Hawk… or Just Misread?

Warsh is no Volcker: Why a "Hawk" Fed might actually be the ultimate liquidity play.

Most people have never seen what serious investment research actually looks like behind a paywall. They see the marketing… the headlines… the hot takes.

They don’t see the real deliverable.

So, I’m going to change that.

From now on, some of my Substack posts will include long-form, properly framed excerpts from what we publish behind the paywall at VMF Research.

You’ll be able to judge the quality for yourself. No paraphrasing. No “adaptations.” Just a clear window into the work.

Today’s excerpt comes from February’s issue of VMF’s Strategic Asset Allocation, published on February 13, 2026.

That issue covered several themes, including what appears to be a Great Acceleration in economic growth, driven by productivity gains, with AI playing an increasing role.

But the passage I’m sharing here focuses on something different… and far more immediate for markets.

It tackles one of the three main drivers of volatility right now (I laid out all three in my latest Leaderboard update): the future path of Liquidity, and what changes when leadership at the Federal Reserve is about to shift.

To be clear: the asset allocation implications, the position sizing, and how we’re acting on this in our Model Portfolios remain behind the paywall. That’s where the actionable edge lives. And if you’ve seen the updated Leaderboard, you already know we have a roster of meaningful outperformers.

For now, I simply want you to read how we think... before we ever tell subscribers what to do.

I hope you enjoy the excerpt. And if you have questions, leave them in the comments

Let’s start with what, in our view, has been the main catalyst behind February’s sudden jump in volatility.

Not a slow build. Not a gentle repricing. A snap.

The kind of move you only get when markets are forced to re-map their assumptions in real time.

On the very last trading day of January, reports broke that President Trump had settled on Kevin Warsh as his nominee for the next Fed Chair.

And the market’s reaction made one thing immediately clear: this wasn’t being treated as a routine personnel headline. It landed as a policy signal... and a disruptive one at that!

