The Setup for a Dovish Shock

How a 4% Productivity Surge and Changing Supply Dynamics Are Setting Up the Ultimate Fed Repricing for Active Investors.

Headlines are a poor compass.

They tell you where attention has already gone. They rarely tell you where the next mispricing sits.

A new monthly publishing cycle begins at VMF Research with SpaceX SPCX 0.00%↑ dominating the market conversation. That matters to us because both VMF's Security Selection and Alpha Tier have carried exposure to SpaceX since the start of 2026, through a listed vehicle that also provided access to private-market leaders such as Anthropic, Revolut and others.

That is the process in one sentence: identify the theme before it becomes consensus, find the investable vehicle, size the exposure, and manage it inside a portfolio.

June’s issue of VMF’s Strategic Asset Allocation begins somewhere else.

The Fed.

Every great growth story eventually meets the discount rate. SpaceX, Anthropic, software, China internet, crypto, precious metals, long-duration equities, and private-market vehicles all depend, in different ways, on liquidity, inflation expectations, and monetary policy.

And right now, we believe the market may be preparing for the wrong Fed surprise.

That is the point of the excerpt below.

Markets recently treated stronger growth as a problem. Payrolls surprised to the upside, the economy looked resilient, and investors immediately reached for the post-pandemic playbook: stronger growth means more inflation risk, more inflation risk means a more hawkish Fed, and a more hawkish Fed means pressure on risk assets.

That reflex may be stale...

If AI, software, automation, capital spending, and operating leverage are beginning to lift productivity, then stronger growth could carry a very different macro signal. It could give the Fed more room, not less.

That is the setup for a dovish shock.

This also connects directly with the Market View we have been developing over the past few months: AI as an abundance shock, scarcity moving across the stack, visible bottlenecks becoming crowded, and the next opportunity shifting toward less obvious parts of the market.

June’s Tier One issue takes that framework into macro.

The excerpt that follows lays out the evidence, the policy logic, and the assets most exposed if the market has priced the wrong path.

Read it as a macro stress test:

What happens if the next major Fed surprise is a dovish repricing rather than another tightening scare?

Good reading.

Last week, the market gave us one of those moments that reveals far more than a hundred calm trading sessions ever could.

The latest payrolls report came in stronger than expected. On the surface, this should have been good news. A stronger labor market means greater economic resilience, stronger income formation, and a higher probability that the expansion remains intact. That is how markets used to interpret this kind of data.

The reaction was not surprising to anyone fluent in the market’s current policy reflex, but it was revealing enough to prompt Donald Trump to comment publicly...

And yet... markets fell sharply.

Equities sold off. Technology shares were hit particularly hard. Treasury yields rose. Oil climbed. Bitcoin weakened. Precious metals came under pressure. Risk assets moved into a clear defensive posture. What should have looked like evidence of economic strength was instead treated as a threat.

That is the starting point of this month’s issue.

Because when markets react perversely to seemingly good news, the key question is not simply what happened.

The key question is: what framework are investors using to interpret what happened?

The market’s logic was straightforward:

Stronger payrolls imply stronger growth.

Stronger growth implies more inflation risk.

More inflation risk implies a more hawkish Fed.

A more hawkish Fed implies higher yields.

Higher yields imply lower valuations, tighter financial conditions, and pressure on liquidity-sensitive assets.

That was the sequence.

To be fair, it was not irrational. It was the logical extension of the regime investors have been living through since the post-pandemic inflation shock. For the last few years, markets have learned to fear strength. Good news became bad news because strong data threatened to keep inflation alive and force the Fed’s hand.

That framework is now deeply embedded in prices. It explains why strong payrolls triggered a vicious risk-off move. The market did not sell off because growth was weak. It sold off because growth was interpreted as inflationary.

But what if that interpretation is too simple?

What if we are dealing with a different kind of growth impulse?

Over the past few months, we have repeatedly argued that the economy may be entering a phase that strongly resembles the Great Acceleration framework laid out by Cathie Wood and ARK Invest.

