The Invisible AI Rails

The 3 AI trades: How crypto rails monetize the agentic economy.

Crypto has spent the past few months doing what it does best when confidence breaks: punishing believers, rewarding cynics, and making every long-term thesis look foolish.

That is exactly why this moment deserves serious work.

The easy response is ideological. The bulls dismiss the damage. The bears declare the entire cycle finished. Neither approach is useful when capital is at risk.

So, in this excerpt from June’s issue of VMF’s Strategic Asset Allocation, we begin with the evidence against us.

The bear case is deep.

A hawkish repricing of the Fed. ETF outflows. Retail capitulation. Speculative deleveraging. Technical breakdowns. Capital being drained toward the most visible AI trades and mega IPOs. New questions around Bitcoin treasury companies. Protocol-security failures. The long shadow of quantum computing.

These are not imaginary risks, and they should not be waved away by anyone serious about investing in the asset class.

But price damage and thesis damage are not always the same thing.

Crypto is still being priced largely as a volatile liquidity trade. When yields rise, liquidity expectations weaken, or investors need cash, it gets sold quickly and indiscriminately.

Beneath that liquidation, however, a more important use case may be taking shape.

AI Agents will need to do more than generate answers. They will need to authenticate, hold value, make payments, settle transactions, access paid services, prove authorization, and interact economically with other machines.

That requires rails.

Wallets. Stablecoins. Digital identity. Programmable payments. Verifiable settlement. Blockchains capable of operating at software speed.

The market currently sees speculative wreckage.

We see parts of a financial stack that may become increasingly important to the agentic economy.

That does not mean every token wins, every network matters, or every decline should be bought. It means the long-term utility of the infrastructure may be improving while the short-term price action is deteriorating.

That tension is where important bottoms are often formed.

We may now be approaching the kind of bottom that investors can actually monetize, rather than recognize comfortably months later. Confirmation still matters. Position sizing still matters. The chart still matters. But the asymmetry is becoming increasingly difficult to ignore.

The analysis that follows presents the full bear case before making the bull case.

Because conviction that cannot survive hostile evidence is not conviction.

It is marketing.

Good reading.

Crypto does not look like an AI trade right now.

That is precisely why we need to study it.

The market already knows how to price the visible side of AI. It can see the chips, the memory, the data centers, the grid constraints, the power demand, and the physical infrastructure behind the intelligence layer. That was the first trade. And as we have explained, we owned that trade through less obvious expressions before the market fully caught up.

EWY ( EWY 0.00%↑ ) was the cleanest example.

We did not own South Korea as a generic country allocation. We owned it because the market had not yet understood the importance of memory inside the AI buildout. High-bandwidth memory, DRAM, NAND, advanced packaging, Samsung Electronics, SK Hynix... these were not side characters. They were part of the physical stack required to make AI scale.

Then the market learned.

The position delivered extraordinary returns.

And we closed it.

Not because the thesis failed.

Because the thesis worked.

That is the lifecycle we want. Find the hidden bottleneck, let the market discover it, and harvest when the asymmetry changes.

Since then, we have been moving toward the less visible AI trades.

Software was one.

When we added IGV ( IGV 0.00%↑ ), the market was still treating software as an obvious AI loser. That was too blunt. Some software businesses will absolutely be disrupted. But others may become more valuable as AI improves their products, lowers development costs, automates workflows, and turns static software into intelligent software.

China’s application layer was another.

Through KWEB, and then more directly through PDD Holdings PDD 0.00%↑in VMF’s Security Selection and Alpha Tier, we moved toward platforms where AI can become monetization: better discovery, better pricing, better advertising, better merchant tools, better logistics, better fraud detection, and better matching between consumers and supply.

Revisiting the structural case for PDD:

Now comes the next question.

If the first AI trade was about building the machine. And the second AI trade is about using the machine. What is the third?

Our answer may sound strange at first: The rails that allow autonomous software to transact.

That brings us to crypto.

But before we make the bull case, we need to begin with the bear case. Because the bear case is real.

Why Crypto is Falling.

Bitcoin is not falling randomly.

The broader crypto universe is not under pressure because investors suddenly forgot the long-term promise of digital assets. Several forces have converged at once, and together they have created one of the most important tests for the asset class since the launch of the spot Bitcoin ETFs.

