products Coinbase now sells and the pace at which they are growing.

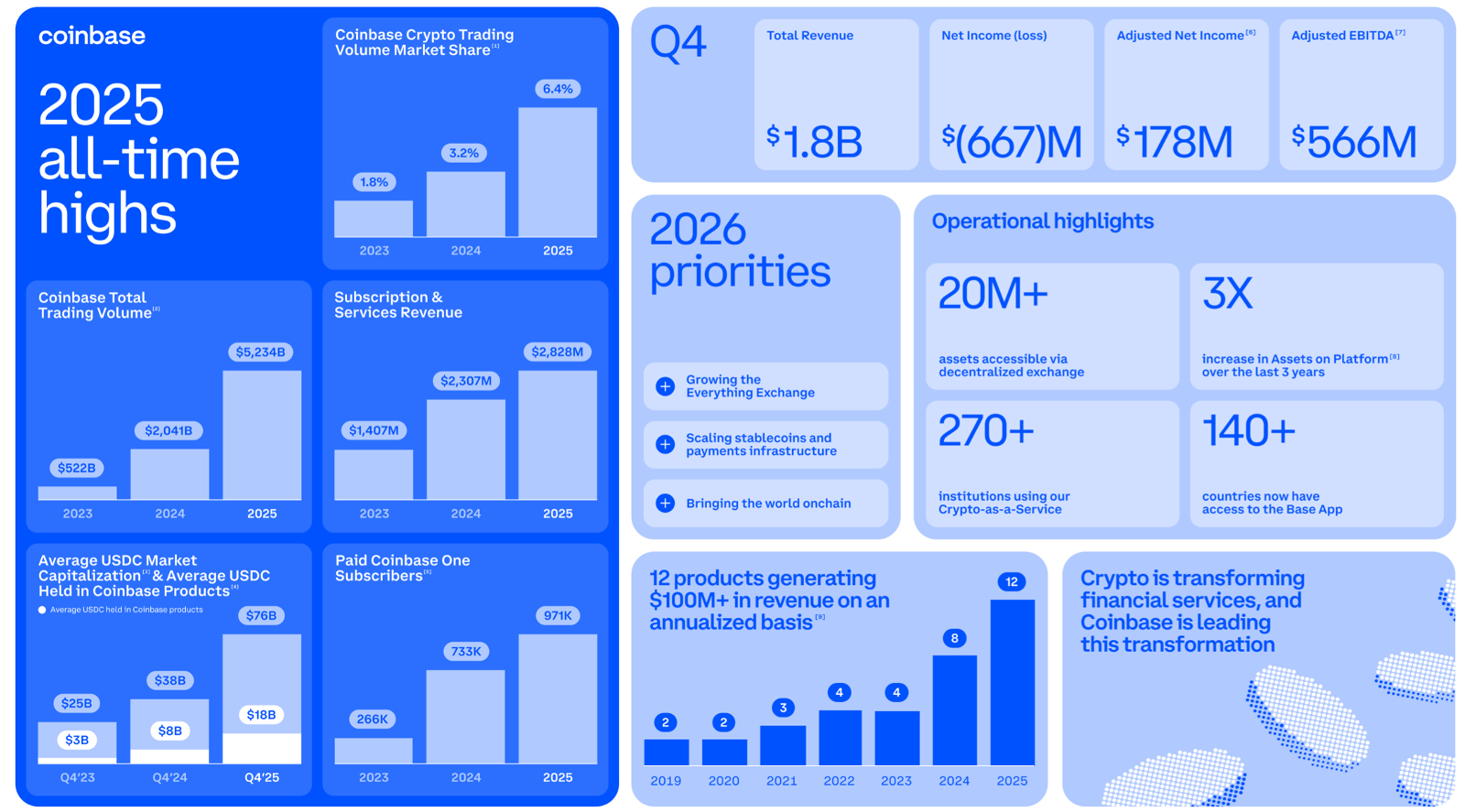

The company says it now has 12 products generating more than $100 million in annualized revenue, half of which generate more than $250 million, and two above $1 billion.

Read that again.

This is not a single-product company riding one cyclical tailwind. It is a business whose product surface is widening quickly across spot trading, derivatives, custody, subscriptions, staking, financing, USDC, payments infrastructure, and developer rails.

The same letter also highlights nearly 1 million paid Coinbase One subscribers, a growing Prime financing business, all-time highs in derivatives volume, strong growth in BTC-backed borrowing, and deeper integrations of USDC across both consumer and institutional products. That breadth matters because it makes the business more resilient and more valuable. A customer holding assets on Coinbase is no longer just a potential trader. That customer is increasingly a candidate for multiple layers of monetization.

