The Forgotten Application Layer

The hardware layer is priced in. The future belongs to deployment. Discover why China’s digital ecosystem is the ultimate AI application-layer play.

The first and easiest money in this AI boom was already made... and it was in the obvious places.

The companies selling the chips.

The companies building the memory.

The companies supplying the power.

The companies financing the data centers.

That is where the earnings bridge appeared first. And once the earnings bridge becomes visible, the market knows what to pay for.

But technology revolutions rarely end where the first money is made...

Infrastructure gets built so that something else can happen on top of it.

Chips are not bought for their own sake.

Data centers are not financed so they can sit there consuming electricity.

Compute is not the final product.

Usage is.

Commerce. Payments. Search. Advertising. Logistics. Manufacturing. Robotics. Mobility. Industrial automation. Consumer platforms. Daily economic life.

That is the application layer.

And this is where the AI story becomes more uncomfortable. Because the next opportunity may not sit in the cleanest market, the safest geography, or the most obvious winner. It may sit where investors still have the least trust.

That brings us to China.

Not because China is easy.

It is not.

Property remains a deep wound. Policy trauma is real. Geopolitical risk is unavoidable. And foreign investors have been disappointed too many times to forget it quickly. But serious investing does not begin when every risk disappears. By then, the discount usually disappears too.

The question is whether the market has priced China with discipline... or with despair.

In May’s issue of VMF’s Strategic Asset Allocation, we argued that China does not need to dominate the frontier-model race for the investment case to matter. It may only need to be good enough in models, unusually strong in deployment, and cheap enough for the market’s distrust to become the opportunity.

In the paid issue, we translated that framework into a concrete Model Portfolio action: the vehicle we chose, the exposure we added, the position we used to fund it, and the catalysts we believe could matter next.

The following excerpt develops the investment case behind that decision.

Because the next AI opportunity may not be hiding where the story is cleanest.

It may be hiding where the market still refuses to look.

Now that the market has begun to reward the visible AI bottlenecks, we need to move to the less comfortable part of the opportunity set.

The application layer.

This is where the debate becomes much harder.

The hardware layer is comparatively easy to understand. If AI usage grows, the world needs more compute. If the world needs more compute, it needs more chips, more memory, more data centers, more electricity, more cooling, more infrastructure, and more capital. The chain of logic is not perfectly clean, but it is visible enough for investors to underwrite.

The application layer is different.

Here, the visibility is lower. The dispersion will be wider. The winners and losers will be harder to identify in advance. Some early leaders will fade. Some apparently obvious use cases will disappoint. Some business models will turn out to be little more than temporary interfaces sitting on top of capabilities that commoditize very quickly.

That is why the market has been more reluctant to pay for this part of the AI stack. And yet, this is also where the long-term upside may ultimately be far larger.

Because infrastructure is not built for its own sake. Chips are not bought for their own sake. Data centers are not financed merely to sit in the desert and consume electricity. They are built because intelligence is expected to move into the real economy: into software, commerce, payments, search, advertising, logistics, entertainment, healthcare, manufacturing, mobility, customer service, industrial automation, robotics, and daily life itself.

In other words, the hardware layer is where AI gets built.

The application layer is where AI gets used.

And that distinction brings us to China.

Not because China is easy.

It is not.

And certainly not because the market has been foolish to apply a discount to Chinese assets...

The discount exists for very good reasons. But before we get to those reasons, we need to recognize something that has become too easy to forget after several years of disappointment: China remains one of the most important technology ecosystems in the world.

Not necessarily because it has overtaken the United States at the frontier-model layer. The U.S. still enjoys significant advantages in leading AI labs, hyperscale cloud infrastructure, advanced semiconductors, venture capital depth, and the ability to fund world-class model development at almost unimaginable scale.

But that is not the whole AI story.

Because the next phase of AI will not be judged only by benchmark scores, training budgets, or the elegance of frontier models. It will also be judged by deployment. By commercialization. By how quickly intelligence gets embedded into the real economy. By how effectively it moves through consumer platforms, industrial systems, payment networks, logistics chains, factories, vehicles, robots, and everyday workflows.

And in that world, China is far more formidable than most investors now seem willing to admit.

This is where the conventional Western framing can become too narrow. Investors look at export controls, chips, sanctions, and the frontier-model race, then conclude that China is structurally behind.

At one layer, that is fair. China still faces serious constraints in advanced semiconductors and the highest-end compute stack. But at another layer, the story is very different...