For the full context on this framework, read:

This is not a generic bullish slogan. It is a specific macro thesis. The idea is that the U.S. economy may be moving into a phase where growth accelerates not because of a classic overheating cycle, but because productivity is beginning to improve meaningfully. AI, software, automation, capital spending, and operating leverage may be combining to create a different kind of expansion than the one markets instinctively fear.

Not all growth is created equal. Some growth is inflationary. It comes from excess demand, rising wages, supply bottlenecks, and companies passing higher costs through to consumers. But some growth is productivity-driven. It comes from better tools, better systems, better software, better processes, and the ability to generate more output with fewer incremental inputs.

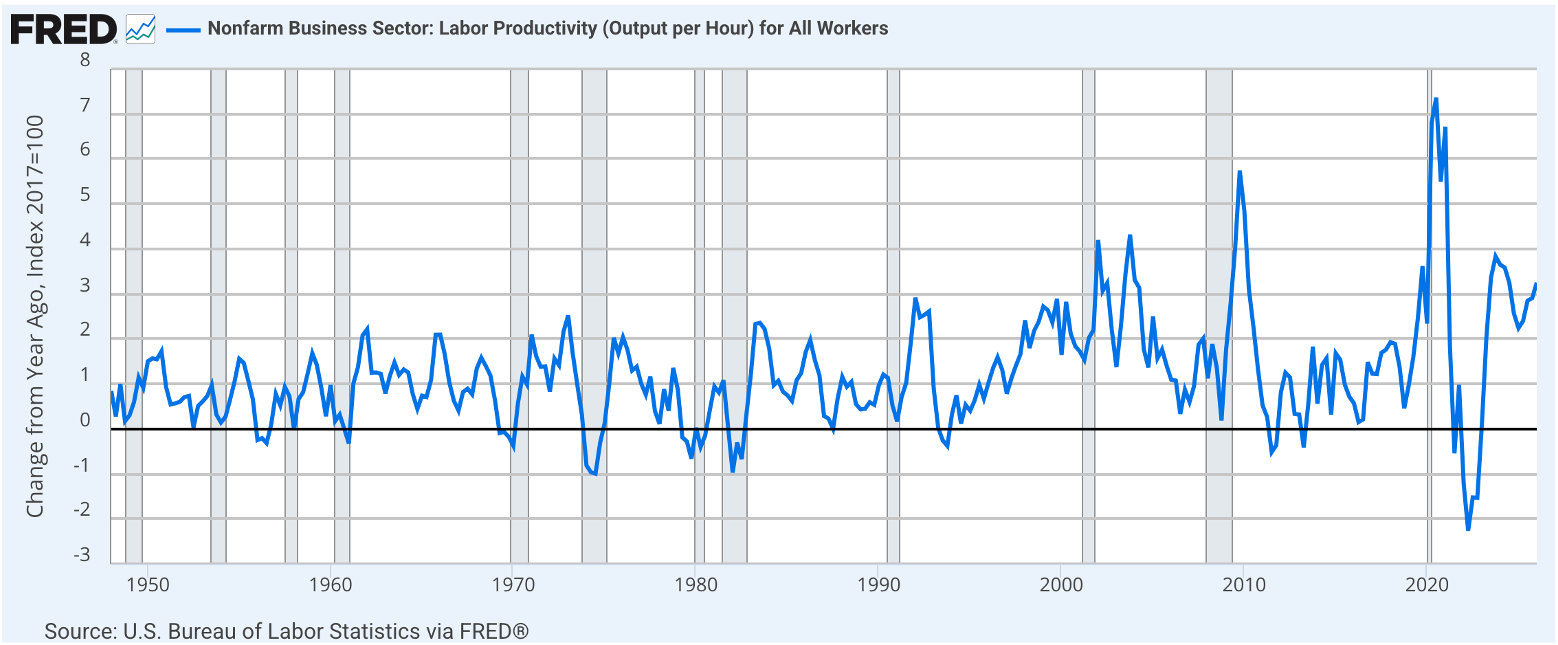

The trough in labor productivity curiously coincides with the public launch of ChatGPT in November 2022. That does not prove causation, of course, and productivity data are volatile and revised over time. But the timing is striking: since then, the productivity trend has turned higher, just as AI adoption, software investment, automation, and capital spending have moved from narrative to implementation.

