PDD: China Price, Temu Optionality.

When the world’s most uncomfortable market gives you an asset-light intelligence engine at 5x free cash flow.

For the past few months, we have been approaching China from the top down.

We have studied the macro scars, the property downturn, the policy trauma, the geopolitical discount, and the possibility that China’s real AI opportunity may not sit only at the frontier-model layer, but also in the application layer, where intelligence gets embedded into industry, robotics, commerce, payments, logistics, advertising, consumer behaviour, and daily economic life.

That work led us to a broad conclusion: China remains one of the most uncomfortable markets in the world to own, but that discomfort is now part of the price.

This post is where we move from the country to the company.

In May’s issue of VMF’s Security Selection, we identified what we believe is one of the more interesting stock-level expressions of that China application-layer thesis: PDD Holdings, a controversial, cash-rich marketplace platform with a powerful domestic profit engine and a global option through Temu.

The market is not stupid. PDD is cheap for reasons that deserve to be taken seriously.

China risk is real.

The VIE structure matters.

Temu faces increasing regulatory scrutiny.

Disclosure is imperfect.

Competition is brutal.

And global investors have good reasons to demand a discount.

But investing is rarely about finding situations without problems. It is about finding situations where the problems are known, the price is depressed, and the underlying value may be much greater than the market is willing to recognize.

That is the tension we see in PDD.

In this excerpt, we are disclosing the actual recommendation from May’s issue: the target weight, the full thesis, the bear case, the valuation work, the role of Temu, the balance-sheet analysis, and why we believe the risk/reward was compelling enough to add PDD to our Value Model Portfolio.

This is a longer post than usual because that is what the opportunity requires. When a stock is controversial, cheap, and sitting at the intersection of China, AI, e-commerce, and global regulation, the work cannot be reduced to a slogan.

Good reading.

The company is PDD Holdings PDD 0.00%↑ .

Not NVIDIA.

Not a South Korean memory champion.

Not a uranium miner.

Not a data-center landlord.

Not one of the obvious names investors now reflexively associate with artificial intelligence. And that is precisely why it belongs in this issue.

The first phase of the AI trade was easy to understand. More AI required more compute. More compute required more chips, more memory, more power, and more data-center infrastructure. The market could see the earnings bridge.

So it paid for it.

The next phase is less obvious. It is not only about building the AI machine. It is about using that machine to improve real economic activity:

Commerce.

Search.

Discovery.

Pricing.

Advertising.

Logistics.

Merchant tools.

Consumer behavior.

Transaction flows.

That is where AI stops being a demo and becomes monetization.

And that is where PDD sits.

The market still sees PDD mostly as a Chinese e-commerce company, with all the usual baggage: weak consumer confidence, geopolitical tension, regulatory uncertainty, and growing scrutiny around Temu. That framing is understandable.

But it is incomplete.

PDD is not entirely new to VMF Research.

In VMF’s Strategic Asset Allocation, we recently increased our position in KWEB, the KraneShares CSI China Internet ETF. PDD is one of KWEB’s largest holdings, at roughly 8.5%. That made sense for Tier One. KWEB gives us a diversified way to own China’s internet platforms without pretending we can know, in advance, which company will capture the largest share of the application-layer opportunity.

But VMF’s Security Selection has a different job. Here, we are not building a broad geographical or sector tilt. We are asking a more specific question:

Is there one company inside that basket where the risk/reward is strong enough to own directly?

That is the question we want to answer this month.

PDD also appears inside another VMF holding: Scottish Mortgage Investment Trust.

That is a different kind of signal.

We own Scottish Mortgage in VMF’s Security Selection and Alpha Tier because it remains one of the market’s most interesting vehicles for long-duration disruptive growth. Its portfolio is filled with companies trying to reshape large markets: SpaceX, TSMC, NVIDIA, ByteDance, Amazon, Stripe, Revolut, MercadoLibre, ASML, Anthropic and others.

And there, too, we find PDD.

You might also like reading

As of Scottish Mortgage’s March 2026 portfolio valuation, PDD represented 2.0% of the trust. Scottish Mortgage’s own description of the company is also revealing: it calls PDD an innovative e-commerce platform built around value-for-money merchandise and interactive shopping experiences.

That is the first interesting point.

PDD is not only a China internet holding inside KWEB. It is also held by a manager whose mandate is to find exceptional growth companies capable of shaping the future economy. Scottish Mortgage is not buying PDD because it needs to hug an index. It is buying PDD because it sees something more durable than the market currently wants to recognize.