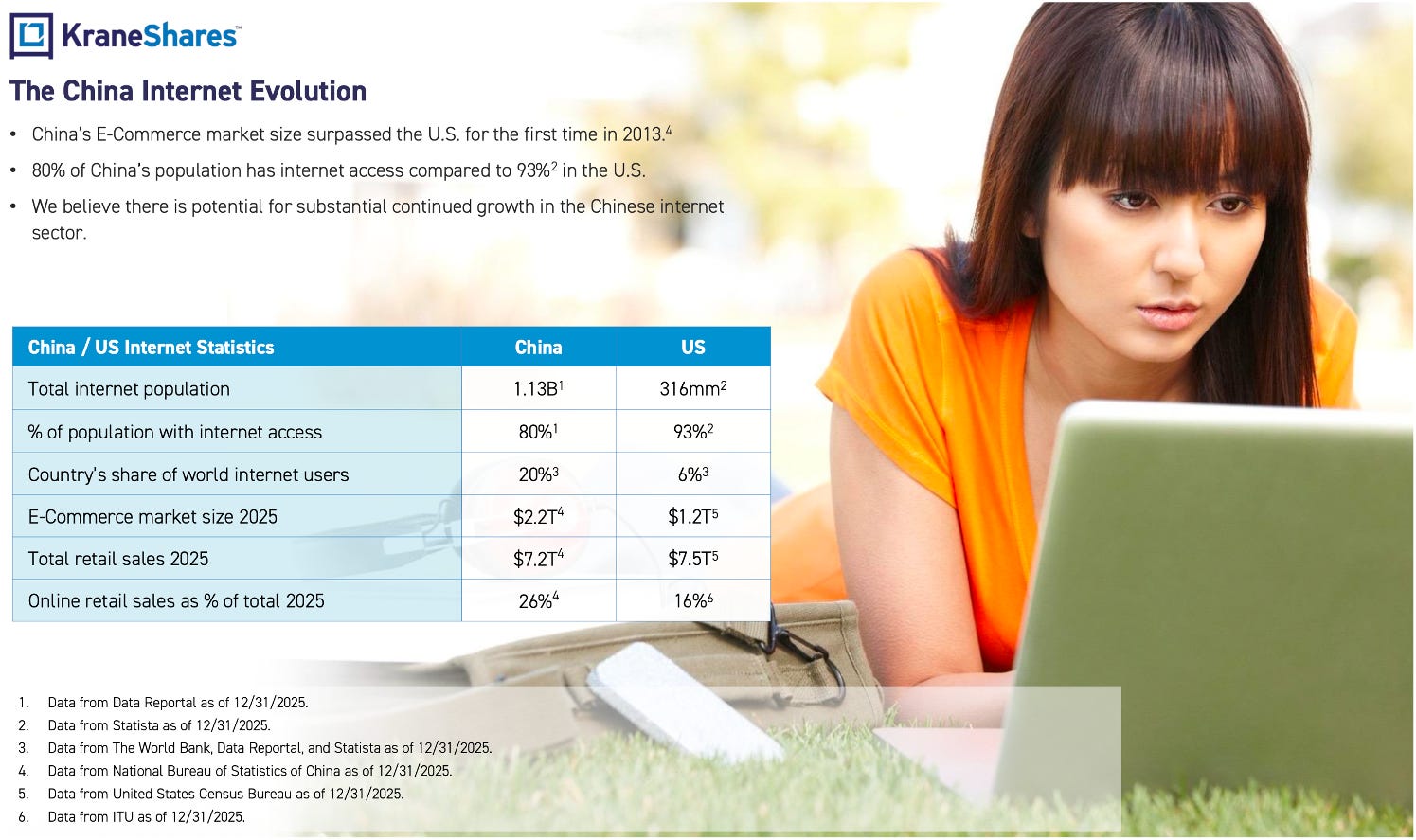

China has already built one of the largest digital economies in the world. Its ecommerce market is larger than America’s. Its internet population is more than three times the size of the U.S. equivalent. Online retail already represents a much larger share of total retail sales than in the United States, yet internet penetration is still meaningfully lower.

That combination is rare: enormous scale, deep digital behavior, and still some room for incremental penetration.

But the more important point is not just size.

It is embeddedness.

China’s technology platforms are not sitting politely beside the real economy. In many cases, they are the interface through which the real economy already operates. Payments, commerce, food delivery, travel, ride hailing, entertainment, healthcare, merchant services, logistics, advertising, cloud, and consumer finance have been pulled into digital ecosystems with a speed that more mature Western markets often struggle to replicate.

