The Hike That May Never Come

3 productivity reviews that could erase the year’s most anticipated rate hike before the Fed cuts a single basis point.

A contrarian thesis is easy to admire before the market tests it.

The real work begins when the tape turns hostile.

Over the past two weeks, readers of VMF’s Market View have watched our Dovish Shock thesis develop in public.

It began with the labor market. Payrolls surprised to the upside, wage pressure remained relatively contained, and investors treated economic resilience as an inflation problem.

Then came The Setup for a Dovish Shock, where we argued that improving productivity, technological investment, and changing supply dynamics could eventually force the market to reconsider the policy path.

In The Invisible AI Rails, we showed why that debate reaches far beyond the bond market. Crypto, precious metals, software, China internet, and other liquidity-sensitive assets are already trading inside it.

Then Kevin Warsh chaired his first Federal Reserve meeting.

The market’s verdict was immediate.

Hawkish.

Rates remained unchanged, but almost everything surrounding the decision pointed toward tighter policy. Forward guidance became thinner. Price stability took center stage. The new projections leaned toward rate increases. Traders rapidly pushed the probability of a hike even higher.

On the surface, our thesis had just met its contradiction.

Good.

That is when a thesis becomes useful.

The first reading of the meeting was clearly hawkish. The second was more interesting.

The Committee was divided almost perfectly between higher rates and no change. Warsh declined to submit his own projection. He described the forecasts as being written in pencil, with large erasers. And one of his first acts as Chair was to reopen the Fed’s frameworks for productivity, inflation, employment, economic data, communications, and the balance sheet.

Meanwhile, the energy shock that helped drive the inflation scare began to reverse.

Oil surrendered much of its war premium as the preliminary agreement between the United States and Iran reopened the Strait of Hormuz, improved the outlook for supply, and weakened one of the strongest arguments for renewed tightening.

The market is now pricing a hike just as one of the forces behind that hike may be disappearing.

That does not guarantee a dovish outcome.

It creates asymmetry.

A Dovish Shock does not need to begin with an emergency cut or a dramatic surrender from the Fed. It can begin much more quietly, with investors discovering that the expected hike is never coming.

When the market moves from pricing one or two increases to accepting that rates may simply remain unchanged, financial conditions can ease before the Fed cuts a single basis point.

That is the setup explored in the excerpt below.

It is our post-mortem on Warsh’s first meeting, the split inside the Committee, the reversal in oil, and the market reaction that may matter more than the headline itself.

Read it with one question in mind:

What happens when the most widely anticipated rate hike of the year quietly disappears?

The full June issue of VMF’s Security Selection goes one decisive step further. We identify the stock-level expression we believe offers exceptional torque if this repricing begins, build the complete bear, base, and bull valuation, and add the position to one of our Model Portfolios.

This free excerpt gives you the macro stress test.

Paid subscribers received the investment decision.

Good reading.

If you have already read the June issue of VMF’s Strategic Asset Allocation, you know where we stand: we believe the market remains vulnerable to a dovish shock.

Not merely one interest-rate cut appearing slightly earlier than expected. We are referring to something broader: a potential reset in the way investors think about inflation, economic growth, and monetary policy

The market has spent much of the past several months returning to a familiar equation:

Stronger growth means higher inflation.

Higher inflation means a more hawkish Fed.

And a more hawkish Fed means higher rates for longer... or even renewed rate increases.

Our working hypothesis is that this equation may be incomplete.

If economic growth is increasingly being driven by productivity, technological investment, and improved operating efficiency, then stronger growth does not necessarily need to produce stronger inflation. The economy may be capable of growing faster without generating the same degree of wage pressure and pricing power that investors have learned to fear.

We will not repeat that entire thesis here.

That was Tier One’s job.

But only one week has passed since we published it, and enough has already happened to put the hypothesis through a serious test.

Kevin Warsh has now chaired his first Federal Open Market Committee meeting.

And the market’s verdict was immediate:

Hawkish.

