The Visible Side of the AI Boom

As the market finally recognizes the physical infrastructure bottlenecks in semiconductors, memory, and power, the investment job shifts from finding growth to finding where it is still underpriced.

The easiest mistake in investing is to think the hard part is being right. - It is not.

Being right is only the first test.

The harder test comes later, when the market finally agrees with you, the thesis becomes obvious, and a position that once looked misunderstood begins to look crowded.

That is where discipline matters.

For much of the past year, one of our central arguments at VMF Research has been that AI may look like a chatbot on the screen, but underneath it sits one of the largest physical infrastructure buildouts in modern market history.

Behind every model, every AI agent, and every productivity breakthrough sits an enormous demand shock for semiconductors, memory, data centers, electricity, cooling, grid capacity, and capital spending.

That framework led us into some of the cleanest AI bottleneck trades before the market fully appreciated them.

But now the visible side of the AI boom is no longer hidden...

The market can see the need for chips.

It can see the need for memory.

It can see the need for data centers.

It can see the need for power.

And once a bottleneck becomes visible, capital starts to crowd into it. That does not mean the opportunity is over. But it does mean the job changes.

The question is no longer simply:

Where is the AI growth?

The better question is:

Where is the AI growth still underpriced?

That is the transition at the heart of May’s issue of VMF’s Strategic Asset Allocation.

In the paid issue, we use this framework to explain why we are managing some of our strongest AI-related winners with more discipline, why we have already taken partial profits in one of them, and where we believe the next layer of opportunity may now be emerging.

The following excerpt focuses on the first part of that argument: the visible side of the AI boom, the bottlenecks the market has already begun to recognize, and the portfolio-management lesson that follows when a thesis works almost too well.

There are moments in markets when a thesis stops being controversial and starts becoming obvious. That is usually a good thing. But it is also the moment when the job changes...

At the beginning of a trade, the real challenge is conviction. The evidence is incomplete. The narrative is uncomfortable. The market has not yet fully recognized what is happening. That is where the opportunity usually lives. Later, once the market begins to agree, the challenge is no longer to see the opportunity.

It is to manage what happens after everyone else starts seeing it too.

That is exactly where we now find ourselves with two of the cleanest AI-related bottleneck trades in our Model Portfolio: South Korean equities through EWY 0.00%↑ and uranium miners through. URNM 0.00%↑

When we added South Korea in January 2025, the logic was already there.

The AI buildout was going to require an extraordinary amount of compute.

And compute would not only require NVIDIA GPUs. It would require memory... a lot of memory! High-bandwidth memory. Server DRAM. Enterprise SSDs. Advanced packaging. The entire physical stack behind the intelligence layer.

In other words, the market was already learning to worship the AI model makers and the GPU suppliers, but it had not yet fully appreciated the broader supply chain that would have to scale with them.

That was the opportunity.