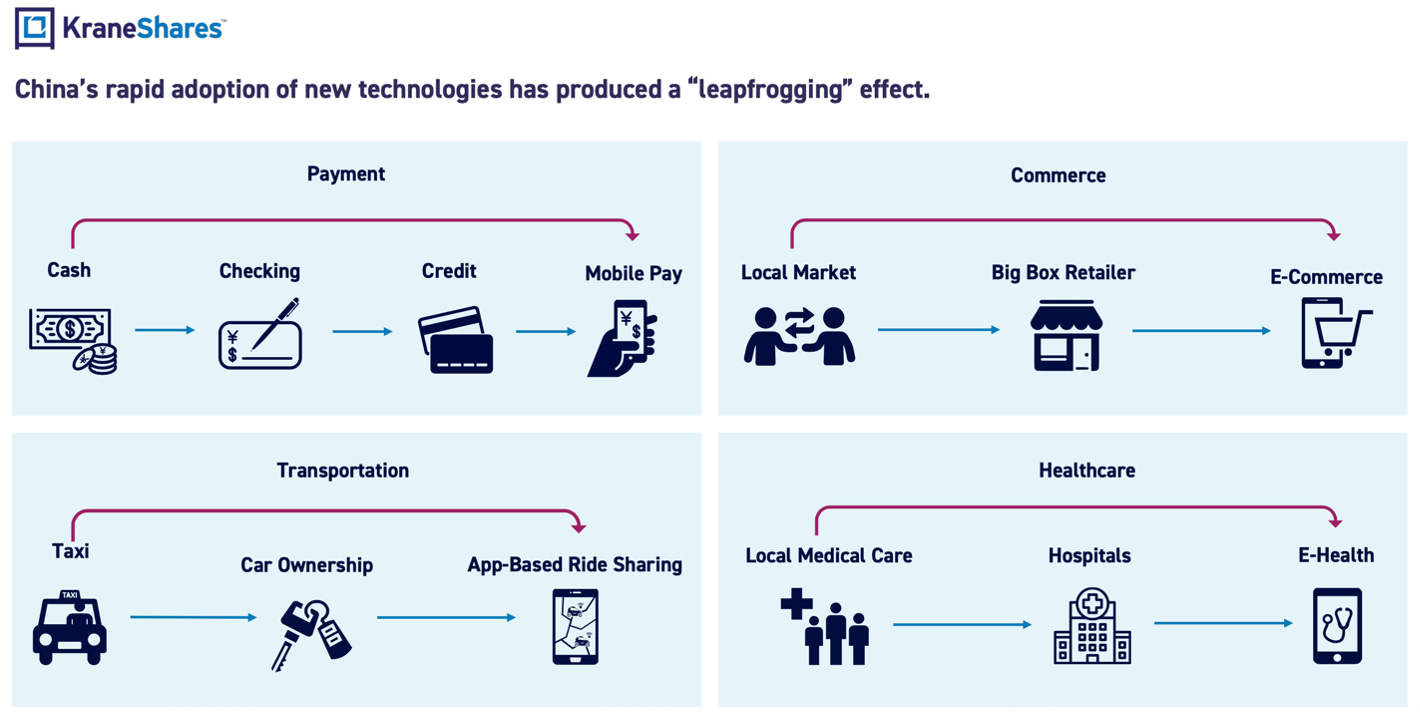

That is the leapfrogging effect1.

China did not need to follow the same path from cash to checking to credit cards before reaching mobile payments. It skipped steps. It did not need to build the same big-box retail infrastructure before embracing e-commerce. It skipped steps. It did not need to preserve every legacy interface in transportation, healthcare, and local services before moving activity onto digital platforms.

Again, it skipped steps.

That is important because AI adoption may reward the same instinct.

A society already accustomed to using digital platforms as the operating layer of daily life may be unusually fertile ground for AI applications. The rails are already there. The users are already there. The merchants are already there. The data exhaust is already there. The habit formation is already there.

This is the part of China’s technology story the market may still be underpricing.

A Chinese consumer does not simply shop online. She pays, chats, orders food, books travel, hails cars, watches video, receives recommendations, interacts with merchants, manages services, and moves across platform ecosystems that are already data-rich and transaction-heavy.

A Chinese merchant does not merely advertise online. It lives inside platforms that touch inventory, payments, logistics, consumer targeting, financing, promotions, and customer acquisition.

That is not a narrow internet story.

It is an application-layer story.

And the more we study it, the more important the distinction becomes. Because if the next phase of AI is going to be about deployment rather than merely model training, China deserves to be taken seriously.

Not sentimentally.

Not ideologically.

Not because we want the China story to work.

But because the evidence no longer supports the lazy conclusion that China is simply a second-tier participant in this technology race.

A quick note on accountability.

We don’t publish these theses to be right on paper. We publish them to express edge in the real economy. Our Leaderboard shows the exact scorecard since inception, tracking every position, our compounding outperformance against the market, and the triple-digit winners we’ve captured along the way.

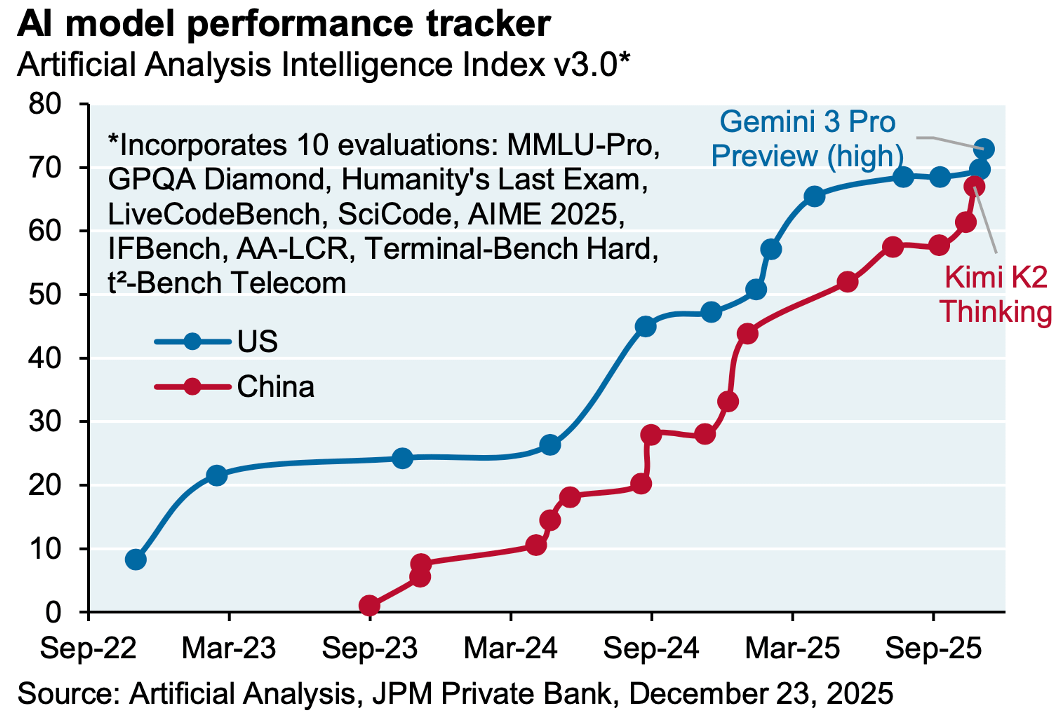

The frontier-model discussion still deserves attention, but the gap is no longer as static as many investors still assume. The chart below makes that clear:

The United States remains ahead, with Google’s Gemini 3 Pro still setting the pace in the broad model-performance rankings. But the more interesting observation is not simply who leads today. It is how quickly the field is compressing. And on that score, China’s progress has been striking.