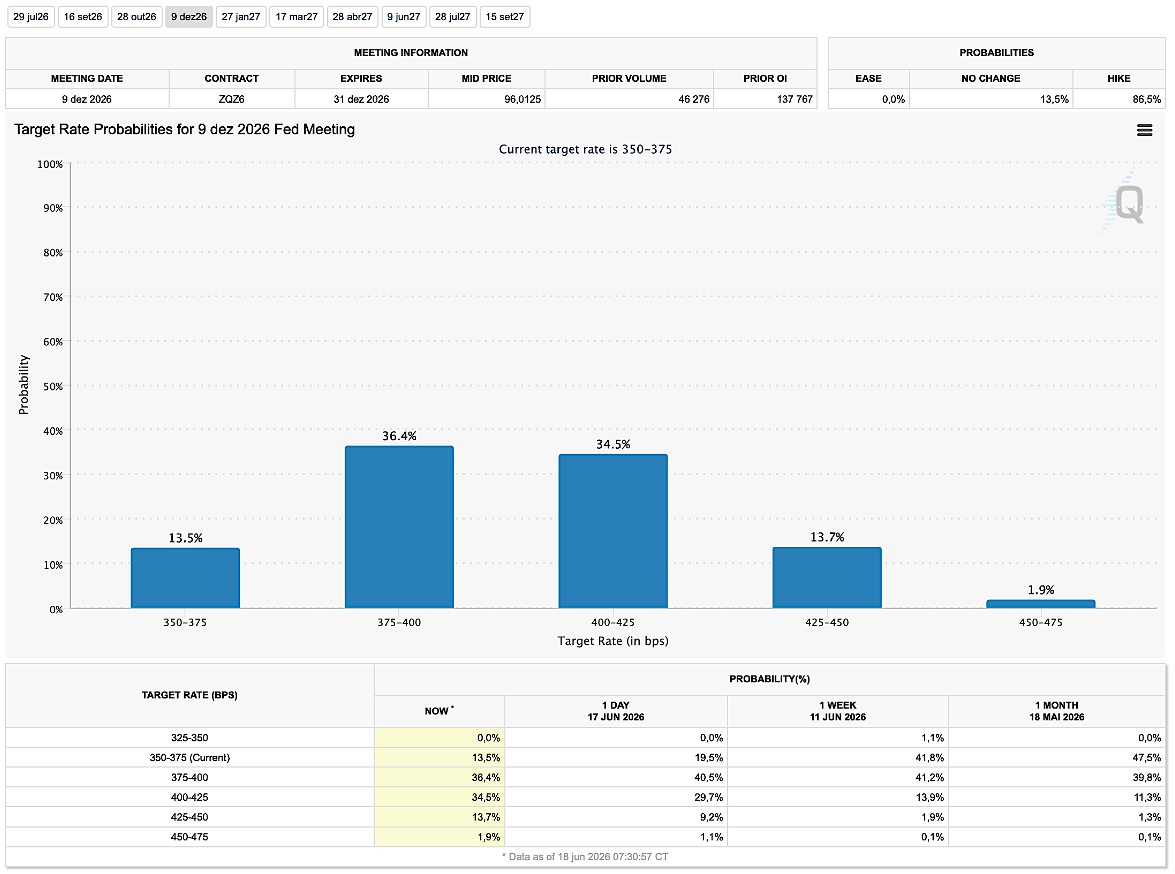

The Fed kept interest rates unchanged at 3.50%–3.75%, which surprised no one.

Everything surrounding that decision did. The statement placed far greater emphasis on price stability, while conventional forward guidance disappeared.

The projections were equally striking... but less one-sided than the headline suggested. Nine policymakers expected at least one interest-rate increase before the end of 2026, with six anticipating more than one. Yet eight projected no change, while only one expected a cut.

Warsh repeatedly stressed that inflation remains too high and that the Committee will deliver price stability.

The dollar jumped.

Treasury yields moved higher.

Equities fell.

