The Index Is Expensive. The Opportunity Set Is Not.

The S&P 500 is heavily concentrated in expensive mega-caps, but the real opportunity is shifting to the high-quality assets the crowd refuses to trust.

In May’s issue of VMF’s Security Selection, we argued that this may be one of the most interesting moments for stock pickers in years.

Not because the index is cheap.

It is not.

The main benchmarks are near record highs. Market concentration remains extreme. The largest AI winners have already been rewarded. And the most obvious conclusion is tempting:

Stocks are expensive.

But that conclusion is too blunt.

The index is expensive.

The opportunity set is not.

That distinction matters because the more capital crowds into the same obvious winners, the more likely it becomes that high-quality businesses outside the spotlight are ignored, misunderstood, or left behind.

That is where security selection begins.

This week, we are publishing two excerpts from May’s issue.

Today’s excerpt explains why an expensive index can still contain mispriced individual businesses, and why market concentration may be creating opportunities rather than eliminating them.

In the next post, we will go one step further and disclose one of our newest stock recommendations: a controversial, cash-rich technology platform sitting directly inside the AI application layer.

But first, the broader setup.

Why the index is expensive...

And why the opportunity set is not

The U.S. market is not cheap.

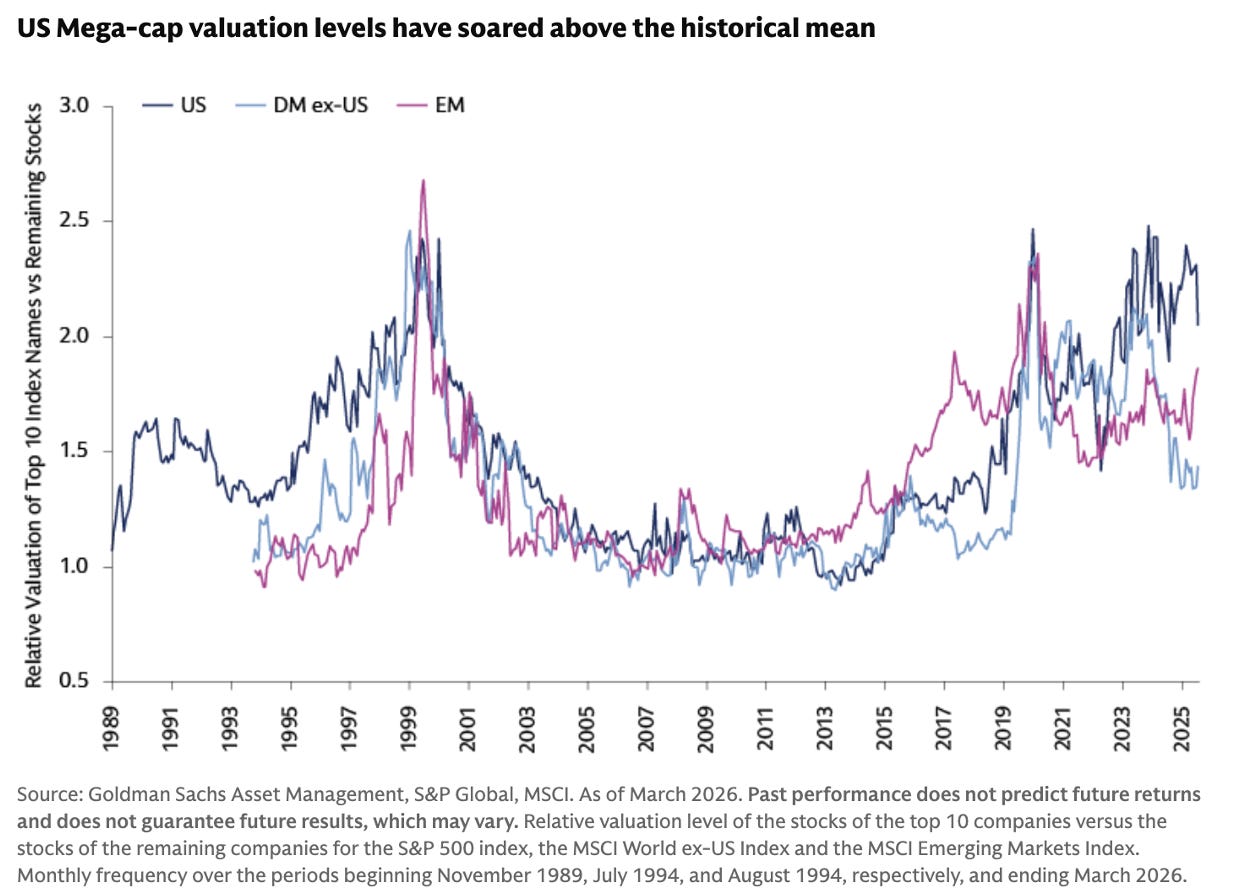

As Goldman Sachs Asset Management shows, the valuation premium of the largest U.S. companies relative to the rest of the market has moved far above its long-term average.

The biggest names are not only large. They are also expensive relative to everything beneath them.

That matters because valuation is not just a number on a spreadsheet. It is a measure of how much future perfection investors are already willing to pay for today. And right now, a great deal of perfection is being priced into a very small group of companies.

This chart compares the valuation of the top 10 companies in each index with the valuation of the remaining companies. A ratio of 1.0x means the largest companies trade at roughly the same valuation as the rest of the market. A ratio above 2.0x means the top 10 stocks trade at more than twice the valuation of the remaining constituents. The message is clear: in the U.S., the largest companies are not only dominating index weight. They are also commanding a much richer valuation than the rest of the market.

This does not mean the winners are bad businesses. Far from it. Many of them are extraordinary. They have dominant platforms, fortress balance sheets, powerful AI exposure, and some of the best economics ever seen in public markets.

But even wonderful businesses can become dangerous investments when the price of consensus gets too high.

That is the first point.

The second point is even more important.