In barely two years, Chinese models have moved from near-irrelevance in these rankings to a level that now forces them into the same conversation as the global leaders. Kimi K2 Thinking may still trail Gemini 3 Pro, but it is no longer sitting in another universe.

The direction of travel is what we should be watching.

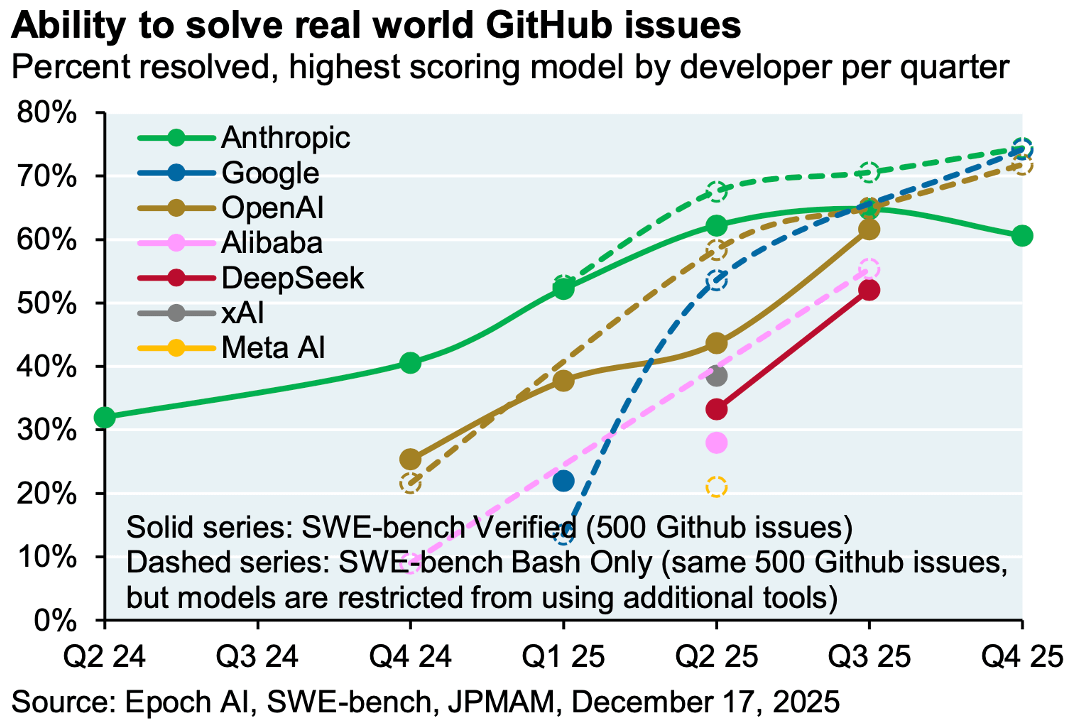

The same pattern appears when we move from broad benchmarks to something more practical. On the chart tracking the ability to solve real-world GitHub issues, the American leaders still occupy the top spots, but the Chinese challengers are no longer spectators...

Chinese models have entered the competitive set in a meaningful way. Their scores still lag the very best Western models, but they are now solving a material share of real coding problems, not just performing well on laboratory-style tests. That distinction is important because software development remains one of the clearest early use cases for AI in the real economy.

The question is no longer whether China can produce capable models. It clearly can. The question is how quickly those models continue to close the gap.