But the story becomes even more interesting when we look at who else owns it, because PDD is not only attracting growth investors. It is also attracting some of the most respected value-oriented investors with deep knowledge of China.

Li Lu’s Himalaya Capital is one example. Li Lu1 is one of the most respected investors in the Buffett-Munger tradition, and Charlie Munger famously entrusted a meaningful portion of his own family capital to him. His disclosed U.S.-listed portfolio is highly concentrated, and as of the latest 13F data, PDD represented 14.64% of Himalaya Capital’s holdings.

Duan Yongping2 is another.

Duan is one of China’s most successful entrepreneurs and investors, with a reputation built over decades through businesses, capital allocation, and long-term ownership. Through H&H International Investment, his disclosed U.S. portfolio also includes a major PDD position. As of the latest filing, PDD represented 7.48% of the portfolio, making it one of his five largest disclosed holdings.

So, PDD sits in a very unusual place.

It is innovative enough to remain inside Scottish Mortgage.

It is cheap enough to attract world-class value investors.

And it is controversial enough for the broader market to still keep its distance.

That is the combination we find interesting.

We are not buying PDD because other investors own it.

That would not be research. It would be imitation. But when a company appeals simultaneously to long-duration growth investors and deeply selective value investors, we pay attention.

Especially when the valuation looks like this.

PDD currently trades at roughly 10x trailing earnings, 8x forward earnings, just over 2x sales, and less than 9x free cash flow.

On an enterprise-value basis, the valuation becomes even more striking, with the stock trading around 6x EBITDA and roughly 5x free cash flow.

And that is before fully appreciating the strength of the balance sheet.