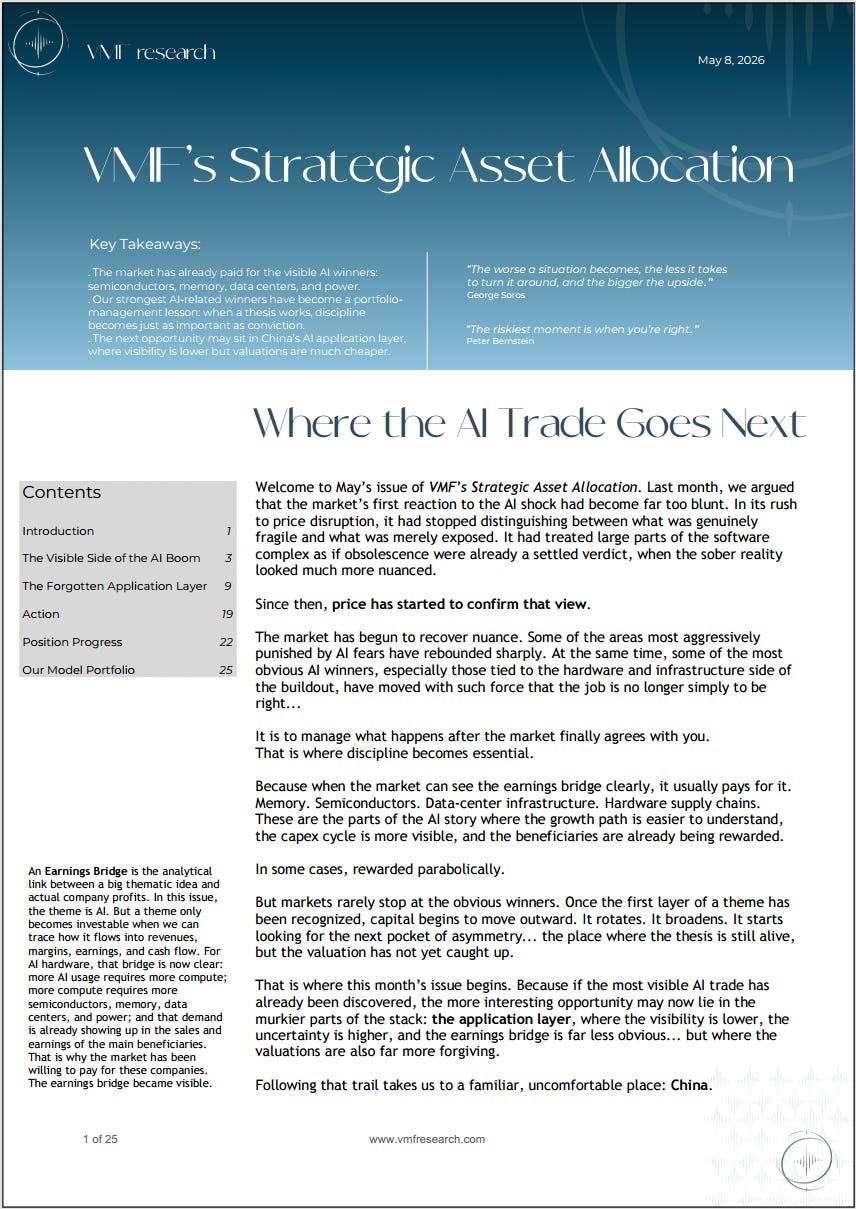

Because AI may feel weightless to the end user, but it is not weightless at all. It is one of the most capital-intensive technology waves the world has ever seen. Gartner now expects global semiconductor revenue to grow 64% in 2026, with memory revenue expected to triple, DRAM prices rising 125%, NAND prices rising 234%, and AI semiconductors representing roughly 30% of total semiconductor revenue this year.

That is not just an upgrade.

That is an industrial buildout.

And the numbers across the winners now confirm it. NVIDIA’s full-year revenue rose 65%, while its fourth-quarter data-center revenue increased 75% year over year. Broadcom’s AI semiconductor revenue grew 106% year over year. TSMC’s ( TSM 0.00%↑ ) first-quarter revenue increased 35%, while net income and diluted EPS both rose 58%.

Even ASML (ASML 0.00%↑), the irreplaceable lithography supplier to the leading-edge semiconductor ecosystem, raised its 2026 sales outlook as AI demand continued to outstrip chip supply.

These are not normal cyclical numbers...

They are the financial footprints of a capex supercycle.