One emerging area we find especially promising is AI agents.

We wrote in the last issue of Alpha Tier that the agentic era strengthens the blockchain case... and Coinbase is one of the few public companies already building for that world in a serious way.

The basic logic is straightforward:

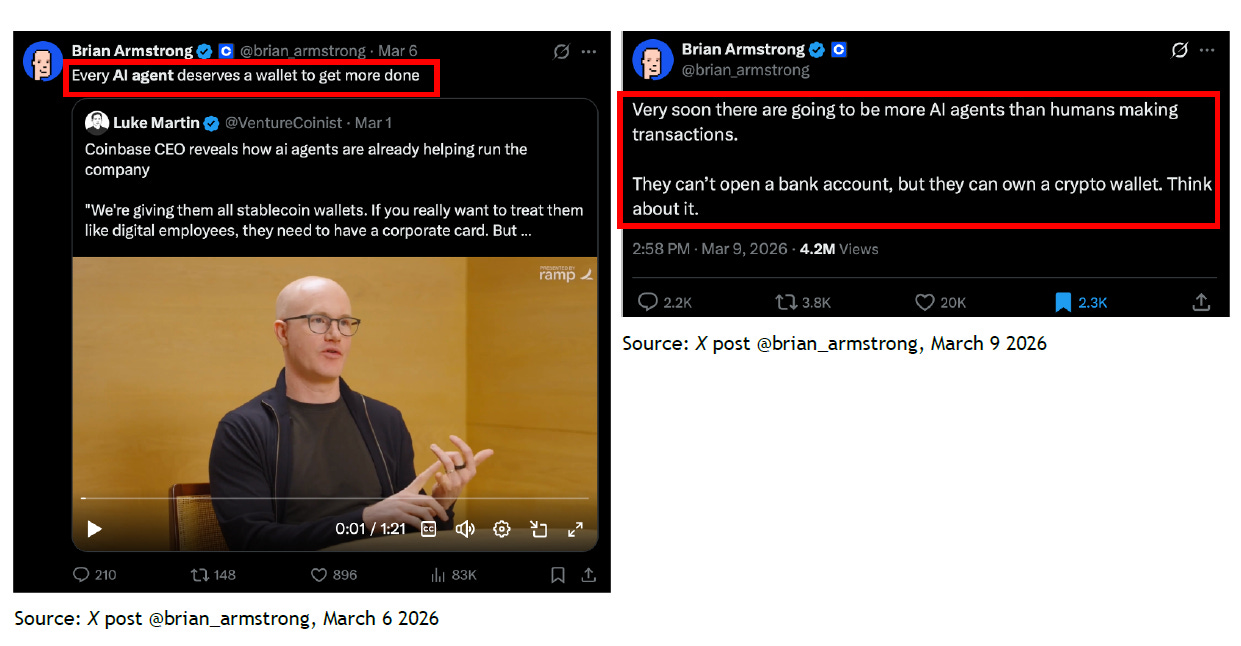

If AI agents become real economic actors, and we believe they will, they will need a native way to hold value, make payments, and interact with services across the internet. They will not open traditional bank accounts.

But they can have crypto wallets.

And Coinbase is already building exactly that infrastructure. Through products such as Agentic Wallets, AgentKit, Payments MCP, and x402, the company is explicitly trying to give software agents the ability to hold stablecoins, pay for services, and transact programmatically over crypto rails. x402, in particular, is designed to let both humans and machines make instant stablecoin payments directly over HTTP. That is not a science-fiction use case.

That is the early financial plumbing of the agentic internet.

And that matters because, over time, there may be far more AI agents than humans online.

If that happens, then the world will need a machine-native payment and settlement layer.

We are still early, and we should not pretend that this is yet a major line item in Coinbase’s income statement. But that is not the point. The point is that the company is already building for a future in which autonomous software becomes a genuine economic participant. That gives Coinbase a valuable growth option embedded inside a business that is already getting stronger on much more traditional metrics.

Of course, there are other promising avenues we could spend time on here. Tokenization is one. Prediction markets are another. We could easily go there. And we probably will in future issues. But not today.

For now, we think the cleanest and most useful way to see Coinbase is this: not as a “crypto stock,” and certainly not as a mere exchange, but as a platform. Better yet, as a tollbooth on crypto adoption.

That is the key.

Because if we are right in our broader macro thesis that this Fourth Turning’s monetary reset ultimately proves supportive for crypto, then Coinbase stands out as one of the clearest corporate beneficiaries of that secular trend. It would benefit not only from higher prices and stronger activity, but from deeper stablecoin penetration, broader onchain payments usage, more tokenized assets, richer developer ecosystems, and a more central role in the financial rails of the next regime.