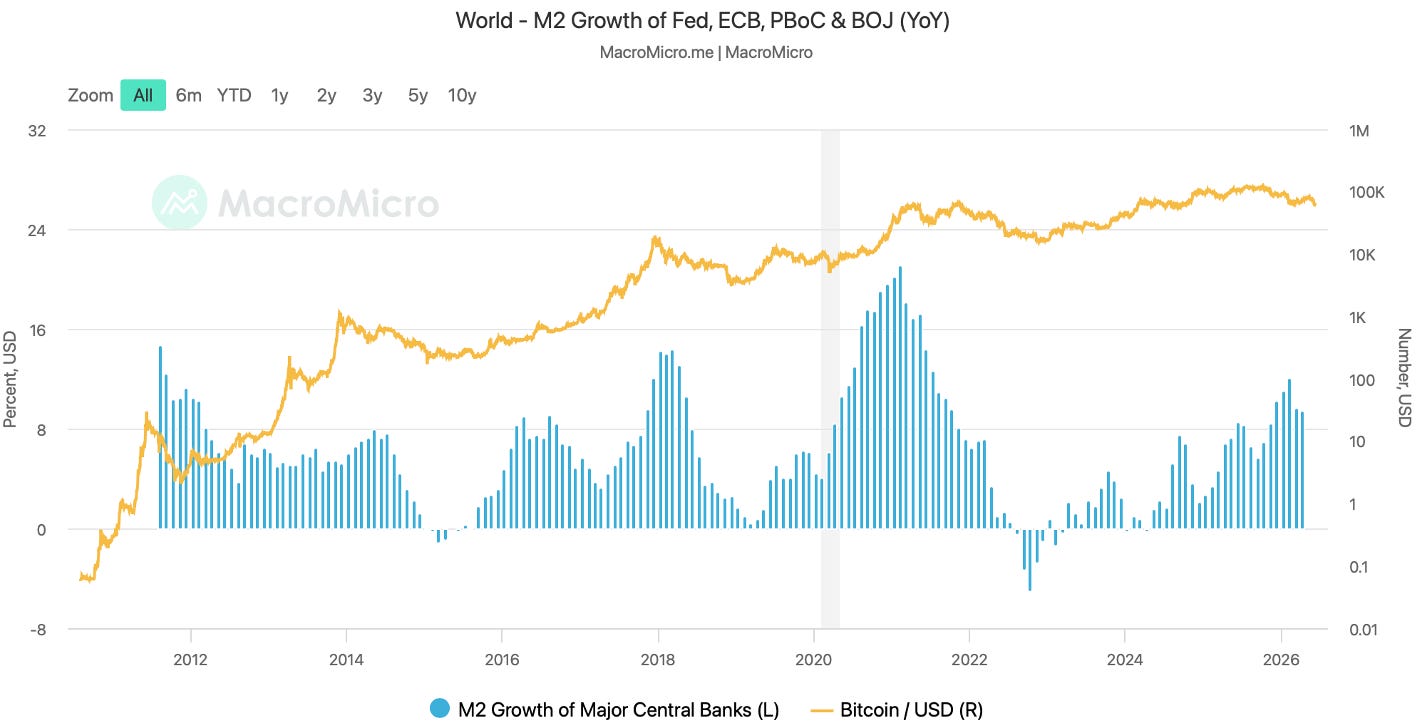

The first force is macro.

Crypto remains one of the purest liquidity assets in the world. It may have a long-term monetary role. It may have a long-term technological role. It may eventually become part of the infrastructure of digital settlement, tokenization, and agentic commerce.

But today, in public markets, it still trades like high-beta liquidity.

When investors expect easier money, Bitcoin usually benefits. When investors price a more hawkish Fed, Bitcoin usually suffers.

*Global M2 is a broad proxy for worldwide liquidity, measuring the amount of money circulating across major economies. Bitcoin has historically shown a strong relationship with Global M2, but the key signal is often not just whether liquidity is rising or falling. It is whether liquidity growth is accelerating or decelerating. When Global M2 expands at a faster pace, Bitcoin tends to benefit; when that expansion slows, Bitcoin can come under pressure even before the absolute level of liquidity turns lower.

That is exactly what happened after the latest employment report.

Stronger payrolls pushed yields higher, increased the probability of rate hikes, and forced investors to reprice the liquidity path. Bitcoin, Ethereum, Solana, crypto equities, and smaller tokens all felt the pressure.

The market did not need to decide that crypto was broken. It only needed to decide that liquidity was less friendly than it thought.

That was enough.