Gold, silver, Bitcoin, and Ethereum were all sold.

At first glance, this appears to be the exact opposite of the Dovish Shock we described last week.

And we need to acknowledge that, honestly.

The Dovish Shock did not arrive at Warsh’s first meeting. Quite the opposite. At the very least, a mini hawkish shock did. But that is not the end of the analysis.

It may only be the beginning.

Gold, silver, Bitcoin, and Ethereum are among the market’s most sensitive barometers of real rates, dollar liquidity, monetary expectations, and risk appetite.

If the Fed had delivered an unequivocally hawkish regime change (and if investors had accepted that a durable tightening cycle was now beginning) we would have expected these assets to break decisively lower.

They did not.

All four sold off after the meeting. But, as of this writing, none has made a fresh lower low. Each remains above an important area of support, and the broader technical structures remain constructive.

That is not proof that our thesis is correct.

Markets can pause before falling again.

Support can break.

And one day of resilience should never be mistaken for final confirmation.

But the failure to make new lows matters because the meeting produced nearly every headline a precious-metals or crypto investor should have feared: a stronger dollar, higher yields, renewed hike projections, no forward guidance, and a chair determined to re-establish the Fed’s inflation-fighting credibility.

The assets bent. They did not break.

That suggests at least part of the hawkish message may already have been reflected in positioning and prices. It also suggests that investors may have heard more in Warsh’s press conference than the headline summary captures. Because although the immediate policy message sounded hawkish, the institutional message was far more nuanced.

Warsh confirmed something we have been expecting:

A new era at the Federal Reserve has begun.

Powell’s Fed spent years guiding markets toward its next decision. Officials communicated frequently. Policy changes were prepared through speeches, interviews, carefully adjusted statements, and a dot plot that investors often treated as a roadmap.

Warsh appears to have a very different philosophy.

The Fed may no longer hold the market’s hand.

Forward guidance, in its existing form, is gone.

Warsh refused to offer a view on the next meeting. He did not submit his own interest-rate projection. He said he did not regard the dot plot1 as particularly helpful and heard little conviction behind the forecasts his colleagues submitted.

That last point deserves attention.

The headline was that nine officials projected at least one hike. But eight projected no change, one projected a cut, and the chair himself declined to participate. That is not a Committee united behind a tightening cycle. It is a Committee divided almost perfectly in half, with an unusually consequential missing vote.

And Warsh described the forecasts as being written in pencil. With large erasers.

The dot plot delivered a hawkish shock, but even the new chair warned investors not to mistake it for a commitment.

Warsh also announced five major reviews covering the Fed’s communications, its balance sheet, the economic data it uses, its productivity and employment framework, and its understanding of inflation.

That list could hardly be more relevant to the thesis we presented last week.

One of those reviews will specifically examine the reach of artificial intelligence and other general-purpose technologies across productivity and employment.

That is a direct validation of our working hypothesis.

We have argued that the Fed and the market may be relying on economic relationships that no longer describe the economy particularly well. Payroll growth does not automatically imply wage inflation. Stronger output does not automatically imply overheating. And technological diffusion may be changing both the productive capacity of the economy and the bargaining power of labor.

Warsh is not yet using that argument to justify lower rates.

We should not pretend otherwise.

At his first meeting, he emphasized inflation, not productivity, as the immediate policy priority.

But the fact that the new chair is reopening the Fed’s productivity, jobs, inflation, data, communications, and balance-sheet frameworks simultaneously tells us that he does not believe the old framework is adequate.

That is important.

The policy may look hawkish today.

But the analytical machinery beneath it is being rebuilt. And because the Fed will now provide markets with less guidance, future changes in that framework may not be introduced gradually.

Under Powell, the Fed usually prepared investors before it changed direction. Under Warsh, investors may be forced to discover that change through the data, and through the decision itself.

That will probably mean more volatility.

But more volatility also means more opportunity.

If markets receive less information, expectations can move further away from reality. Positions can become more crowded. Wrong assumptions can survive for longer. And when the underlying facts finally force a reassessment, the adjustment can become far more violent.