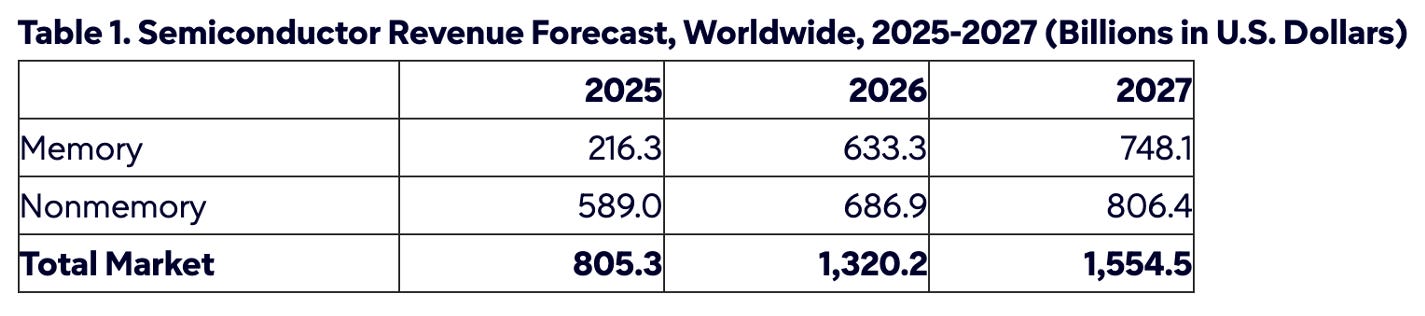

The above chart compares today’s tech capital-spending boom with previous U.S. infrastructure and innovation buildouts, measured as a share of GDP. The message is clear: this is not a normal upgrade cycle. The current wave of tech capex is already larger, relative to the economy, than several landmark projects and past investment booms, including the Apollo Program, the Interstate Highway buildout, and the dotcom broadband cycle. In other words, AI is not just changing software. It is forcing one of the largest physical infrastructure buildouts in modern market history.

But our edge was not simply recognizing that AI hardware would benefit. By early 2025, that was already becoming increasingly clear. The harder question was where that visibility had not yet been fully priced.

Our answer was South Korea.

Because if AI compute was going to grow exponentially, memory demand was going to follow. The market could not keep treating memory as just another cyclical commodity if high-bandwidth memory, server DRAM, and enterprise SSD demand were becoming structural bottlenecks. South Korea, through Samsung Electronics and SK Hynix, sat directly in the path of that change.

That is now being confirmed with force.

Samsung’s latest quarter showed a 43% sequential increase in consolidated revenue, with its Device Solutions division posting an 86% sequential sales increase, as the memory business set new quarterly records and management pointed directly to AI-related demand, HBM, DDR5, SOCAMM2, and enterprise SSDs. SK Hynix, meanwhile, delivered record quarterly results, with revenue rising roughly 60% sequentially, operating profit nearly doubling versus the prior quarter, and management explicitly attributing the performance to strong AI infrastructure demand and higher sales of high-value-added products such as HBM, high-capacity server DRAM, and enterprise SSDs.

That is the earnings bridge the market is now paying for.

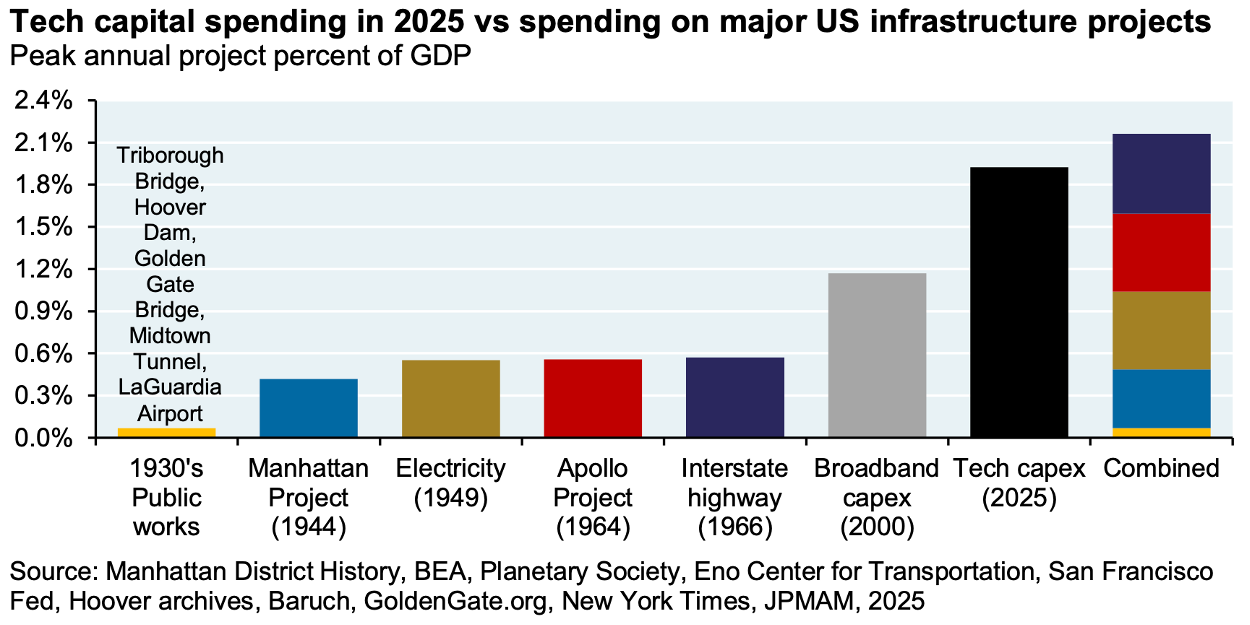

And, as you can observe in the chart on the previous page, once that reality became impossible to ignore, the market paid for it aggressively.