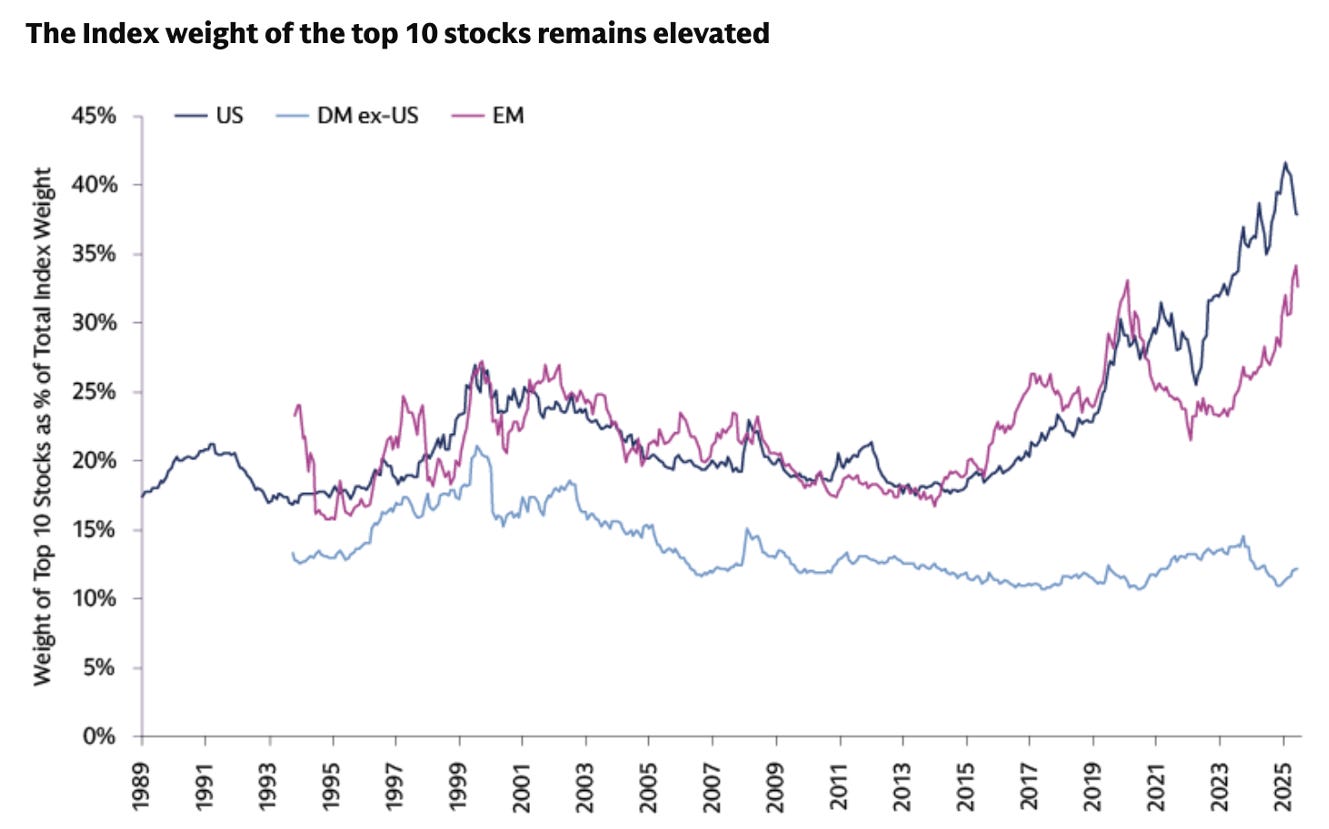

The index is no longer a neutral picture of “the market.” It has become a much narrower bet than many investors realize. As the next chart shows, the top 10 stocks now account for an unusually high share of the U.S. equity market.

This is not merely a valuation issue. It is a concentration issue.

When the top of the market becomes this large, investors start making a dangerous mental shortcut.

They look at the index.

They see high valuations.

They conclude that stocks are expensive.

But the index is not the opportunity set.

The S&P 500 is market-cap weighted. And today, that means it is heavily influenced by a small group of mega-cap winners.

That is why we believe this environment is so interesting for stock pickers.

Because the more the index becomes dominated by the same obvious companies, the more likely it becomes that other high-quality businesses are ignored, misunderstood, or left behind.

In other words, market concentration does not eliminate opportunity... It changes where the opportunity hides.

The opportunity is less likely to be in the most admired businesses already priced for near-perfection. It is more likely to be in the companies that still require explanation. The ones with visible problems. The ones investors distrust. The ones sitting outside the comfort zone of benchmark buyers.

That is where the real work begins.

And this is where the chart below becomes especially useful.