The first kind of growth forces the Fed to tighten.

The second kind can relieve inflationary pressure.

That is the core of the disinflationary growth thesis. And if we are right, the market may be using an old framework to interpret a new regime.

The previous chart is crucial.

As you can see, labor productivity has turned higher again. The series is volatile, of course, and no serious investor should pretend otherwise. But the broader message is increasingly difficult to ignore: productivity is no longer behaving like the stagnant variable many macro narratives still assume.

The market’s reflex remains deeply tied to a Phillips Curve1 worldview... a worldview in which stronger labor markets automatically create inflationary pressure through wages.

But wages are only part of the equation. The inflationary problem is not simply whether workers earn more. The real problem is whether compensation is rising faster than output. If productivity rises alongside compensation, unit labor costs can remain contained even in a stronger labor market.

That changes the meaning of growth.

A stronger economy with stagnant productivity can become inflationary.

A stronger economy with improving productivity is something very different.

And there is more evidence that this is not just a statistical curiosity.

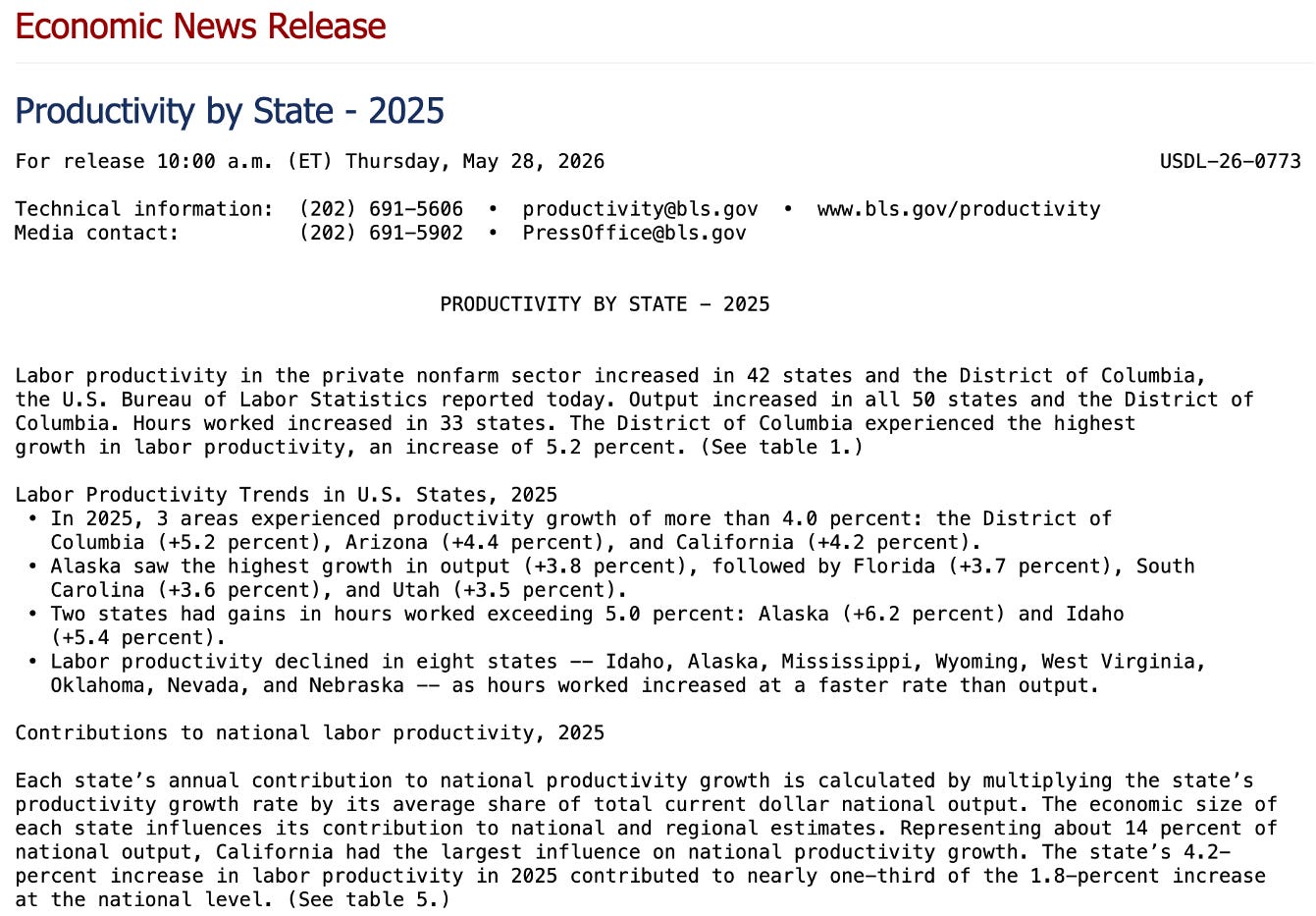

The Bureau of Labor Statistics’ state-level release reinforces the point.

The breadth of the improvement is striking: output increased across the entire country, while private nonfarm labor productivity rose in 42 states. Some of the gains were unusually strong, with the District of Columbia up 5.2%, Arizona up 4.4%, and California up 4.2%.

That last number deserves special attention.

California is not a small regional footnote. It is one of the largest economic engines in the world. When a state of that size delivers productivity growth above 4%, it should not be dismissed as noise.

This does not prove that we are already in a full-blown productivity boom. The data are backward-looking. They are volatile. They can be revised. And productivity cycles are notoriously difficult to identify in real time.

But the evidence is beginning to accumulate.

Productivity is improving in the national data. It is broadening across states. And it is doing so at the same time that AI adoption, software investment, automation, and capital spending are moving from narrative to implementation.

That is no longer merely a story about what might happen someday.

It is beginning to show up in the data.