Since the beginning of 2025, EWY (green line) has not merely kept pace with the semiconductor trade. It has dramatically outperformed two of the most popular semiconductor ETFs, SMH (red line) and SOXX (blue line).

The green line tells the story: South Korea became one of the cleanest expressions of the AI hardware cycle precisely because the market had initially underappreciated how much operating leverage the memory giants could capture once the demand surge became undeniable.

The initial chart makes the portfolio-management lesson even clearer. We recommended EWY ( EWY 0.00%↑ ) when the opportunity was still underappreciated and, above all, inexpensive.

That is the crucial point.

The sales and earnings momentum now being delivered by Samsung and SK Hynix sits in the same broad neighborhood as some of the most celebrated AI winners in the U.S. and global semiconductor complex. Yet, because the market had not initially priced South Korea as an obvious AI winner, the price response has been far more explosive. EWY has almost doubled the performance of the semiconductor ETFs where those more fashionable AI names command the largest weights.

Still, when the market began to recognize the story, we took our first partial profit at the beginning of November. And now, after another extraordinary move, we have taken a second partial profit, closing half of the remaining position at $162 and locking in a 206.5% total return on that tranche.

That decision is not a rejection of the thesis...

It is the thesis working.

Btw, Have you check our leaderboard section?

It tells the story better than any intro, showing our total returns since publication, including multiple triple-digit winners and a consistent record of beating the market while managing risk.

And just as importantly, it is our Investment Process working. The goal is not to fall in love with a position after the market has finally discovered it. The goal is to keep moving capital toward the best risk/reward opportunities inside the same secular megatrend.

After a powerful advance, URNM has spent the past few months moving sideways, compressing into a symmetrical triangle defined by lower highs and higher lows. This suggests consolidation rather than a completed reversal. Because triangles usually act as continuation patterns when they appear after a strong prior uptrend, our base case is for an eventual upside resolution. Still, confirmation requires a decisive breakout above the upper boundary of the pattern. Until then, the message is clear: URNM is digesting its gains, and a point of decision is approaching.

But before we move to the pockets of opportunity that now look more attractive, we need to address our other obvious AI winner. Because the same broad logic we applied to EWY also applies to URNM.

The difference is that this trade is not yet as mature.

For a long time, nuclear energy was discussed mostly as a political, environmental, or commodity story. Today, it is increasingly being pulled into a very different conversation: AI infrastructure.

The reason is simple.