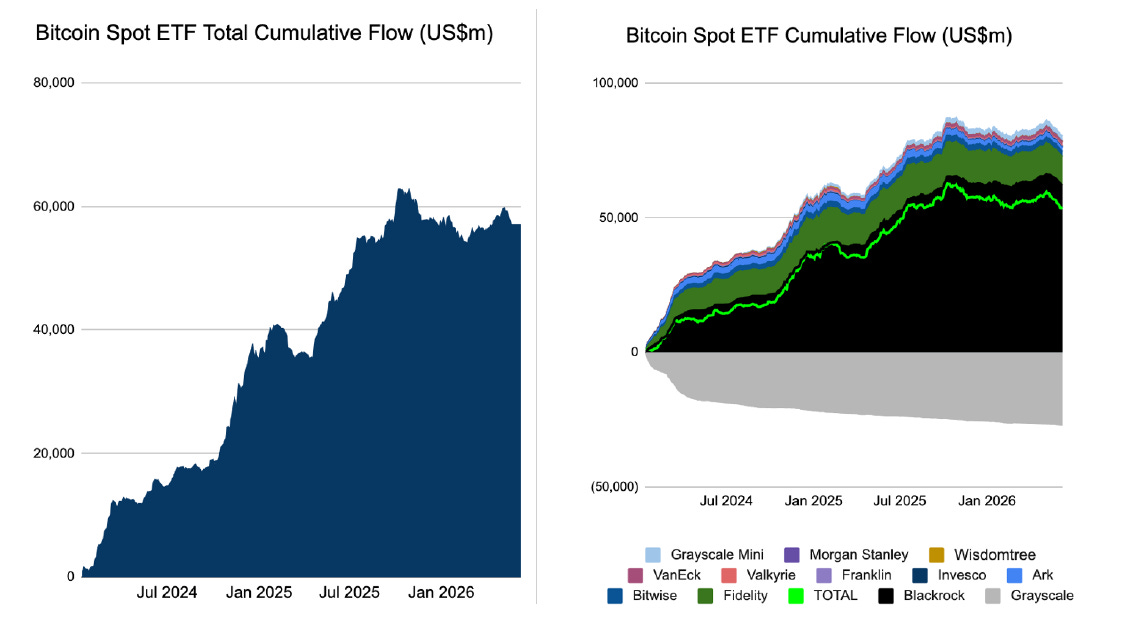

The second force is flows.

Recent ETF data show that investors have been pulling capital from Bitcoin products at a significant pace. This is important because the ETF structure changed the market. It made Bitcoin easier to own. It brought new capital into the asset. It legitimized the allocation for a wider investor base.

But that channel works both ways.

The same wrapper that makes it easier to buy also makes it easier to sell.

When macro pressure rises, when sentiment deteriorates, or when investors need liquidity, ETF flows can quickly become a pressure valve. In that sense, Bitcoin’s institutionalization is not only a source of upside. It is also a source of faster, more visible outflows during stress.

The third force is sentiment.

Retail sentiment is in the dust.

The speculative energy that surrounded crypto earlier in the cycle has faded dramatically. Funding rates have weakened. Outflows have intensified. The broader crypto universe has underperformed. And the psychology has shifted from excitement to exhaustion.

That matters because crypto is still heavily influenced by marginal retail buyers.

In equities, a deep institutional base can sometimes absorb retail fatigue. In crypto, retail and speculative capital still matter enormously at the margin. When those buyers disappear, prices can fall faster than fundamentals change.

The fourth force is speculative deleveraging.

Crypto sits inside a broader risk-taking ecosystem. It overlaps with leveraged ETFs, 0DTE options, meme stocks, high-beta growth, disruptive technology, altcoins, crypto treasury companies, and retail momentum.

When that ecosystem comes under pressure, crypto usually feels it quickly.

The market does not deleverage politely. It sells what is liquid. It sells what has volatility. It sells what can be turned into cash. It sells the assets with the most emotional ownership.

Bitcoin may be the institutional anchor of crypto, but the broader universe is still full of leveraged beta. Ethereum, Solana, smaller tokens, miners, treasury companies, and crypto-linked equities can all behave like amplified expressions of the same liquidity cycle.

That is why crypto selloffs often feel disorderly. They are not only fundamental repricings... they are positioning events.

The fifth force is liquidity absorption from the obvious AI trade.

This may be the most interesting pressure point of all.

The market is preparing for enormous capital events tied to the most visible parts of the technology boom: mega-IPOs, AI infrastructure financings, data-center-related equity raises, and the public-market arrival of companies investors already associate with the future.