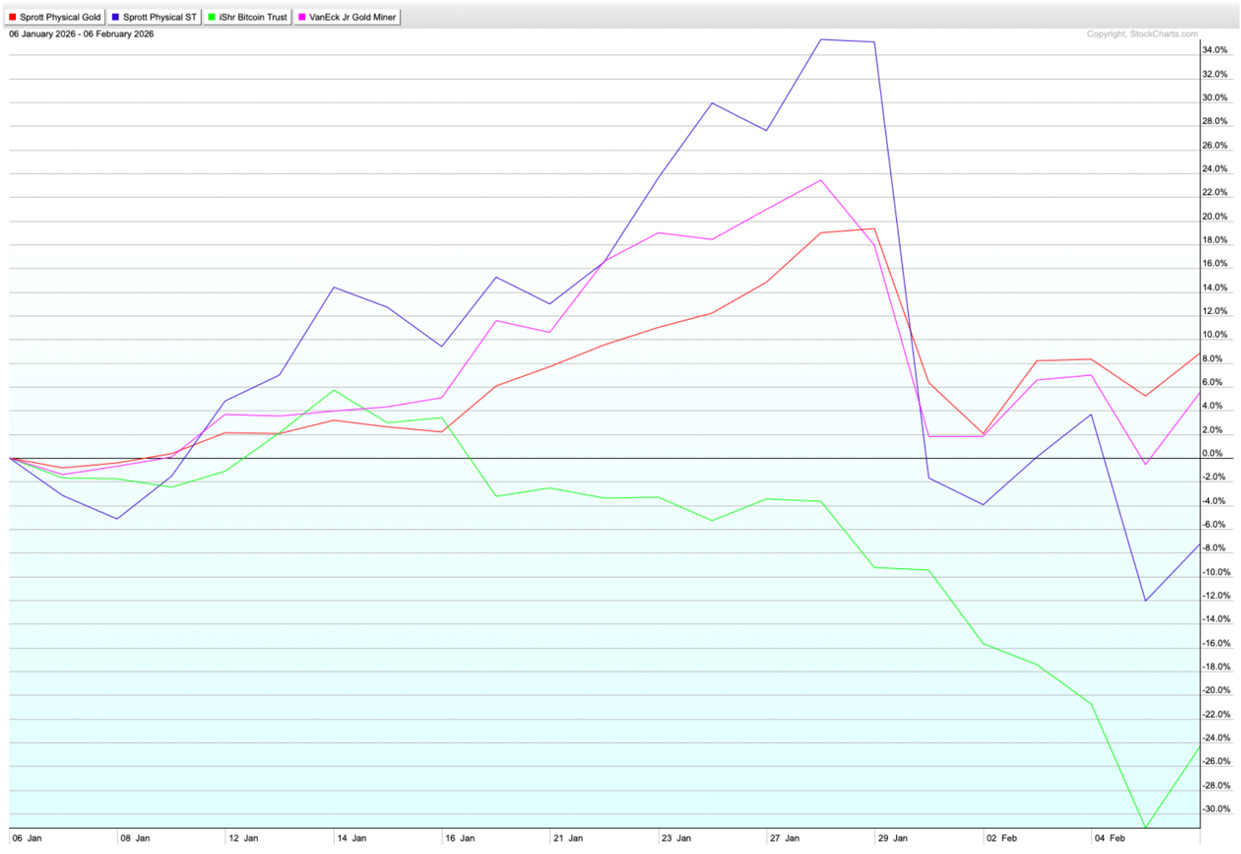

Just check what happened to gold ( PHYS 0.00%↑ ), silver ( PSLV 0.00%↑ ), junior gold miners ( GDXJ 0.00%↑ ) and Bitcoin BIT 0.00%↑ on the very last trading day of January:

What you saw was the market pricing a different policy regime. Not higher rates tomorrow, but a different balance between rate cuts, balance-sheet policy, and the Fed’s tolerance for “easy money” as a permanent feature.

And once that question gets opened, the assets most exposed to liquidity expectations are forced to reprice immediately... before the rest of the market even knows what it’s reacting to.

So yes, the surprise was real... and, in our view, far more consequential than what prediction markets were implying in the days leading up to Trump’s decision.