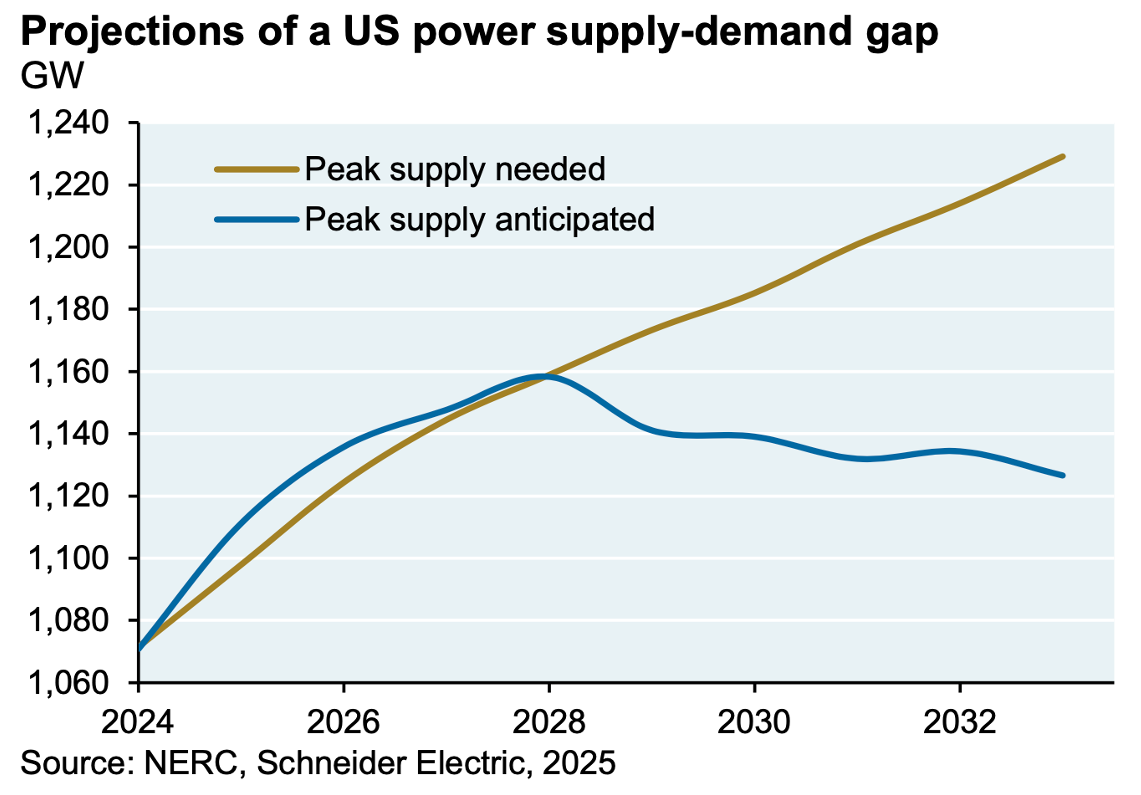

The AI buildout does not only need chips. It needs electricity. Reliable electricity. Scalable electricity. And, most importantly, electricity that can be delivered where and when data centers need it.

That is becoming one of the most important bottlenecks in the entire AI stack.