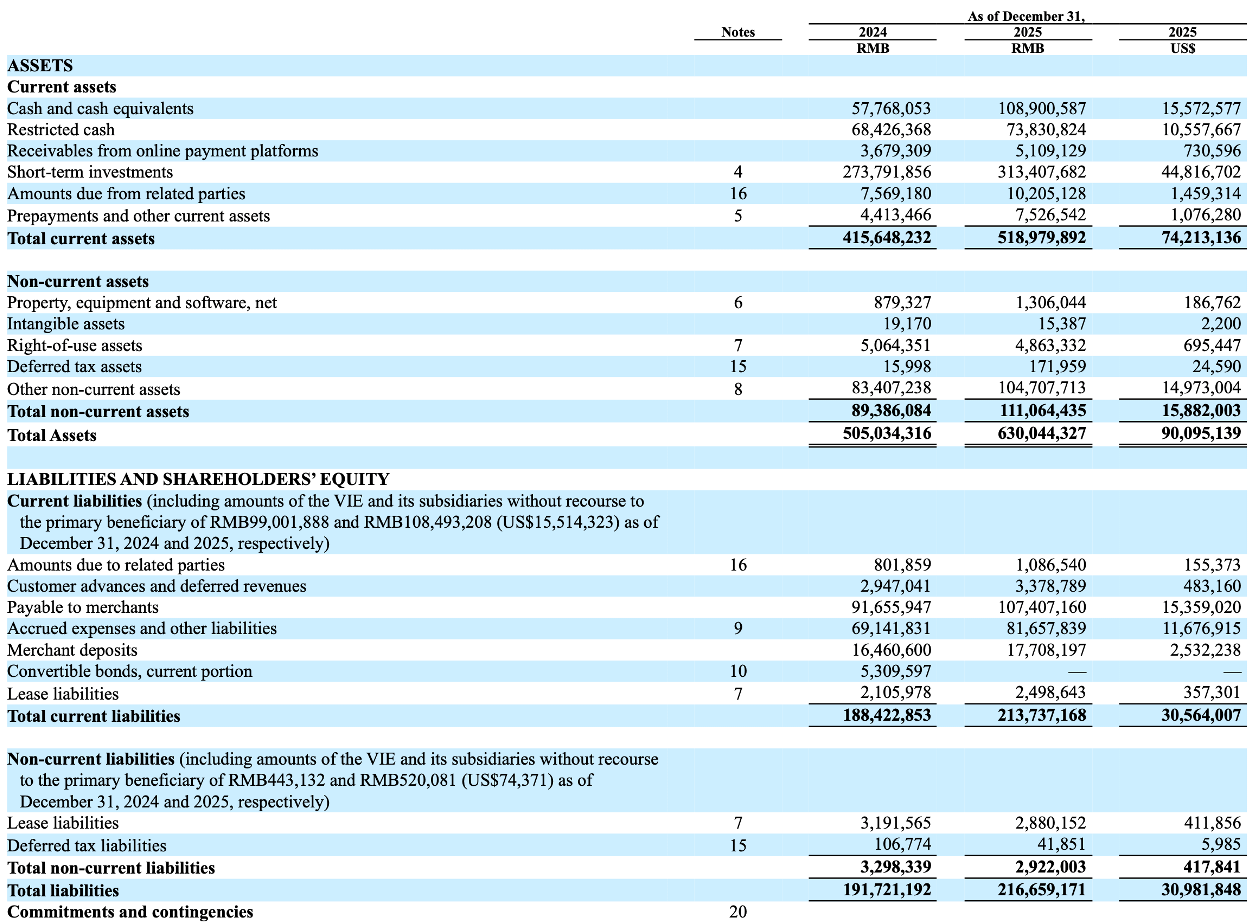

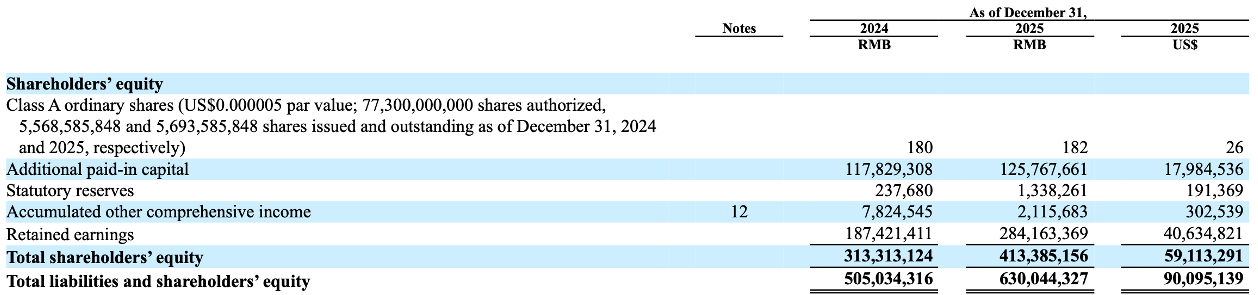

At the end of 2025, PDD held RMB422.3 billion in cash, cash equivalents, and short term investments, equivalent to roughly $60.4 billion. If we subtract debt-like obligations, mainly lease liabilities, net cash still sits close to $60 billion.

A very large part of PDD’s market value ($136.3 billion) is backed by cash and liquid investments.

That is not how the market usually values a dominant, profitable, asset-light technology platform with exposure to one of the largest consumer markets in the world.