The absence of forward guidance cuts both ways.

The first surprise was hawkish.

The next one does not have to be.

And almost on cue, the first major challenge to the Fed’s newly hawkish narrative has already arrived. Because, just as policymakers marked up their inflation and interest-rate projections, the energy shock underpinning much of that concern began to reverse.

The war with Iran has reached its most significant diplomatic milestone so far.

The United States and Iran have signed a memorandum of understanding intended to end the conflict, reopen the Strait of Hormuz, restore maritime traffic, permit renewed Iranian oil exports, and create a 60-day window for negotiating a broader agreement.

This is not yet peace.

Either side can still walk away. Implementation disputes remain. Israel and Lebanon could complicate the ceasefire. Shipping may take time to normalize. And President Trump has made clear that military action could resume if the agreement fails.

But markets rarely wait for certainty. They react to changes in direction.

And the direction has changed materially.

As the previous chart shows, oil prices have continued to retreat and are now testing major technical support, including the 200-day moving average, represented by the red line.

Brent, in particular, has surrendered most of its war premium and returned toward the zone from which the conflict-driven advance began. At the same time, the fundamental backdrop is softening: Iraqi production is recovering, tankers are repositioning toward the Gulf, Iranian exports may resume, and the IEA now expects global oil consumption to fall far more sharply than it previously projected, while warning that a successful peace agreement could contribute to renewed oversupply in 2027.

And here lies the tension at the heart of the current setup: the Fed’s hawkish shift was heavily influenced by the energy shock.

The new projections were formed in a world of disrupted Gulf supply, a closed Strait of Hormuz, oil above $100, rising headline inflation, and fears that higher energy costs would spread through the rest of the economy.

That world may already be changing.

The Fed itself acknowledged that part of the recent inflation increase reflected sector-specific supply shocks, including energy. If oil continues to fall, the market will eventually have to answer an uncomfortable question:

Why should a temporary supply shock produce a durable tightening cycle after the shock itself has begun to reverse?

That is where the Dovish Shock setup we presented last week becomes more, not less, interesting.