But... and that is exactly what makes this thesis so robust...

...even if our big macro call proves too early, too partial, or simply wrong, we still believe Coinbase can continue to grow in an increasingly digital world where AI agents play a larger role, financial activity keeps migrating online, and customers increasingly gravitate toward asset platforms that combine trust, custody, utility, and product breadth inside a single ecosystem.

In other words, the macro thesis makes the upside bigger.

But it is not the only thing holding the thesis together.

And now, as if to underline that point, the incumbents are beginning to validate the category for us.

The parent of the New York Stock Exchange, ICE, has just taken a minority stake in OKX at a $25 billion valuation and paired that investment with a strategic partnership around crypto futures, tokenized equities, custody, and wallet architecture.

Nasdaq has also partnered with Kraken to develop tokenization infrastructure for blockchain-based equities.

Those are not fringe actors chasing a fad...

They are two of the most important market-infrastructure franchises in the world, and both are now moving toward crypto-native platforms. That is a meaningful tell. It suggests that what we are describing here is not some niche corner of the market, but the early construction of a new financial architecture.

So yes, Coinbase still gets mislabeled as an exchange. And yes, the cycle will still matter. But the more we study the business, the harder it becomes to see it through that narrow lens alone.

The better way to think about it is this: Coinbase is building a flywheel in which trust attracts assets, assets attract utility, utility attracts more activity, and that activity funds the continued expansion of the platform.

If that flywheel keeps turning, then what looks today like a cyclical crypto business may, in hindsight, prove to have been one of the most important public tollbooths sitting on top of crypto adoption all along.

We believe we have made our view quite clear.

We like Coinbase’s competitive position. We like its value proposition. And above all, we like Brian Armstrong’s vision for what the business can become.

Therefore, at this stage, only two questions remain:

• How much are we paying for that business?

• And is the stock suffering from the same kind of market myopia we are seeing in so many other names we like right now... poor price action despite a business that keeps getting stronger?

Let’s begin with valuation.

We have just spent the last several pages arguing that Coinbase is not simply an exchange. It is something much broader and much more strategically important than that. Still, the cleanest place to start is to compare it with the incumbents the market already knows how to value.

And frankly, Coinbase shines against all of them.

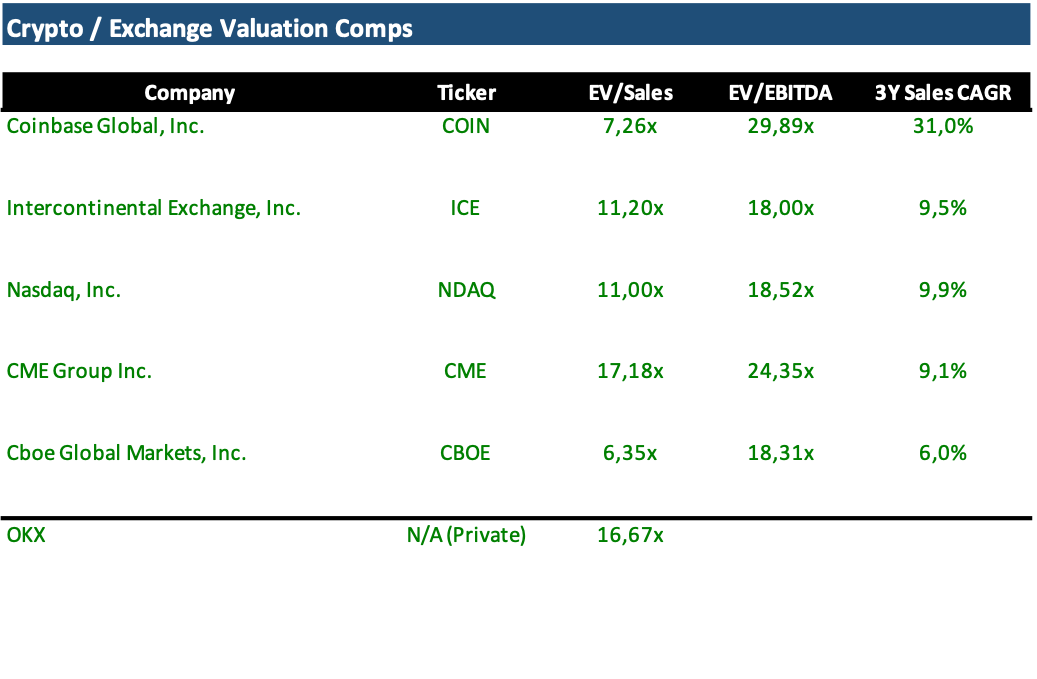

Start with the top line.