Capital is not infinite.

If investors want to buy the next obvious AI story, they need cash. And when they need cash, they sell what they can.

Crypto is liquid. It trades constantly. It is volatile. It is widely owned by speculative capital. It is easy to use as a source of funds.

That gives us the irony at the heart of this issue:

The market may be selling one of the invisible AI trades to fund the obvious one.

The sixth force is Strategy MSTR 0.00%↑ .

This point requires nuance.

Strategy’s recent Bitcoin sale was tiny relative to its total holdings. Financially, it was almost irrelevant. Psychologically, it mattered much more...

For years, the company’s Bitcoin strategy was built around a simple message: accumulate, hold, never sell. So, when even a small sale occurs, investors begin to ask questions that did not seem urgent before.

Could Bitcoin treasury companies become marginal sellers?

Could preferred dividends, leverage, capital-structure complexity, and market discounts create new pressure points?

Could the financialization of Bitcoin introduce reflexive downside channels that did not exist in earlier cycles?

This does not invalidate Bitcoin. But it does remind us that every form of institutional adoption brings new market plumbing. And market plumbing can transmit stress in both directions.

The seventh force is protocol-security risk.

The recent Zcash episode was not a Bitcoin event. It was not even a crypto-wide protocol failure. But markets are not always careful during periods of stress. A critical vulnerability in a major privacy chain reminded investors that complex cryptographic systems can contain hidden risks, even after years of operation and audits.

That is especially relevant because many of the most exciting crypto use cases depend on technical complexity: zero-knowledge proofs, privacy pools, bridges, smart contracts, rollups, custody systems, interoperability layers, and programmable settlement.

Complexity creates power.

It also creates attack surfaces.

This does not mean the entire sector is unsafe. It means the sector is still young enough that security, verification, governance, and upgradeability remain central investment risks.

The eighth force is quantum computing.

This is not an immediate Bitcoin death sentence. It is often exaggerated by critics and misunderstood by casual observers. But it is not irrelevant. Bitcoin’s proof-of-work mining mechanism is far less vulnerable to practical quantum attack than many headlines imply. The more serious long-term concern is signature security: whether sufficiently powerful quantum computers could eventually threaten the elliptic-curve cryptography used in many digital-asset systems.

That risk is not here today.

But markets discount the future.

As quantum progress continues, institutions will increasingly ask whether digitalasset networks have credible paths toward quantum-resistant upgrades. The answer may ultimately be yes. Open-source networks can adapt. Cryptography evolves. Post-quantum standards are being developed. But the transition will require governance, coordination, incentives, and time.

So, quantum risk should not be treated as a reason to dismiss crypto. It should be treated as a reason to demand maturity from it.

Finally, there is the chart.

Bitcoin is testing a major long-term support zone, but the weekly and daily charts have already suffered meaningful damage. The broader crypto universe remains weak. Several support levels have broken. Momentum has deteriorated. And the burden of proof has shifted back to the bulls.

That is the bear case.

Macro pressure.

ETF outflows.

Retail capitulation.

Speculative deleveraging.

AI-related liquidity absorption.

Strategy (MSTR) narrative damage.

Protocol-security concerns.

Quantum overhang.

Technical weakness.

None of this should be dismissed.

But none of it necessarily destroys the long-term thesis either.

And that is where the opportunity begins.

The Bull Case Begins Where the Bear Case Ends

The strongest bull markets do not usually begin when the headlines look clean. They begin when the market has good reasons to be worried, but the price has already absorbed too much of the worry.

We strongly believe that may be the situation today.

Crypto is being treated as broken liquidity beta at the exact moment when its long-term relevance may be increasing. The market is looking at Bitcoin and seeing a risk asset that sold off when yields rose. It is looking at altcoins and seeing speculative wreckage. It is looking at ETF outflows and seeing disappointment. It is looking at Strategy and seeing a crack in the “never sell” story.

All of that is visible. What may be less visible is the infrastructure being built beneath the surface. Because AI is changing the question.

For most of the internet’s history, the problem was information.

How do we create it?

How do we organize it?

How do we distribute it?

How do we search it?

How do we monetize attention?

AI changes the problem.

When intelligence becomes abundant, the next bottleneck shifts toward action. A chatbot answers. An agent acts. An agent can search, compare, negotiate, book, pay, settle, verify, authenticate, and interact with other software systems. It can make decisions inside defined limits. It can use tools. It can transact on behalf of users or organizations.