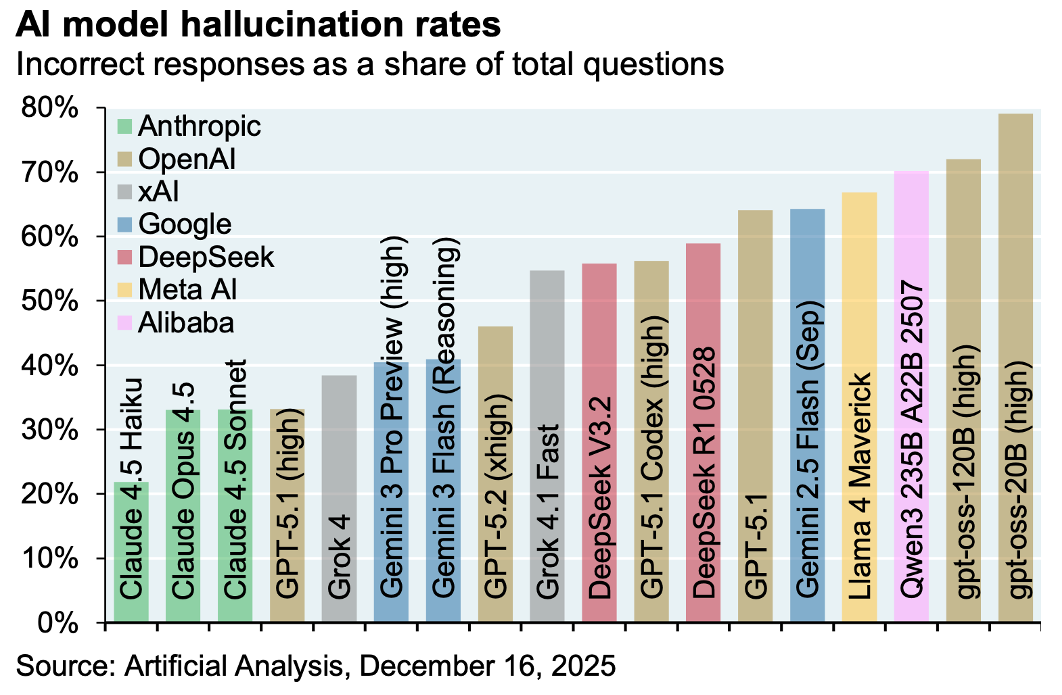

Reliability, however, is where humility is still needed.

The hallucination-rates chart shows that several Chinese models remain more error prone than the best offerings from Anthropic and OpenAI. That matters because, in AI, intelligence without consistency still leaves a lot of value on the table. But even here, the lesson is not that China is absent from the race. It is that China is already in the race, just not yet leading it.

And for us, that is more than enough.

Our investment case does not require China to dominate the frontier-model layer. It only requires China to be good enough, to improve fast enough, and to sit inside an ecosystem that is unusually well positioned to commercialize AI at scale.

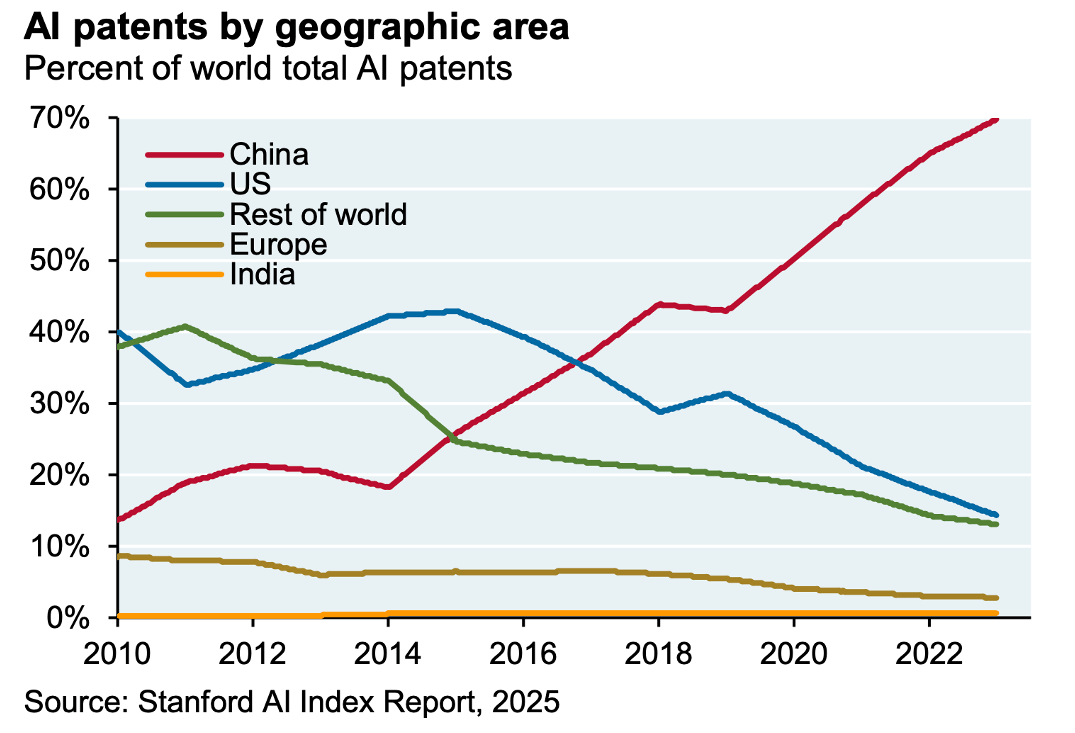

The patent data points in the same direction.

Now, we should be careful here. Patents are not profits. They are not moats. And in China, as elsewhere, they can sometimes tell us more about policy incentives than commercial outcomes.

China has been climbing the innovation food chain for years.

It has broken into the top tier of global innovation rankings, its export complexity has converged meaningfully with the United States, and its share of global AI patents has moved from marginal levels a decade ago to a commanding position today. The same pattern appears in clean-energy patents and even in nuclear science and engineering research, where China has moved from the periphery to the center of the global research base.

That is not the footprint of an economy simply waiting to import the next technological wave.

It is the footprint of a country trying to build the entire stack.

Models. Applications. Robotics. Manufacturing. Power. Transmission. Nuclear. Clean energy. Industrial automation.

Some of this will be wasteful. Some of it will be subsidized. Some of it will produce poor returns on capital. That is what happens when the state pushes aggressively into strategic industries. But some of it will also work. And when it works, it can scale very quickly.

That is the real point.