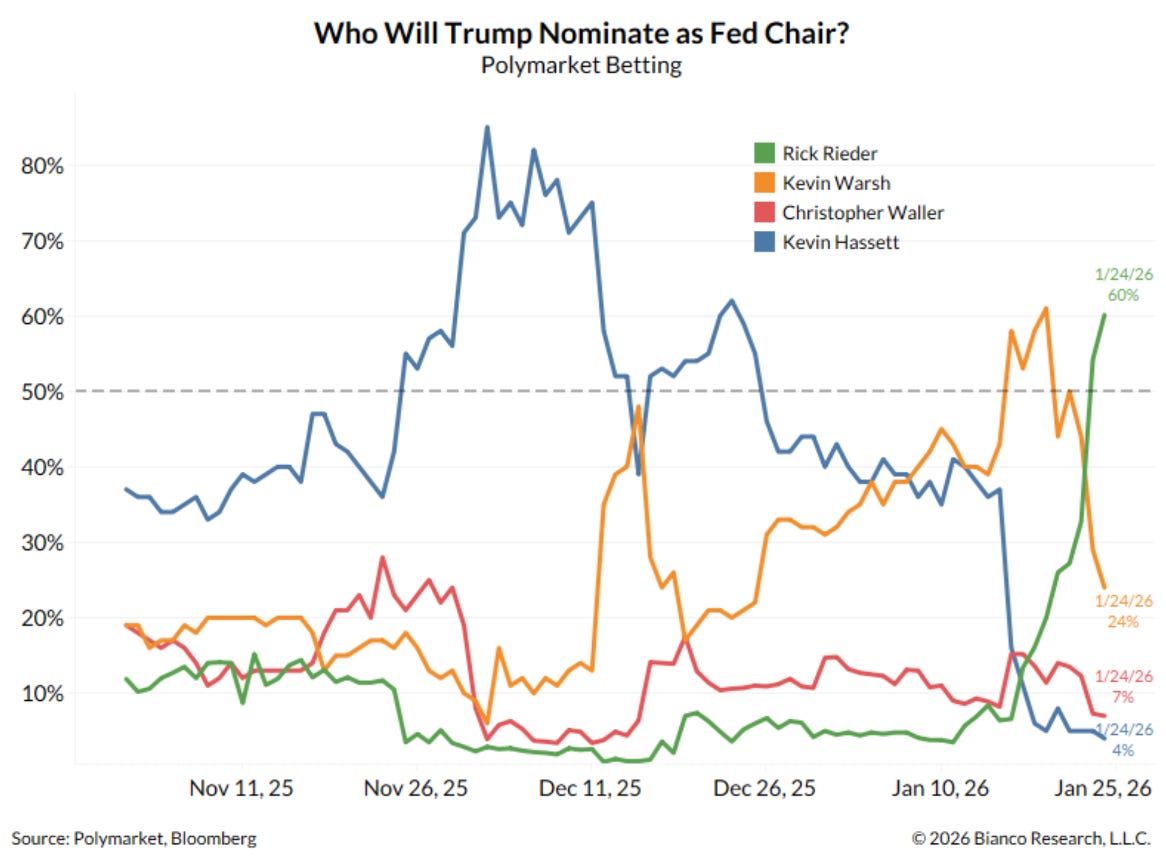

The chart above This chart shows Polymarket’s odds for Trump’s Fed Chair nomination. Prediction markets are becoming increasingly valuable tools (as we’ve noted recently in our Alpha Tier).

Those markets had already been furiously rotating through other names.

First, Kevin Hassett was widely treated as the near-certain frontrunner into late 2025.

Then, more recently, BlackRock’s Rick Rieder briefly became the dominant favorite in the same prediction-market ecosystem.

In other words, investors were bracing for one type of Fed future… and then got served a different one.

But the deeper reason Warsh landed as a shock is what he may imply for the single variable we currently weight most heavily in our Investment Process: Liquidity.

Now, don’t misunderstand us.

Trump didn’t nominate a Volcker-style hawk1. In fact, Warsh has been associated with the view that rates should come down, and come down quickly.

That aligns perfectly with Trump’s political incentives in a midterm year: relieve pressure on households, support economic activity, and ease stress in a Treasury market that’s groaning under the burden of refinancing.

That part of the profile is not the problem.

The problem is the second part.

Warsh has been a long-standing critic of a permanently swollen Fed balance sheet. He’s argued (repeatedly) that the post-2008 framework created bad habits, blurred lines, and baked in an unhealthy dependence on perpetual intervention.

And he’s floated the idea that what the Fed really needs isn’t another tweak at the margin… but a more fundamental reset in how it operates.

And that is the fault line.