As the table above shows, Coinbase is growing much faster than the traditional exchanges. A lot faster!

Over the last three years, revenue has compounded at roughly 31% annually, versus about 10% for Nasdaq, 9.5% for ICE, 9.1% for CME, and just 6% for Cboe. No wonder ICE, the parent company of the New York Stock Exchange, has now decided to invest in OKX. And look at the valuation it was willing to bless. Based on the reported $25 billion valuation and the best available outside estimate of roughly $1.5 billion of revenue, the market is implicitly valuing OKX at around 16.7x sales.

Now here is where it gets even more interesting.

For those same growing sales, the market is actually paying a discount for Coinbase versus most of the traditional exchanges. Coinbase currently trades at roughly 7.3x EV/Sales, compared with about 11.2x for ICE, 11.0x for Nasdaq, and more than 17x for CME. Only Cboe screens lower.

In other words, the market is giving the slow-growing incumbents more credit for each dollar of revenue than it is giving Coinbase. That strikes us as a strange conclusion for a business growing at several times their pace and operating much closer to some of the most important financial trends of the coming decade.

When we turn to profitability, measured here through EBITDA, the picture looks different. Coinbase screens more expensive, trading around 29.9x EV/EBITDA, versus roughly 18x to 24x for the traditional exchange group.

But we believe it deserves that premium...

And the reason is not hard to understand. Coinbase is spending heavily to build the Everything Exchange, expand stablecoins and payments, scale Base, deepen regulation and compliance, and widen the product surface of the platform.

Many of those investments run straight through the income statement as operating expenses, which depresses near-term EBITDA even as they may be strengthening the long-term economics of the business. In other words, current profitability understates the embedded optionality.

In the context of everything we have laid out, and the growth runway we still see ahead, we find the valuation attractive.

And we suspect that premium could crystallize much faster if and when the CLARITY Act passes, because that would make it far easier for the market to value Coinbase as a regulated financial platform rather than as a volatile crypto proxy.

Even today, with the legislation still stalled, that reframing is already beginning.

Now let’s talk about the stock.

Notice the hammer candle Coinbase has just printed. In technical analysis, that kind of price action often signals that sellers managed to push the stock sharply lower during the session, only to see buyers step in aggressively and force a close much higher. When it appears after a prolonged decline and near an important support zone, it can be an early sign that downside pressure is being absorbed and that sentiment may be beginning to turn.

Regarding the technical action of Coinbase’s chart... well, the chart speaks for itself.

The stock is still trading at less than half the intraday high it reached on the day of its April 2021 direct listing, when shares opened at $381 and rose as high as $429.54 in first-day trading.

Today, Coinbase is still only around the low $200s. So... despite all the progress the business has made since then, the stock is still carrying the emotional scar tissue of the previous crypto bull market.

And... let’s be frank, the stock has not exactly covered itself in glory relative to the broader opportunity set. It has lagged the great benchmark indices (like the S&P500 or the Nasdaq) and, more importantly for our purposes, it has lagged the major Bitcoin, Ethereum or Solana).

Coinbase has underperformed... that’s a fact, but that is also the point. The business has grown massively across multiple fronts, but the stock has not yet fully reflected that transformation.

That disconnect is exactly what interests us.

Because when the crypto cycle turns, and when today’s depressed sentiment eventually gives way to something more constructive, we believe the market will be forced to look at Coinbase very differently.

Not as a one-dimensional trading venue.

Not as a speculative sidecar to Bitcoin.

But as a platform with custody, stablecoins, subscriptions, derivatives, developer rails, Base, and an increasingly important role in the financial architecture of the next monetary regime. And if that is the lens through which the market eventually learns to see Coinbase, then we believe the stock can reach levels well above the old highs from April 2021.

We will be here to be accountable for that claim.

Let’s allocate 2% of the Quality Model Portfolio to Coinbase COIN 0.00%↑ @ $197.50.

You might also like reading:

The Everything Exchange is Brian Armstrong’s vision of Coinbase as a single platform where users can do far more than trade crypto. In this model, Coinbase becomes the trusted place to hold assets, trade spot and derivatives, use stablecoins, access payments, earn yield, borrow, and eventually manage a much broader universe of financial products inside one compliant ecosystem.

AI agents are software systems designed not just to answer questions, but to take actions on a user’s behalf. Unlike a traditional chatbot, an AI agent can pursue a goal across multiple steps, use tools, interact with applications, retrieve information, make decisions within defined limits, and in some cases even execute transactions. In practical terms, they are closer to digital workers than to search boxes. We wrote extensively about agents on “The Agentic Era”