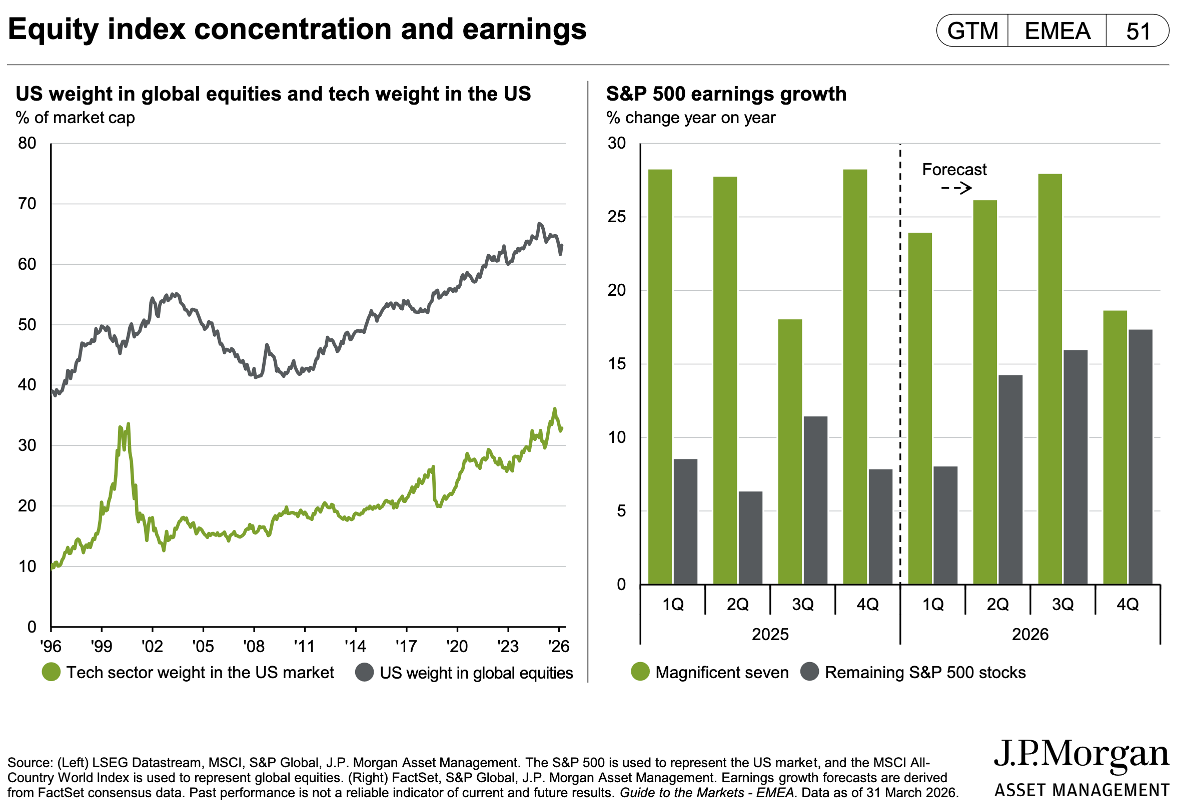

J.P. Morgan’s work shows that the U.S. equity market has become increasingly dominated by technology and by the United States itself within global equities. It also shows that the Magnificent Seven1 have been delivering much stronger earnings growth than the rest of the S&P 500.

So, let’s be clear.

This concentration did not come out of nowhere. The winners have earned a great deal of their leadership. Their earnings growth has been superior. Their business models are exceptional. Their exposure to AI is real.

But this chart does more than explain the past.

It also hints at the next phase.

The earnings-growth gap is expected to narrow.

In fact, by the fourth quarter of 2026, FactSet’s estimates show the Magnificent Seven’s earnings growth slowing materially, while the rest of the S&P 500 is expected to keep accelerating. If those forecasts are even directionally right, the market’s leadership may already be preparing to broaden.

That does not mean the mega-caps will collapse.

It does not mean the AI leaders are finished.

And it certainly does not mean investors should blindly rotate out of them... But it does suggest that the thesis we have been building across VMF Research is now beginning to show up in the numbers.

The first phase of the AI trade rewarded the companies building the infrastructure.

The next phase may reward the businesses that can turn that infrastructure into better economics: higher revenue, wider margins, faster productivity, deeper customer engagement, smarter logistics, cheaper software development, stronger distribution, and superior capital efficiency.

You might also like reading:

And remember: the chart only shows the S&P 500.

Our opportunity set is much broader.

It includes international markets. It includes emerging markets. It includes individual companies outside the benchmark comfort zone. It includes businesses investors still distrust because of geography, regulation, complexity, size or recent disappointment.

That is why this is becoming a stock picker’s market.

Not because the index is cheap.

It is not.

Not because the macro backdrop is simple.

It is not.

And not because every beaten-down stock is suddenly a bargain.

Most are not.

It is a stock picker’s market because the gap between what is loved and what is ignored remains extreme... while the earnings-growth gap that justified some of that concentration may already be starting to close.

When that happens, careful security selection becomes more valuable, not less.

That is why Bill Ackman’s recent comments caught our attention.

In late March, Ackman argued that this is one of the best times in a long time to buy quality stocks. He urged investors to look past macro fears and focus on deeply discounted opportunities, even as markets were still wrestling with sticky inflation, rising energy prices, and geopolitical stress.

Coming from Ackman, that is not generic bullishness. His entire investment career has been built around a very specific discipline: concentrated ownership of durable, cash-generative businesses when the market is temporarily unwilling to value them properly.