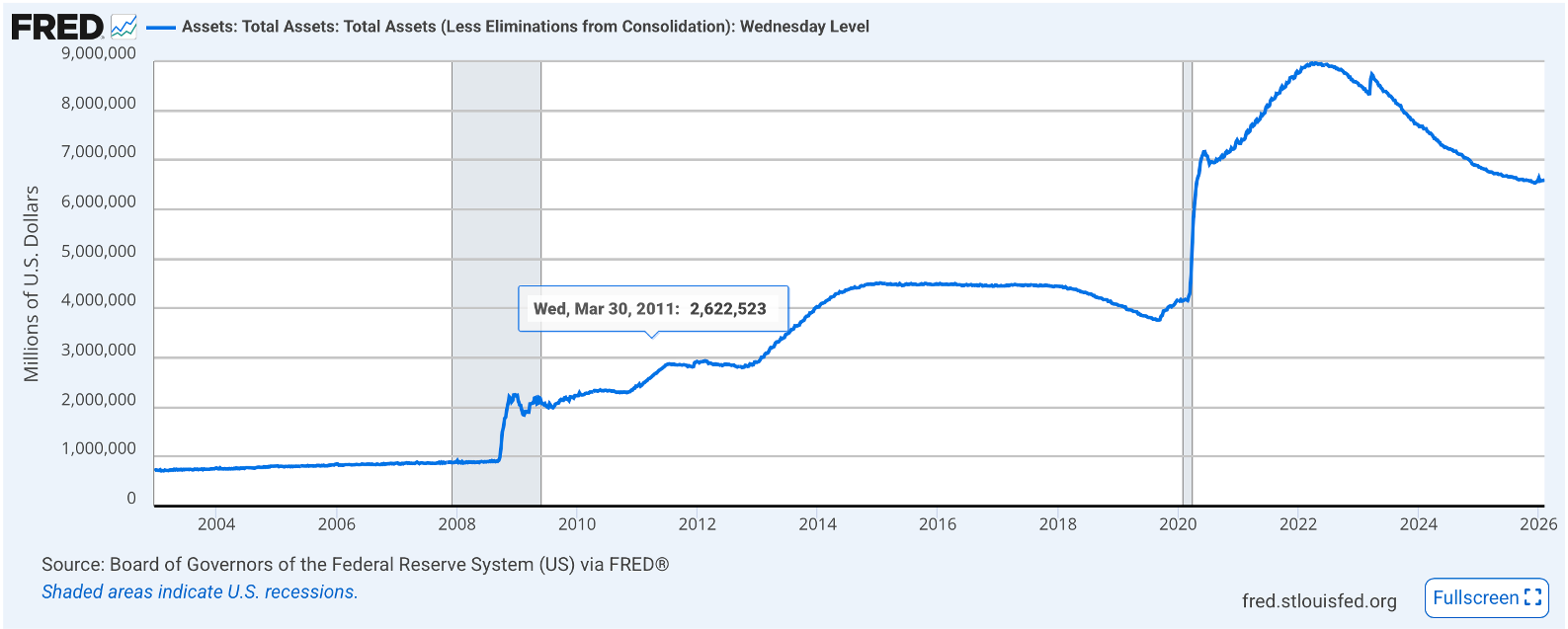

If you look at the chart above showing the Fed’s balance sheet since 2003, you’ll notice something that still defines this entire era: once the line goes vertical in 2008, it never truly goes back to “normal.”

That’s why we chose this timeframe.

Kevin Warsh isn’t a commentator looking in from the outside. He’s a Fed veteran who lived through the moment the old operating framework snapped. Warsh served as a member of the Board of Governors from 2006 to 2011.

And the market’s shock in late January is tied to how that chapter ended.

To understand why Warsh’s name hits like a policy grenade, you have to revisit what the Fed actually did in 2008–2009... and why it did it. The balance sheet exploded for a simple reason: the system was freezing. Credit markets were seizing.

Major institutions were failing.

So, the Fed responded the only way it could at the time: it became the buyer, lender, and shock absorber of last resort.

It rolled out emergency liquidity facilities and then moved to large-scale asset purchases (the infamous QE) buying Treasuries and mortgage-backed securities to stabilize markets, push down longer-term rates, and restart the plumbing.

In other words, the Fed didn’t just cut rates. It manufactured liquidity (printed money) by expanding its footprint across the financial system.

That set a precedent. And precedent is destiny in central banking.

Once markets learn the Fed will step in, and once the political system learns the Fed can step in, the balance sheet stops being a crisis tool and starts becoming part of the permanent architecture. QE1 bleeds into QE2 (and 3 and 4).

Emergency measures turn into a standing doctrine. And over time, the market internalizes a new rule: when things get shaky, the Fed’s balance sheet will do the heavy lifting.

Warsh was there for the birth of that doctrine... and then he walked away from the institution that institutionalized it.

He resigned in 2011, and his departure was widely read as a rebuke of the Fed’s post-crisis trajectory, especially its continued reliance on extraordinary measures like QE2.

Now connect the dots to why his name matters today.

Warsh’s criticism has never been, “the Fed should never act in a crisis.”

His argument has been more dangerous than that... because it’s structural. He has repeatedly warned that a permanently bloated balance sheet distorts markets, blurs the line between monetary policy and quasi-fiscal policy, and creates an unhealthy dependency on ongoing intervention.

That’s the point.

Markets can live with “rates down.” They can even live with “rates down fast.”

What they can’t easily price is a Fed Chair who might be willing to question the deeper engine of the post-2008 regime: the assumption that the balance sheet only grows in one direction over time.

Which is why the nomination didn’t just move yields or futures for a few hours.

It hit the most liquidity-sensitive assets first, because it challenged the one story they’ve been trading on for years: not today’s liquidity... but the market’s confidence in tomorrow’s liquidity.

Ironically, it makes perfect sense that the next arena of “tectonic change” is monetary policy. January gave us geopolitical shocks. February is giving us institutional shocks. Because if there’s one sacred assumption markets have leaned on for the past two decades, it’s that, when things get ugly, the Fed will show up, cut rates, add liquidity, and cushion the fall.

That reflex has a name: the “Fed put.” Not an official policy, of course… but a behavioral pattern investors have learned to love. When risk assets wobble, the central bank steps in, sometimes quickly, sometimes quietly, but reliably enough that markets began to treat liquidity support as part of the architecture.