The application-layer thesis is not just that China has a large digital consumer base. It is that China has the technological capacity to keep improving the models, the industrial capacity to deploy them, and the social infrastructure to absorb them into daily life faster than many investors expect.

Then comes the other bottleneck.

Power.

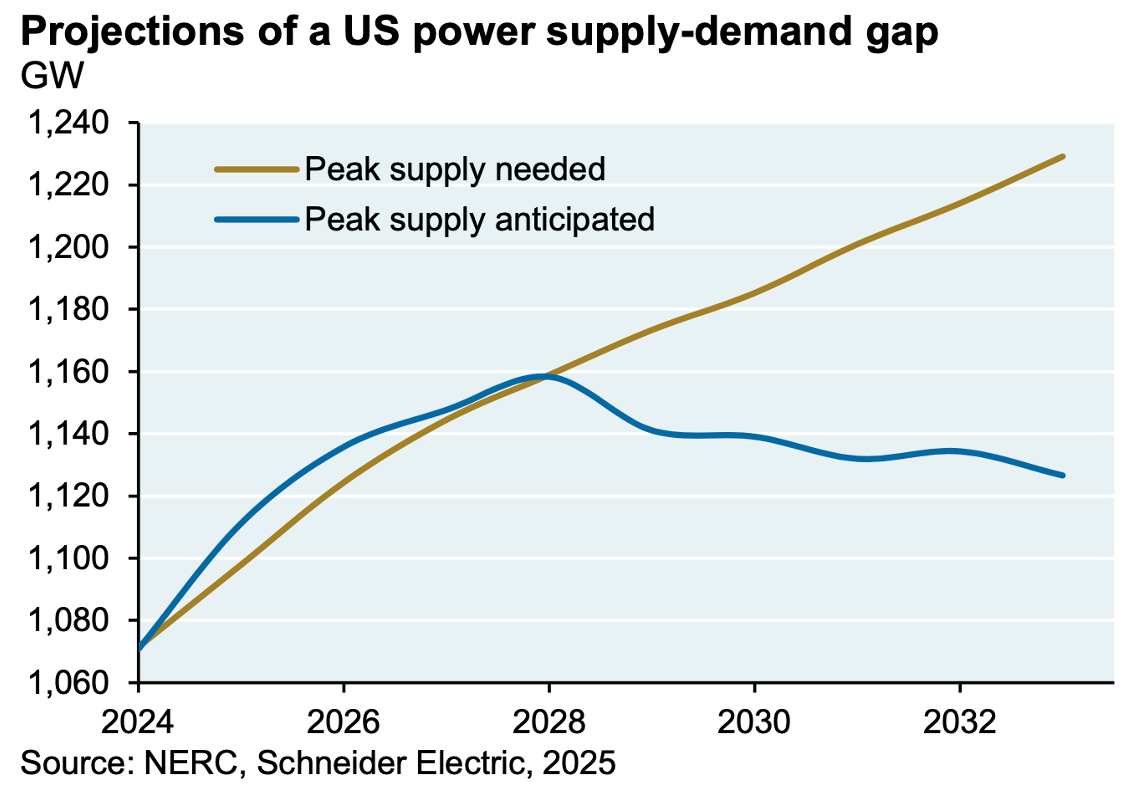

Because AI is not merely a contest of models and applications. It is also a contest of electricity. The country that wants to push AI into factories, logistics networks, robots, vehicles, cloud platforms, consumer services, payments, and industrial systems needs an enormous amount of reliable power behind it.

And here, China’s position looks very different from America’s.

The U.S. is discovering that power may be one of the hard limits of the AI boom. Data-center demand is rising into an electricity system that was not built for a sudden step-change in load growth. Peak supply needs are expected to keep rising, while anticipated supply is not keeping pace.

The gap is enormous.