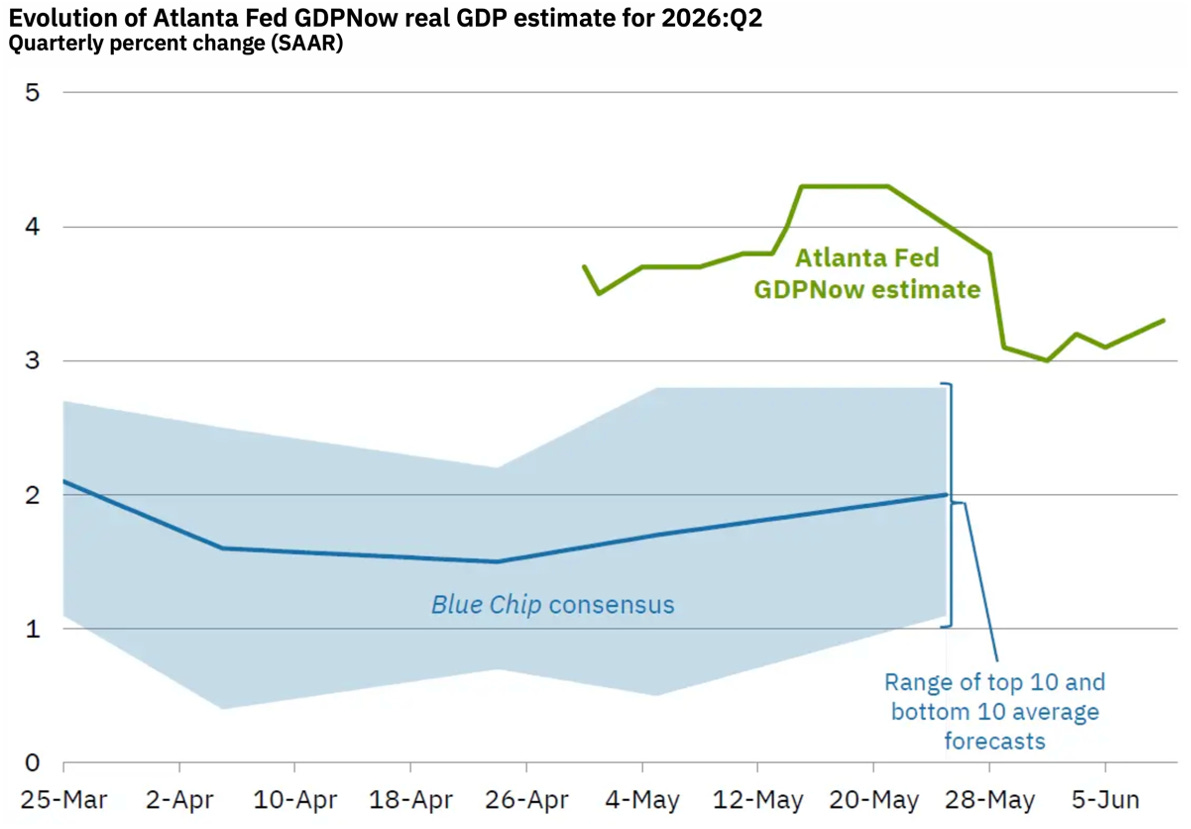

Now add the economic growth backdrop.

The Atlanta Fed’s GDPNow estimate is pointing to real GDP growth well above consensus expectations. The economy is not merely avoiding recession. It is outperforming what most forecasters had penciled in.

Here is where the market begins to panic. If growth is accelerating while the economy is already near full employment, the standard interpretation is obvious: this must be inflationary.

That fear is not unreasonable.

A stronger growth impulse can absolutely become inflationary if it is driven by excessive demand, wage pressure, and tightening capacity constraints. But that is the analytical question, not the conclusion.

Is this growth impulse demand-driven overheating? Or is part of it coming from a supply-side improvement... higher productivity, stronger capital spending, better technology adoption, and greater operating efficiency?

Those two scenarios lead to very different inflation outcomes.

They also lead to very different Fed outcomes.

Which brings us to inflation itself.

If one looks only at the official Consumer Price Index (CPI) narrative, that concern is understandable. The BLS measure is still printing at a level that keeps investors on edge.

But note the divergence with Truflation2.

The Truflation index is running meaningfully below the official BLS CPI. That discrepancy deserves attention.

The two indicators are built differently. The BLS CPI is the official benchmark. It is methodologically structured, widely followed, and crucial for policy, contracts, and market expectations. But it is also slower-moving by design. It relies on survey based collection, fixed methodology, and lagged components (especially shelter, which can keep official inflation elevated even after real-time housing pressures have started to soften).

Truflation is different. It updates more dynamically and attempts to capture price changes closer to real time. It is not a replacement for official statistics, and we should not pretend otherwise. But it can be useful when trying to detect whether inflation pressure is already fading beneath the surface.

That is why this divergence is important. If Truflation is closer to the real-time direction of travel, inflation could surprise on the downside even as growth remains stronger than expected.

That would be a major macro surprise.