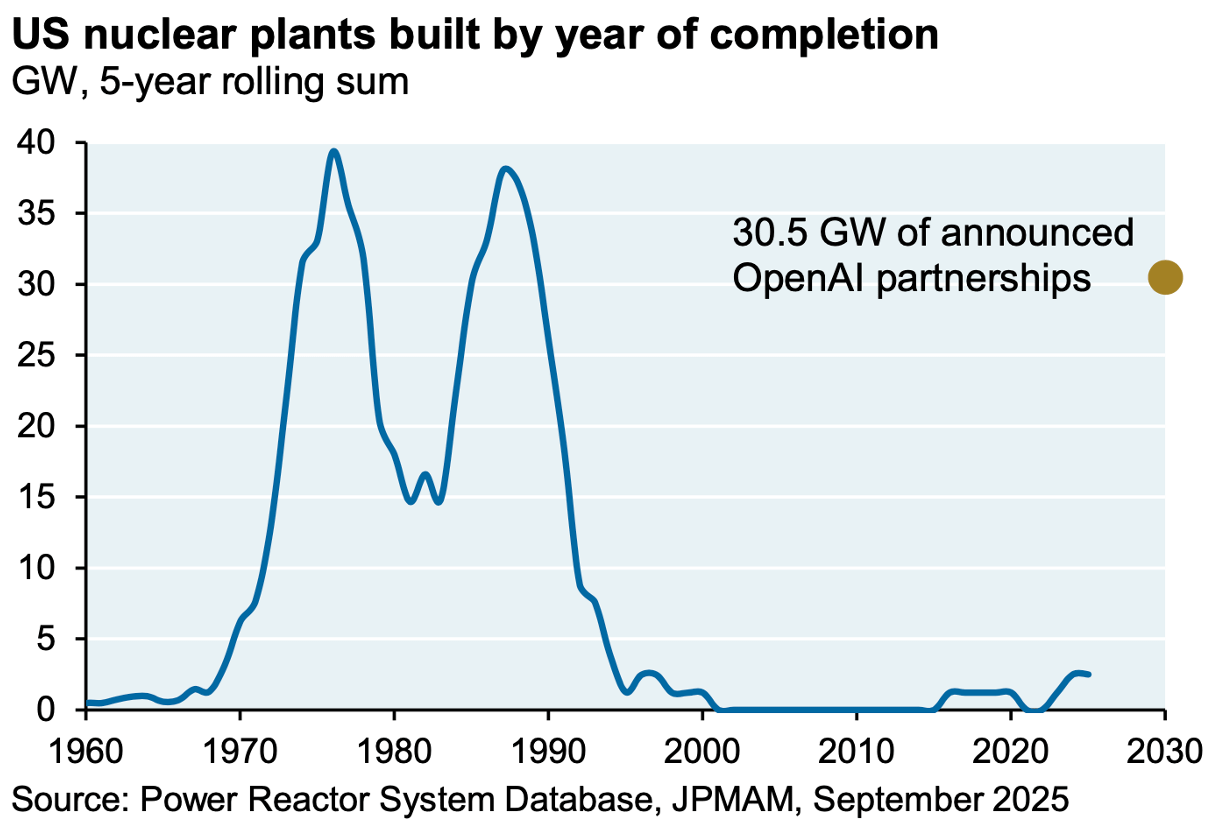

OpenAI alone has announced partnerships requiring 30.5 GW of new power. To put that figure into context, that is roughly 75% of the peak level of nuclear capacity the U.S. completed over any five-year period during the nuclear buildout era.

And that is just one company in the AI ecosystem...

That comparison should stop us in our tracks.

Because the market has become comfortable talking about AI as if the limiting factors are mostly models, chips, and capital. But the physical world is now pushing back. The entire U.S. added only 25 GW of capacity in 2024 after adjusting for intermittency and reliability, while the projected gap between peak supply needed and peak supply anticipated continues to widen into the next decade.

The AI economy is trying to grow inside an electricity system that was not designed for this kind of step-change in load growth.

That is the gap nuclear is being pulled into.

Not because nuclear is perfect. It is not. New plants are hard to build. Timelines are long. Permitting is painful. Small modular reactors still have a lot to prove. And only a very small number of decommissioned U.S. nuclear plants may realistically be restarted.

The dot in the first chart represents only OpenAI’s announced power partnerships. That alone is remarkable. These commitments already approach the peak levels of U.S. nuclear capacity completed during the 1970s and 1980s nuclear buildout. And OpenAI is only one company in the AI ecosystem. That is why the power bottleneck is becoming impossible to ignore.

But that is precisely why existing nuclear assets, uranium supply, and the broader nuclear fuel cycle have become so interesting.

If power is the bottleneck, and if new nuclear supply cannot be created quickly, then the existing uranium ecosystem becomes far more strategically relevant. Not because it solves the entire data-center power problem tomorrow. It obviously does not. But because it sits inside the narrow group of solutions capable of providing the kind of reliable baseload power the AI economy increasingly needs.

This buildout is not limited to uranium or nuclear power. It also requires natural gas, grid equipment, cooling systems, electrical infrastructure, construction capacity, and specialized engineering. That is why, across VMF’s Security Selection Model Portfolios, we have also recommended individual companies that benefit directly from the broader AI infrastructure boom.

And that changes the nature of the trade.

Uranium is no longer just a commodity story.

It is becoming another AI bottleneck trade.

That is why our URNM position matters. As the chart on page 6 shows, we are already up roughly 70% since adding the position to the Model Portfolio. Like EWY, it has dramatically outperformed our equity benchmark. And like EWY, it reflects the same Investment Process: identify the bottleneck early before the market fully understands how visible the demand is likely to become.

But, again, maturity matters.

EWY has already entered the phase where the market has moved from recognition to something close to euphoria. URNM is not there yet. The position did briefly approach the 100% mark at the beginning of this year, but the move was too quick for us to formally monetize it through our publications. If it reaches that level again, we intend to close half of the position and lock in part of the gain. That is not because the nuclear thesis would be over. Far from it...

It is because our job is not merely to identify the right secular trend. It is to manage the position as the market increasingly discovers it.

This is the key lesson.

The market has now discovered the visible parts of the AI trade. It understands GPUs. It understands semiconductors. It is beginning to understand memory. And it is increasingly being forced to understand power.

Once a bottleneck becomes visible enough, capital begins to crowd into it. That does not mean the opportunity disappears overnight. But it does mean the risk/reward changes. And once that happens, the opportunity can move very quickly from underappreciated to overextended. That is why discipline now matters.

EWY and URNM have done exactly what we hoped they would do. They gave us exposure to the visible hardware and power bottlenecks of the AI buildout before that visibility had been fully priced. They rewarded us handsomely as the market caught up. And in the case of EWY, the move became stretched enough for us to harvest another part of the gain.

That is not a bad problem to have, it is the kind of problem good investing creates.

You might also like reading