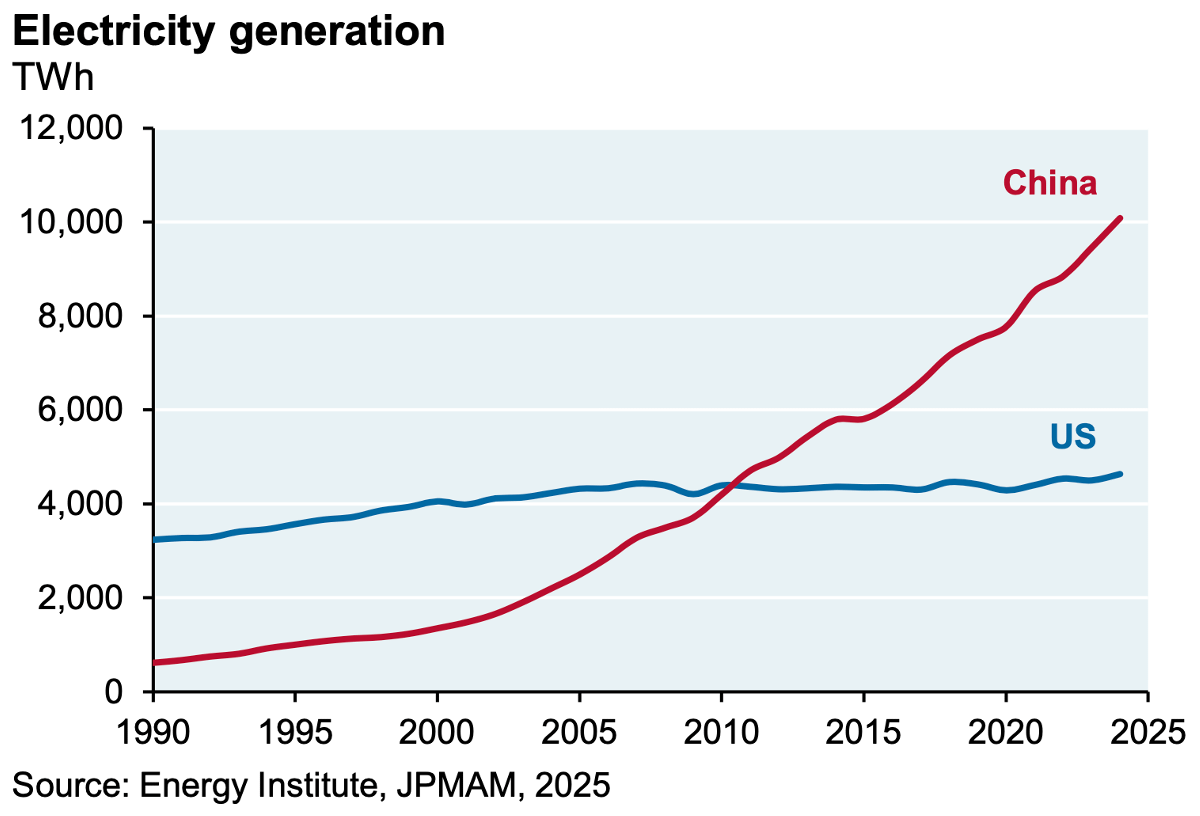

China, by contrast, has been increasing electricity generation at a scale that is difficult for the West to comprehend.

You might also like reading:

Based on Energy Institute data, Chinese power generation has risen by roughly 2,500 TWh since 2019, compared with only 221 TWh in the United States and a decline of 110 TWh in Europe. And this is not merely a coal story. China has been adding generation across essentially every major source, electrifying final energy consumption faster than any other major economy, and leading the world in the deployment of high-voltage direct-current transmission lines, which are crucial for moving electricity across long distances.

That does not make China’s energy system clean.

It is not.

Coal still plays a major role, and the environmental, efficiency, and capital allocation questions are real. But from the perspective of the AI race, perfection is not the test. The test is whether China has the ability and willingness to build the physical capacity required to support a much more electrified, automated, and AI enabled economy.

And on that question, the evidence is hard to ignore.

This is why the China application-layer thesis is more interesting than a simple “cheap internet stocks” argument.

China has the users.

It has the platforms.

It has the embedded digital behavior.

It has increasingly competitive models.

It has a rapidly expanding patent base.

It has manufacturing depth.

It has robotics ambition.

And it has a far stronger grip on the power side of the equation than the United States currently appears to have.

That combination is rare.

Scale. Embeddedness. Technological capability. Manufacturing depth. Power.

This is why China may be one of the most important application-layer markets in the AI cycle.

Not because it is cleaner than the U.S. Not because it is safer. And not because it leads across every part of the stack. But because it may be good enough where it needs to be good, unusually strong where deployment matters most, and far cheaper than a market with these attributes would normally be.

Which brings us to the uncomfortable part of the argument:

If China has so much scale, capability, and strategic relevance, why are Chinese assets still so cheap?

To answer that properly, we need to do what we always try to do before increasing exposure to a hated market:

We need to make the bear case first.