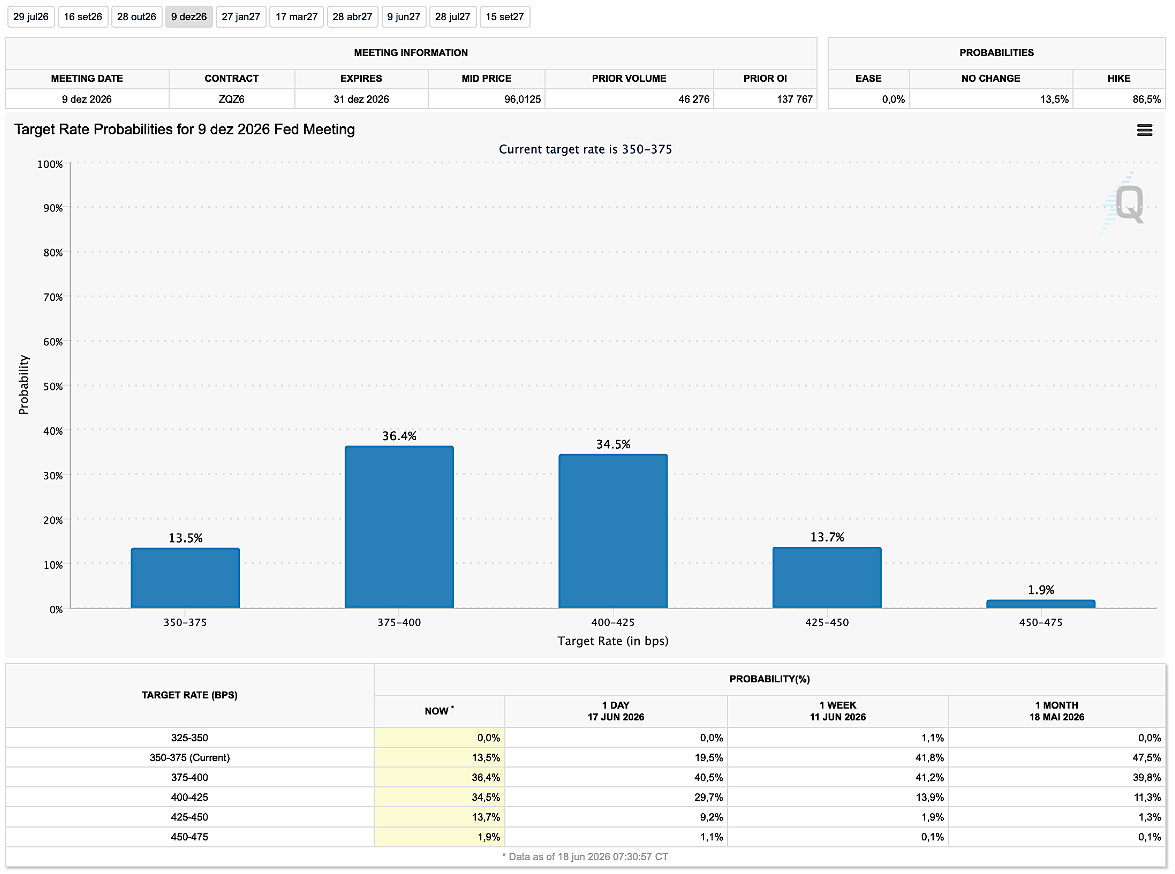

The market has now moved beyond merely fearing higher rates. As the table below shows, it is pricing a hike.

And that is what makes the setup increasingly asymmetric.

The hurdle for another hawkish surprise has risen.

The hurdle for a dovish one has fallen.

Remember, the first stage of the Dovish Shock we anticipate does not require the Fed to begin cutting rates tomorrow. It requires only a change in the direction of expectations.

If the market moves from believing that the Fed’s next move will be a hike to accepting that policymakers are likely to remain on hold, financial conditions can begin easing long before the first rate cut arrives. And if inflation continues to cool, that pause could eventually give way to outright easing.

That is how a Dovish Shock can begin without the Fed cutting a single basis point.