And this is where Warsh matters. Because if his nomination signals anything, it’s that the old operating assumptions are no longer untouchable. That doesn’t mean the Fed suddenly becomes “tight.” It doesn’t mean policy stops reacting. But it does mean the backstop may become more conditional, more politically contested, and less automatic.

That is exactly the kind of shift Neil Howe associates with Crisis eras (Fourth Turnings) periods when institutions stop coasting on habit, legitimacy gets stress tested, and the rulebook gets rewritten under pressure. In other words, if investors are beginning to question the permanence of the Fed put... they’re not just repricing a market narrative.

They’re repricing the stability of the regime itself.

So, do we agree with the emerging consensus that a Warsh Fed would “take away the Fed put”?

Let’s start with the obvious: would Trump really nominate someone who’s fundamentally misaligned with Trump’s own interests?

We’ve seen this movie before.

Trump nominated Jerome Powell in 2017… and we all know how that relationship unfolded. And yes, interestingly, Warsh was already one of the names floating around that earlier Fed Chair race, before Powell ultimately got the job.

Trump himself has even acknowledged the dynamic publicly: the ideas nominees advertise before the job often don’t survive after they get the job.

In Davos, he basically said the quiet part out loud... people “change” once they’re in the seat.

That framing matters, because it leads to our variant view: Warsh is not being nominated to “end the Fed put.” He’s being nominated for a purpose. And the purpose is straightforward: get rates down and keep the refinancing machine running in an environment where the U.S. Treasury is rolling an absurd amount of debt.

Even Warsh’s critics generally concede he’s not a “higher-for-longer”2 ideologue... he’s been associated with the view that policy is “too tight” and that rates should move lower.

The real question isn’t whether he’ll accommodate the rollover.

It’s how.

Because the “how” is where regimes change… and where markets get nervous.

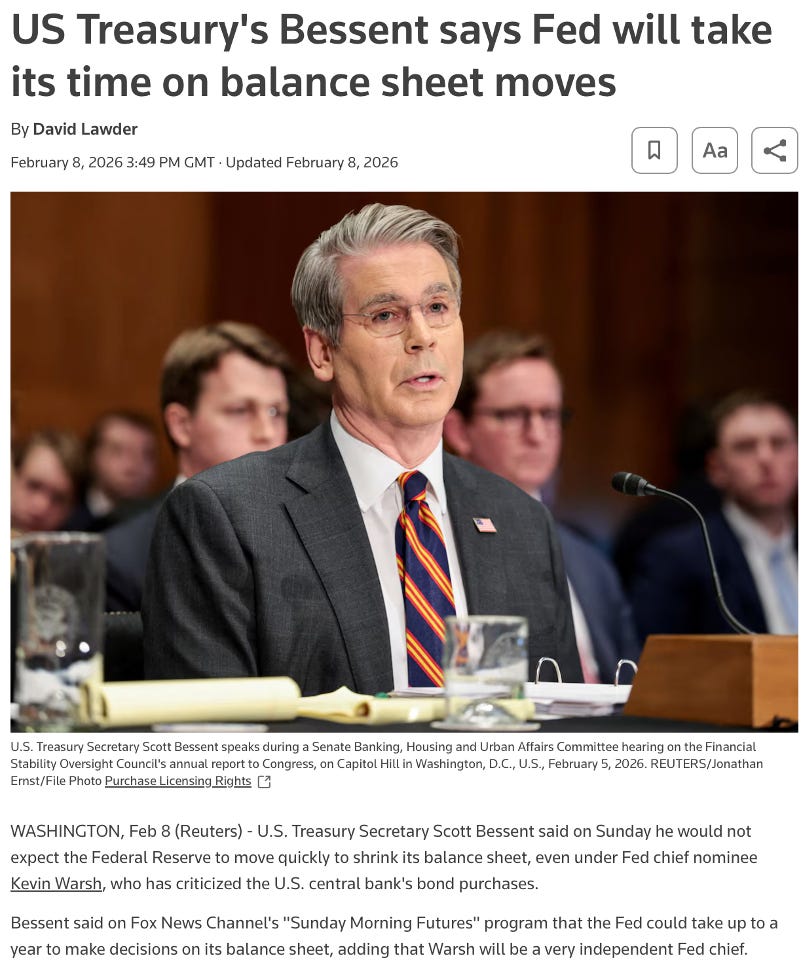

If Warsh lands at the Fed while Scott Bessent is running the Treasury, the base case is not institutional warfare... it’s coordination! And the playbook almost writes itself: lean harder into short-term issuance (so the government funds itself at the part of the curve the Fed directly controls) while expanding the Treasury buyback program to smooth the long end and manage refinancing pressure.