That is also the logic behind Pershing Square USA Ltd2 ( PSUS 0.00%↑)

PSUS is Ackman’s new U.S.-listed closed-end fund. In broad terms, it gives American investors access to the same style of concentrated, quality-focused investing that sits behind Pershing Square Holdings ($PSHD.L), the London-listed vehicle we already own in our Model Portfolios.

But the structure was more ambitious than a simple fund launch.

The transaction also included a second layer: Pershing Square Inc. (PS), the management company itself. As part of the offering, investors who bought PSUS received shares in Pershing Square Inc. at no additional cost.

Beat the old playbook. Get institutional-grade research delivered to your inbox.

In other words, the asset-management company was used as a sweetener for the fund IPO. Buyers were not only getting access to Ackman’s concentrated investment portfolio through PSUS... they were also receiving a direct interest in the economics of the Pershing Square platform itself. That made the listing a broader attempt to bring the entire Pershing Square ecosystem to public investors: the fund, the permanent-capital structure, and the management company behind it.

On paper, it was a major event.

PSUS raised $5 billion, making it one of the largest closed-end fund IPOs in history. Ackman and his employees also committed roughly $500 million to the offering, a meaningful signal of alignment. But the market reception was underwhelming. The fund traded sharply below its IPO price on the first day, and Ackman later blamed part of the weakness on retail investors who had overcommitted to the deal.

We see a useful lesson in that contrast.

Ackman is telling investors that high-quality stocks are unusually attractive. At the same time, his own new vehicle for concentrated quality investing struggled to generate the kind of enthusiasm once imagined.

That gap is revealing.

Investors like the idea of quality. But in practice, many still prefer the familiar comfort of index exposure, mega-cap leadership, and the obvious AI winners that have already worked.

In other words, the market is still rewarding what is easy to own.

Our job in VMF’s Security Selection is different.

We are not trying to time the exact moment when market leadership broadens. That is a more natural discussion for Alpha Tier. Here, we care about something narrower and more practical: individual securities where the risk/reward already looks compelling before the crowd is willing to agree.

And that brings us to this month’s company.

The broader market is near all-time highs. By several measures, it looks historically expensive. But beneath that surface, we continue to find businesses where quality, growth and optionality do not line up with the prevailing pessimism.

This one sits directly inside the application layer of the AI trade we discussed in May’s Strategic Asset Allocation issue.

It is not part of the most obvious infrastructure story.

It is not in the geography investors feel most comfortable owning.

It is in China, where sentiment remains depressed, valuations remain compressed, and many investors still struggle to separate country-level discomfort from company-level opportunity.

That is what makes the setup interesting.

We are moving from the index to the stock.

From infrastructure to application.

From crowded consensus to a business many investors still refuse to trust.

Let’s turn to the company itself.

Tomorrow, we will reveal the name right here.

A quick note on accountability.

We don’t publish these theses to be right on paper. We publish them to express edge in the real economy. Our Leaderboard shows the exact scorecard since inception, tracking every position, our compounding outperformance against the market, and the triple-digit winners we’ve captured along the way.

The Magnificent Seven earned their market leadership by delivering much stronger earnings growth than the rest of the S&P 500. But the key point in this chart is forward-looking: according to FactSet estimates shown by J.P. Morgan, that earnings-growth gap is expected to narrow materially into late 2026. By the fourth quarter of 2026, Magnificent Seven earnings growth is expected to slow, while earnings growth for the remaining S&P 500 companies is expected to accelerate. That does not mean the AI leaders are finished. It means the market may be entering a broader phase, where the next opportunities are less about owning the obvious winners and more about identifying the companies whose earnings power is still underappreciated.

Pershing Square Inc. is the asset management company behind Bill Ackman’s investment vehicles, including Pershing Square Holdings and Pershing Square USA. That makes it different from the funds themselves. A fund owns a portfolio of investments. The asset manager earns economics from managing those portfolios, typically through management fees, performance fees, and the value of permanent or long-duration capital. That distinction is important. Pershing Square Inc. gives investors exposure not only to Ackman’s stock-picking ability, but also to the business model behind that stock-picking franchise. We will dissect that opportunity in a future issue.