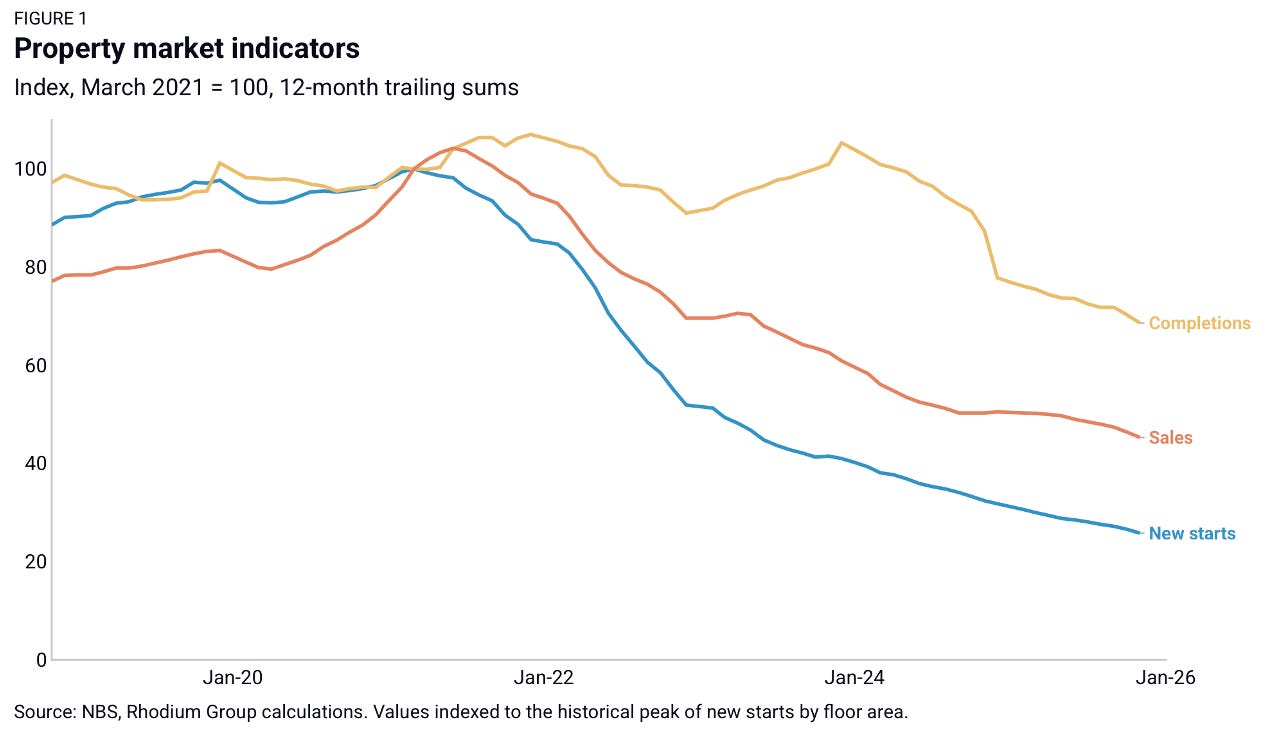

Let’s start with the obvious wound.

Property.

For years, real estate was not merely another sector in China. It was the household savings vehicle, the collateral engine, the confidence anchor, the local-government funding mechanism, and one of the main pillars of the country’s growth model.

So, when that machine began to reverse, the damage was never going to remain neatly contained inside the property market.

It spread into consumption.

It spread into confidence.

It spread into local-government finances.

It spread into the willingness of households to take risk.

And it created a deflationary impulse that is arguably larger, at least in balance sheet and confidence terms, than the U.S. housing shock that preceded the 2008 crisis. The comparison is not perfect. China’s bust is slower, more state-managed, and less brutally marked-to-market.

But property sits much deeper inside Chinese household wealth and economic activity: Brookings notes that average Chinese households hold about 70% of their assets in housing, while housing valuation is roughly five times GDP.

That is the macro scar.

And it is deep.

But it is also forcing a change in policy direction. If the old wealth engine was property, the new one increasingly has to involve financial assets, capital markets, technology, and consumption. Chinese authorities appear to understand this. Regulators have been encouraging insurers, pension funds, and mutual funds to increase equity exposure, while also reducing frictions in the fund industry to promote longer-term investment.

That does not solve the property problem overnight.

But it changes the direction of travel.

The second wound is policy trauma.

Global investors have not forgotten the crackdowns on internet platforms, fintech, private education, gaming, data, and other parts of the private sector. Nor should they. Those interventions did not merely reduce earnings forecasts. They damaged trust. And once trust is damaged, even good news gets discounted.

That is why the hardest question in China is not whether companies can innovate...

They clearly can. The harder question is whether shareholders will be allowed to capture enough of that innovation.

That uncertainty sits at the heart of the China discount.

The third wound is geopolitics.

The U.S.-China rivalry is no longer background noise. It runs directly through semiconductors, AI export controls, tariffs, sanctions, rare earths, capital flows, Taiwan, and investor access. The same technological ambition that makes China interesting also makes it strategically sensitive. And if China becomes more competitive in AI, robotics, clean energy, nuclear engineering, semiconductors, and industrial automation, the rivalry with the United States is unlikely to disappear.

It may intensify.

Then come the other familiar problems: weak private-sector confidence, deflationary pressure, demographics, youth unemployment, uneven corporate governance, currency risk, and years of foreign-capital exhaustion after too many false dawns.

So, we understand the pessimism.

In fact, we would be suspicious of any China thesis that did not begin there.

But this is also why we do not need to spend the rest of this issue re-litigating the entire China bear case. We have been covering it since the inaugural issue of VMF’s Strategic Asset Allocation, precisely because we have been overweight Chinese equities from the beginning. The risks were visible then. They remain visible now.

What has changed is the opportunity set.

Back then, Chinese equities were cheap because investors had lost confidence.

Today, they are still cheap, but the application-layer AI case has become much stronger. At the same time, the obvious AI trades elsewhere have become much more expensive, while our South Korea position has already delivered the kind of return that forces us to ask where the next pocket of asymmetry may be hiding.

That is why we now believe the China opportunity may be even more attractive than South Korea was at the beginning of 2025.

Not because it is safer.

It is not.

Not because the visibility is higher.

It is not.

But because the market may be making a similar mistake in a different layer of the AI stack. In South Korea, it underpriced the hardware and memory opportunity. In China, we believe it may now be underpricing the application layer.

The opportunity is murkier.

The risks are higher.

But the valuation is much cheaper.

And the potential re-rating may be just as powerful.

The question that remains is simple:

How should we increase this exposure... and by how much?

The Leapfrogging Effect describes how an economy can skip older stages of development and move directly to newer technologies. In China, this meant moving from cash to mobile payments, from traditional retail to e-commerce, from taxis to app-based ride sharing, and from fragmented local services to digital platforms. This matters for AI because societies already accustomed to rapid platform adoption may be better positioned to absorb new AI applications into daily life.

Hi VMF

You should use

Application Layer Intelligence Economy Engine instead of Marketplace Intelligence Engine which you have mentioned in PDD article

Economy is a deeper than Marketplace in the economy depth and scale.