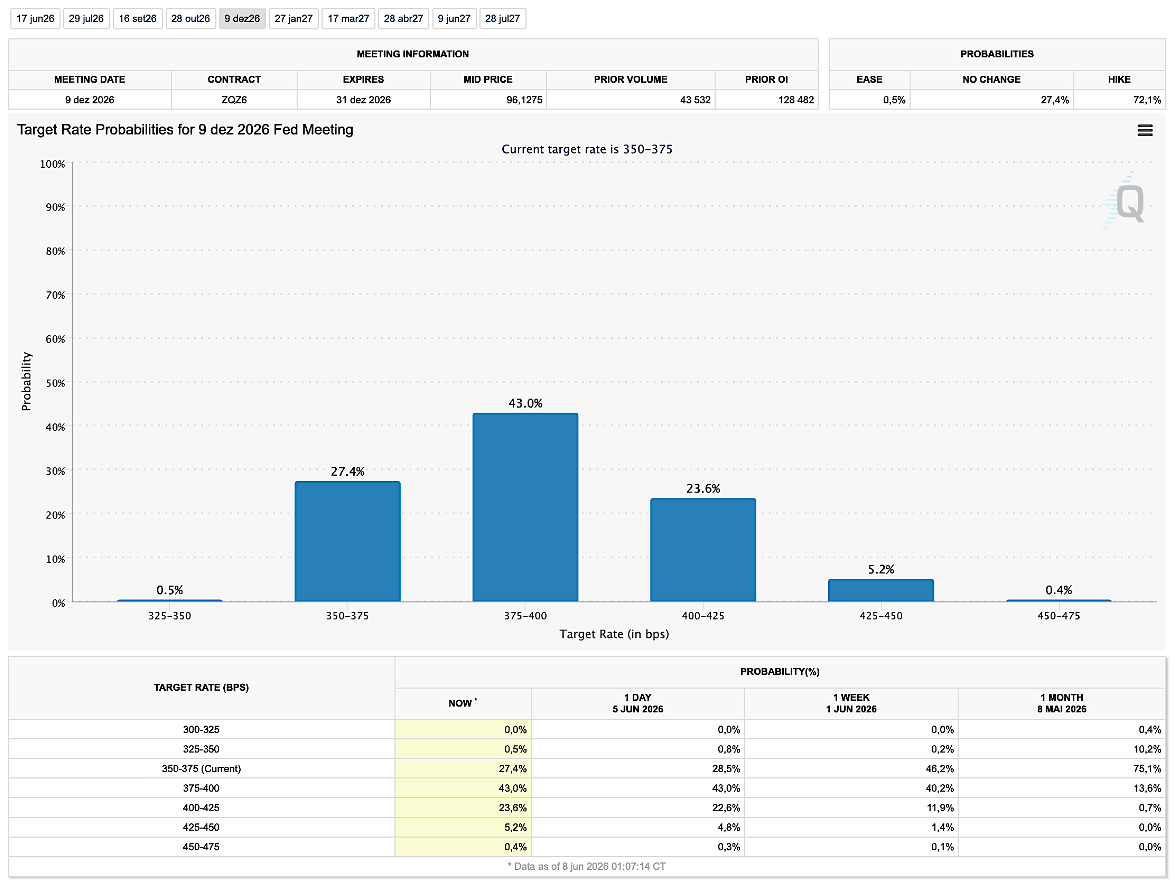

Because the market is currently positioned for the opposite.

The implied probabilities for Fed hikes into year-end have increased materially. Investors are no longer merely debating whether the Fed stays higher for longer. They are increasingly entertaining the possibility that the next move could be up.

The following chart captures the market’s fear very clearly.

That is why markets sold off.

Not because growth was bad. Because growth was interpreted as inflationary. And inflationary growth was interpreted as a reason for tighter policy. That is the market’s chain of thought.

But if the growth impulse is more productivity-led than investors believe. And if inflation surprises on the downside rather than the upside… Then the market may be positioned for exactly the wrong policy path.

That brings us to Kevin Warsh.

The consensus view on Kevin Warsh is that he is hawkish. That is certainly how the market is treating him. At first glance, the assumption makes sense. He has spent years warning about inflation credibility, criticizing monetary excess, and sounding more orthodox than many investors would prefer.

But markets have a habit of flattening people into caricatures.

The deeper question is not whether Warsh has hawkish instincts.

The deeper question is how he would respond to a world in which growth is improving because productivity is improving.

That is a very different setup from a classic inflationary overheating cycle.

If stronger growth is accompanied by higher productivity, better capital allocation, and contained inflation pressure, then the case for further tightening becomes much weaker. In fact, under that scenario, the real policy surprise may not be hikes at all.