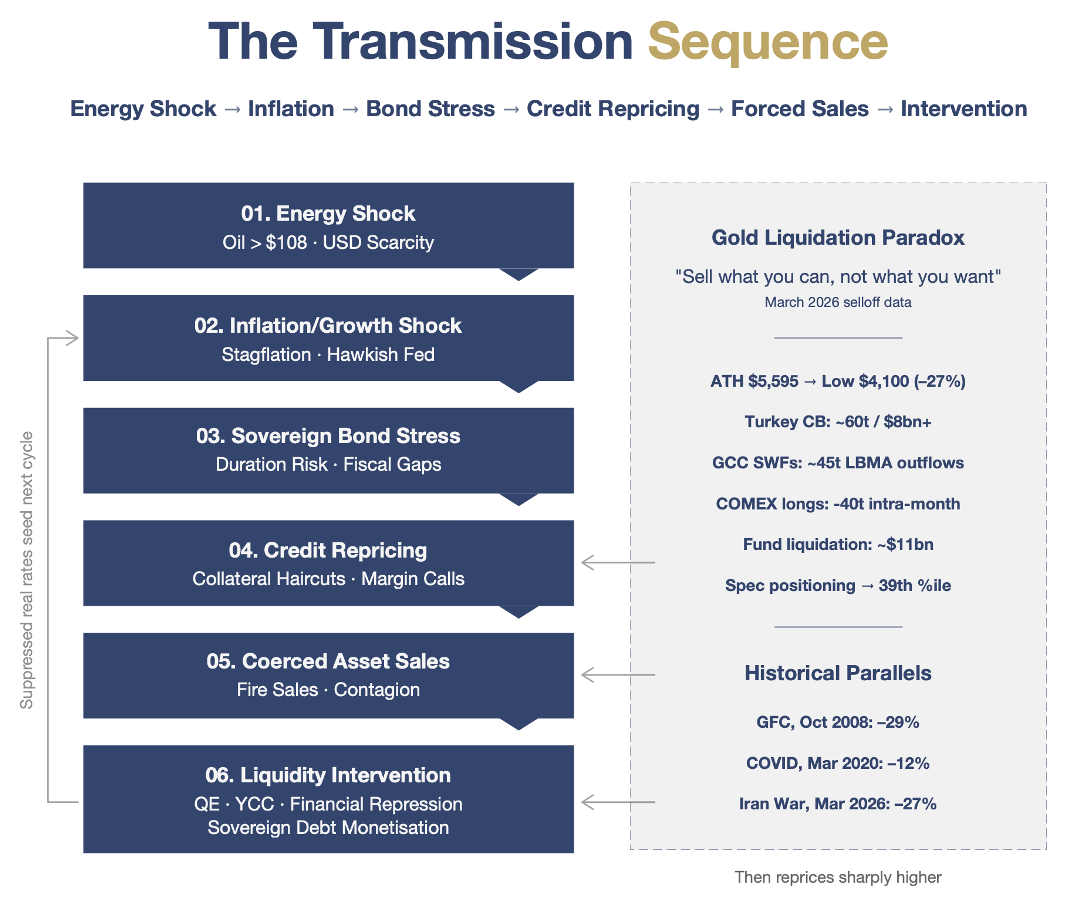

The latest In Gold We Trust Report captures the broader mechanism particularly well. As the chart on the previous page shows, the sequence is often straightforward:

An energy shock lifts inflation.

Higher inflation tightens financial conditions.

Bond and credit markets come under pressure.

Investors sell liquid assets.

And, eventually, policymakers are forced to respond.

We are not claiming that every stage must unfold exactly as it did in 2008 or 2020. But the broader lesson is important: the assets that suffer during the tightening phase can become the largest beneficiaries when the policy response changes.

We already own several positions that should benefit disproportionately if our Dovish Shock thesis proves correct.

Coinbase gives us leverage to a recovery in crypto liquidity and trading activity.

Bitmine offers even more direct exposure to Ethereum. And Altius Minerals remains our preferred high-quality, royalty-based expression of the long-term precious metals and real-assets cycle.

But this time, we want something different... We want silver torque.

We want a company whose earnings, cash flow, and equity value can respond far more aggressively than the metal itself if silver resumes its advance.

For that role, we believe in a perfect candidate.

Subscribe to get it on your inbox.

The top-down setup may be approaching a turn.

The bottom-up case is already in place.

And when both begin pointing in the same direction, that is when VMF’s Security Selection should act.

You might also like reading

Disclaimer

The information provided herein is for general informational purposes only and does not constitute financial advice or a recommendation to buy, sell, or hold any investment. It is not tailored to any specific individual or investor profile. All investments involve risks, and past performance is not indicative of future results. Before making any investment decisions, it is important to consider your own financial situation and risk tolerance. We do not guarantee the accuracy, completeness, or reliability of any information provided, and we disclaim any liability for any loss or damage arising from reliance on the information herein. Readers are advised to consult with an authorized financial intermediary before making any investment decisions.

A quick note on accountability.

We don’t publish these theses to be right on paper. We publish them to express edge in the real economy. Our Leaderboard shows the exact scorecard since inception, tracking every position, our compounding outperformance against the market, and the triple-digit winners we’ve captured along the way.

The Fed’s dot plot shows where each FOMC participant believes the federal funds rate should stand at the end of the coming years and over the longer run. Introduced in January 2012, it was intended to make policymakers’ thinking more transparent, but markets often treat the anonymous dots as firm guidance rather than conditional judgments. Warsh has challenged that practice. He declined to submit his own dot at his first meeting and placed the entire framework under review, arguing that such projections can become misleading when economic conditions change quickly.