The buyback mechanism isn’t hypothetical: the Treasury has already been laying the groundwork for it, and senior officials have been explicit about treating buybacks as a live debt management tool.

Put differently, this starts to resemble a soft version of yield curve control... not the formal Bank of Japan kind, but a U.S.-style cousin: rate cuts anchoring the front end, issuance tactics shaping the duration profile, and buybacks helping contain the long end’s “accident risk.”

If Warsh cuts rates more aggressively than the market is pricing, then yes —mechanically, interest expense pressure eases, and the deficit math looks less explosive at the margin.

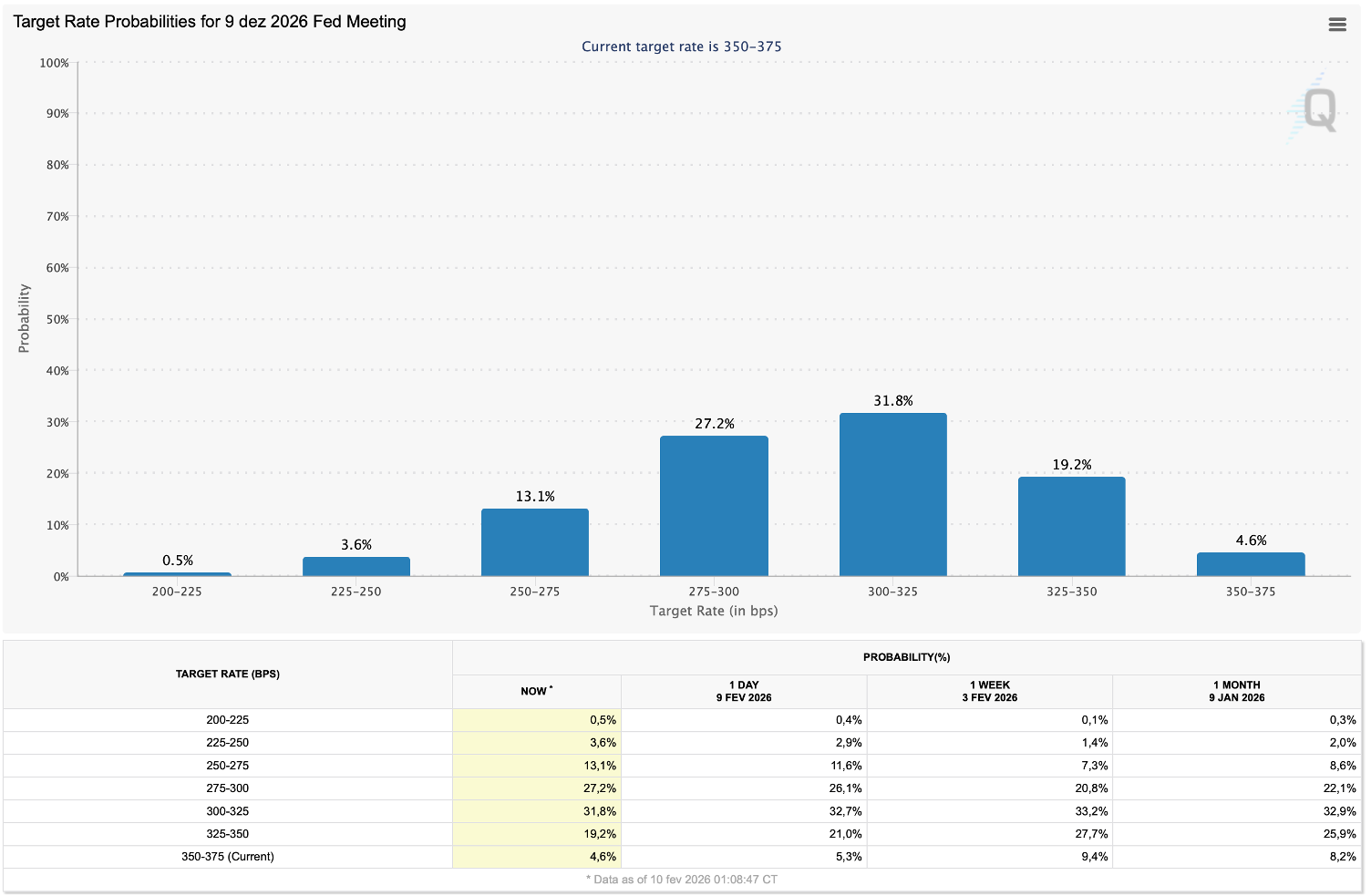

As you can see in the chart above, the market is still pricing a very tame path: roughly two Fed cuts this year (about 50 basis points in total).

We think that’s too conservative.

If Warsh gets the seat, our base case is that the cuts come faster and deeper... potentially twice what the curve is implying today. We’ll be here to stand accountable for that call.

And that’s why, despite the chaos we’ve seen in some liquidity-sensitive positions, our verdict remains constructive for the Model Portfolio. Meaningfully lower short rates aren’t just “good optics.” They’re real stimulus (in a midterm election year).

They ease the monthly burden across the economy, loosen financial conditions, and typically act like a tailwind for the parts of the market that thrive when money gets cheaper.

In practical terms, that’s especially supportive for our recent small-cap tilt (via the Simplify Piper Sandler US Small-Cap PLUS Income ETF, LITL). And it can remain constructive for our mortgage-finance exposure, Annaly Capital Management ( NLY 0.00%↑ ) because a rate-cut cycle that pulls the front end down while the long end holds up tends to steepen the curve... and a steeper curve is oxygen for that business model.

But here’s the catch: markets hate uncertainty more than they hate bad news.

And right now, the uncertainty is structural.

Investors can’t yet tell whether a Warsh Fed tries to cut rates while also shrinking the balance sheet faster… or whether it leans on alternative liquidity channels (repo facilities, regulatory tweaks, treasury-market plumbing) to keep the system lubricated.

That ambiguity is exactly the kind of thing that punishes liquidity-sensitive assets first... because they’re the quickest to reprice the “future path of liquidity.”