It may be cuts.

That sounds highly contrarian today. Which is precisely why it deserves attention: if the market is positioned for a hawkish Fed and instead receives a more dovish policy path, the repricing could be violent.

Risk assets would not need perfection.

They would only need the market to discover it had become too pessimistic. And perhaps our view is simply paying closer attention than consensus to what Warsh has been signaling all along: the quality of growth matters, the supply side matters, and productivity matters.

The White House is not being subtle about this. It is openly arguing that higher productivity and capital spending (particularly those associated with AI) can reduce inflationary pressure and give the Fed room to cut.

That is no longer a fringe interpretation... it is being stated explicitly. Of course, the White House has political incentives. We understand that. No serious investor should confuse political messaging with objective truth. But in a politically charged Fourth Turning environment, it would be equally foolish to ignore the direction of policy pressure.

Markets have an old adage:

Don’t fight the Fed. Don’t fight the tape.

In this cycle, we would add a third:

Don’t fight the White House.

If the administration wants lower rates, if it sees AI and productivity as disinflationary, and if the data begin to support that interpretation, the market may be setting itself up for a major upside surprise.

Because the current consensus is still anchored to the old inflationary-growth framework.

If our thesis holds, the implications are significant.

A market that has rapidly repriced toward higher rates would have to reconsider the policy path. Investors who have been selling duration, software, China internet, precious metals, and other liquidity-sensitive assets would have to ask whether they reacted to the right data with the wrong framework. And the parts of the market now being punished for their sensitivity to rates and liquidity could suddenly become the greatest beneficiaries of a macro surprise.

That is where the opportunity sits.

Not necessarily in the most obvious AI winners, where the earnings bridge is already visible, positioning is increasingly crowded, and the market has learned to pay for the story. The more interesting setup may now lie in the assets still carrying the scars of the old inflationary-growth framework: long-duration growth, where lower rate expectations can change the discount-rate math; software, where AI may turn from perceived threat into operating leverage; China internet, where the application layer remains deeply discounted; and precious metals, where a softer real-yield path could revive the monetary thesis.

But there is one area where the disconnect may be even more striking.

Because if the market is wrong about the nature of this growth impulse, if the Fed surprise is dovish rather than hawkish, and if the next AI opportunity is less visible than the last one, then the major opportunity may not be in the AI trade investors have already discovered.

It may be in the one they are currently selling.

Crypto.

—

Disclaimer

The information provided herein is for general informational purposes only and does not constitute financial advice or a recommendation to buy, sell, or hold any investment. It is not tailored to any specific individual or investor profile. All investments involve risks, and past performance is not indicative of future results. Before making any investment decisions, it is important to consider your own financial situation and risk tolerance. We do not guarantee the accuracy, completeness, or reliability of any information provided, and we disclaim any liability for any loss or damage arising from reliance on the information herein. Readers are advised to consult with an authorized financial intermediary before making any investment decisions.

A quick note on accountability.

We don’t publish these theses to be right on paper. We publish them to express edge in the real economy. Our Leaderboard shows the exact scorecard since inception, tracking every position, our compounding outperformance against the market, and the triple-digit winners we’ve captured along the way.

You might also like reading

And from VMF’s Strategic Asset Allocation:

The Phillips Curve describes the traditional relationship between labor-market tightness and inflation: when unemployment is low and the economy is strong, wage pressure tends to rise, which can feed into higher prices. That is why strong payrolls often make markets fear a more hawkish Fed. But the key variable is not wages alone; it is wages relative to productivity. If workers produce more output per hour, companies can absorb higher compensation without the same inflationary pressure.

Truflation is not just another inflation gauge: it is a cryptonative attempt to make macro data faster, more transparent, and more verifiable. Its U.S. index tracks more than 15 million items from 30+ data sources and updates daily, creating a real-time contrast with the slower official CPI process. That matters because markets and the Fed may still be reacting to lagging inflation data just as real-time price pressure is fading.