Once that happens, the internet needs more than information rails. It needs economic rails.

That is where crypto becomes interesting again. Not the casino.

The rails.

AI agents need ways to hold value, send value, receive value, verify identity, prove authorization, access paid APIs, settle microtransactions, use digital services, and interact across platforms without a human manually approving every step.

The legacy financial system was not built for that. Banks require human identity. Card networks require human approval flows. Payment processors are optimized for merchants, not swarms of autonomous software agents. Cross-border settlement remains slow. Micropayments remain awkward. Machine-to-machine commerce remains underdeveloped.

Crypto was built around a different primitive.

A wallet.

A signature.

A transaction.

A settlement layer.

A verifiable record.

That primitive may be far more important in an agentic economy than the market currently appreciates. Stablecoins are the clearest example. They already allow digital dollars to move globally, programmatically, and with far less friction than many legacy payment systems. If AI agents need money that is always on, programmable, global, and capable of settling at software speed, stablecoins are an obvious candidate.

That is why recent infrastructure developments are so important.

Agentic payment systems are beginning to move from concept to implementation.

The relevant point is not that the current infrastructure is already mature... it plainly is not. The point is that major cloud, payments, and crypto-infrastructure companies are now building the plumbing through which AI agents can discover services, authenticate wallets, execute payments, settle in stablecoins, and receive verifiable proof that a transaction has occurred.

That matters because it hints at the emergence of a new financial layer for the internet. It will not arrive fully formed. It will be early, imperfect, and full of difficult questions around security, compliance, identity, fraud prevention, user permissions, spending limits, audit trails, and protocol design. But that is often what important infrastructure looks like before the market understands it. The first versions are usually clunky, the killer use case is rarely obvious in real time, and the investment opportunity often appears before the vocabulary around it has fully settled.

Then, gradually, the pieces begin to connect. APIs become paid resources. Agents purchase data. Models pay for tools. Software transacts with other software. Stablecoins become settlement rails. Wallets become agent accounts. Programmable blockchains become execution environments. Tokenized assets become machine-readable collateral and ownership records.

At that point, crypto stops looking only like a speculative corner of the market and starts looking like one possible financial operating system for autonomous digital activity.

That is the bull case.

Not that every token wins. Most will not. Not that every blockchain becomes systemically important. Most will not. And not that Bitcoin, Ethereum, Solana, Coinbase, stablecoins, tokenization, DeFi, and agentic payments are all expressions of the same trade. They are not.

Bitcoin is the monetary asset. Stablecoins are the payment layer. Programmable blockchains are the execution layer. Exchanges, custodians, wallets, and compliance systems are the tollbooths. Tokenized assets are the ownership layer. Together, they form a potential financial stack for a more automated internet.

The market is not pricing that today. It is pricing fear, outflows, Fed risk, technical damage, and the exhaustion of retail speculation. That is exactly why the setup deserves attention.

The market is selling crypto because it looks like liquidity beta. We are studying it because parts of the crypto stack may be becoming financial infrastructure for the agentic-AI economy.

That does not mean we buy blindly. A strong thesis does not cancel a weak chart, and a powerful long-term story does not remove the need for discipline, position sizing, and confirmation. But it does tell us where to focus our attention.

The issue, then, is not whether crypto is comfortable. It is not. The issue is whether the market is allowing near-term liquidation to obscure an emerging use case at precisely the wrong time.

That is the question we now need to answer as investors. Because identifying the invisible AI trade is only the first step. The next step is deciding what to do with it.

You might also like reading: - why the index can be expensive while the opportunity set remains attractive.

A quick note on accountability.

We don’t publish these theses to be right on paper. We publish them to express edge in the real economy. Our Leaderboard shows the exact scorecard since inception, tracking every position, our compounding outperformance against the market, and the triple-digit winners we’ve captured along the way.

Disclaimer

The information provided herein is for general informational purposes only and does not constitute financial advice or a recommendation to buy, sell, or hold any investment. It is not tailored to any specific individual or investor profile. All investments involve risks, and past performance is not indicative of future results. Before making any investment decisions, it is important to consider your own financial situation and risk tolerance. We do not guarantee the accuracy, completeness, or reliability of any information provided, and we disclaim any liability for any loss or damage arising from reliance on the information herein. Readers are advised to consult with an authorized financial intermediary before making any investment decisions.

What about Solana vs Ehereum?