Will Warsh and Bessent pull it off?

Right now, the market’s default read is that Warsh is a hawk... or at least as the least “liquidity-friendly” option that was on the table. That perception matters because investors have grown used to a world where the Fed backstops markets in one way or another. Warsh has a track record of pushing back against that habit, and that’s why his name instantly triggers anxiety about a less generous liquidity regime.

But we think the market may be overreacting to the balance-sheet part of his profile and underweighting the political incentives sitting right in front of us.

Let’s ask the obvious question one more time: would Trump really nominate someone who plans to frustrate Trump’s own objectives? Trump wants lower rates, easier financial conditions, and a smoother refinancing path into a midterm election. Warsh may dislike a “forever-QE” framework... but that doesn’t mean he won’t act aggressively if the mandate (and the pressure) is clear.

And then there’s Bessent. He isn’t a traditional bureaucrat either. He’s coming from the hedge fund world, which tends to produce people who are fluent in market plumbing and ruthless about outcomes. That matters, because if this becomes a “get the refinancing done” moment, Treasury and the Fed will likely coordinate more tightly than markets are used to seeing.

So yes... we’ll give them the benefit of the doubt.

But we’ll also stay highly vigilant. Because even if the destination is “easier policy,” the path matters.

Paul Volcker was Chairman of the Federal Reserve from 1979 to 1987, and he is best known for crushing the double-digit inflation of the 1970s. Faced with runaway prices and a collapsing dollar, Volcker aggressively raised interest rates — pushing the federal funds rate above 20% at its peak. The move triggered a deep recession, but it ultimately broke inflation’s grip on the U.S. economy and restored credibility to the Fed. Volcker’s legacy is that of a central banker willing to tolerate short-term pain to reestablish long-term price stability.

“Higher for longer” is a phrase used to describe a central bank’s commitment to keeping interest rates elevated for an extended period of time, even after inflation begins to cool. The idea is to prevent premature easing that could reignite price pressures. For markets, it signals tighter financial conditions, sustained pressure on borrowing costs, and less immediate support for risk assets.