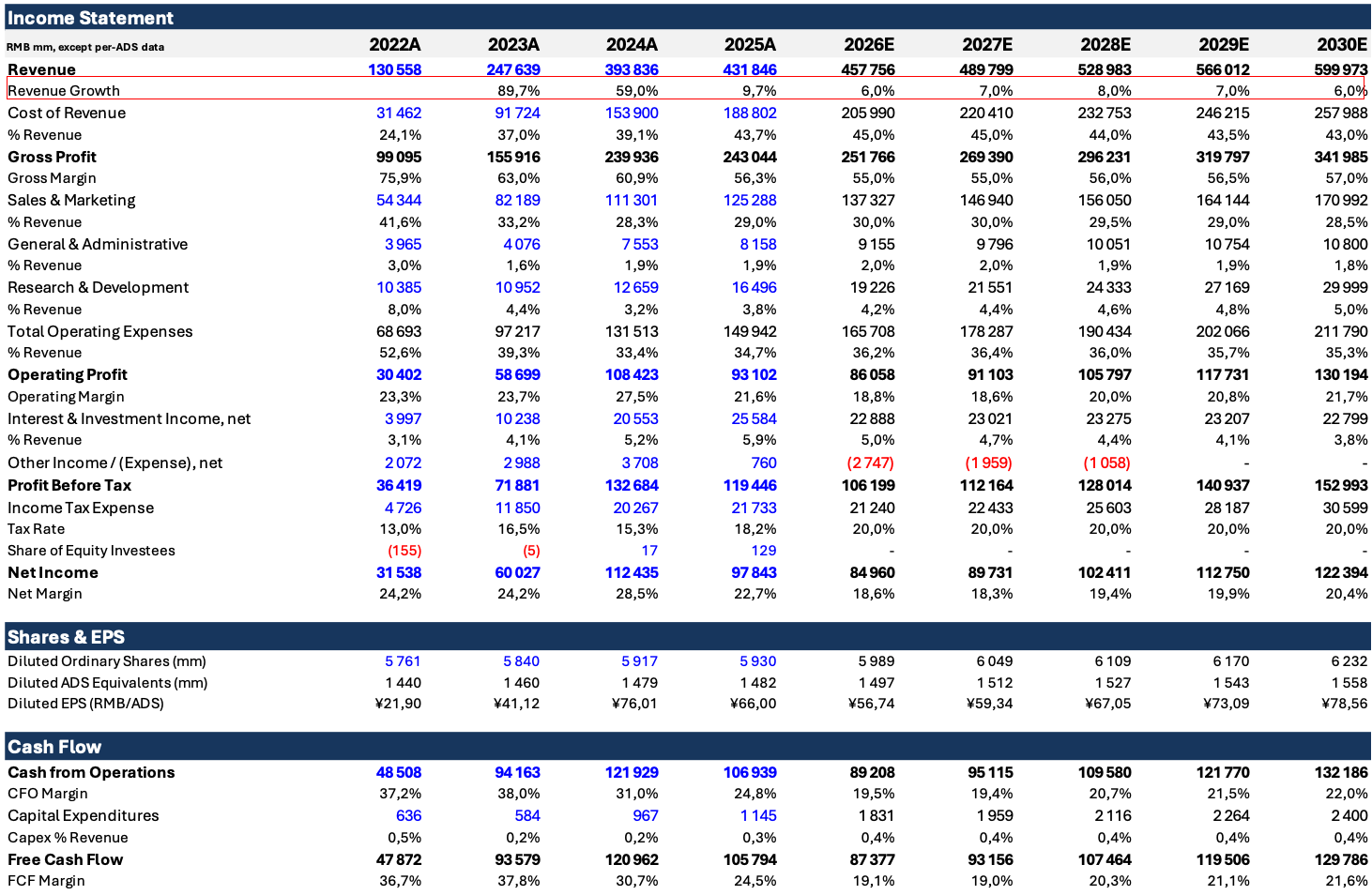

And the operating scale is just as important. In 2025, PDD generated RMB431.8 billion in revenue, or roughly $61.8 billion, representing 10% year-over-year growth, despite a year in which investors remained deeply skeptical of Chinese equities, consumer confidence, and Temu’s international expansion.

That leaves us with a paradox.

PDD is large.

It is profitable.

It is cash-rich.

It sits directly in the application layer of the AI economy.

It is held by sophisticated growth investors.

It is held by highly respected value investors.

And yet the market values it like a business carrying a very large warning label. The obvious question is:

Why?

Let’s begin where we should always begin when a stock looks this cheap... with the bear case.

The first layer is the country.

China remains one of the most difficult markets in the world for foreign investors to underwrite.

We do not need to repeat the full discussion from this month’s VMF’s Strategic Asset Allocation, but the concerns are real: weak consumer confidence, the property downturn, regulatory scars, geopolitical friction, governance concerns, and the persistent fear that Chinese companies may create value without allowing outside shareholders to capture enough of it.

From VMF’s Strategic Asset Allocation:

Then there is the VIE structure.

As we explained in detail when we recommended Alibaba BABA 0.00%↑ back in July 2024, many Chinese internet companies listed offshore do not give foreign investors direct ownership of the operating business inside China. PDD follows that same broad architecture.

Investors in PDD’s ADSs own shares in an offshore Cayman Islands holding company, not direct equity in the Chinese VIEs and their subsidiaries. Their economic exposure to the operating business is created through contractual arrangements rather than ordinary share ownership in the underlying operating assets.

That structure has worked for decades, but it is not the same thing as owning a conventional U.S. or European equity. It adds a layer of legal, regulatory, and political uncertainty that foreign investors are right to discount.

So, the China discount is not random.

It exists for a reason.

But in VMF’s Security Selection, we cannot stop at the country label. Our job is to ask whether the country risk has overwhelmed the company-specific reality.

And with PDD, the company-specific concerns are also serious.

The first is Temu.

Temu has been one of the most aggressive e-commerce expansions of the past several years. It transformed PDD from a mostly domestic Chinese e-commerce story into a global discount-commerce force almost overnight.

That created enormous optionality, but also a much harder underwriting problem.

International expansion is expensive.

Customer acquisition is expensive.

Logistics are complex.

Regulatory scrutiny is increasing.

And the model’s early advantage depended partly on cross-border shipping economics that governments are now challenging...

The United States has already moved against the de minimis framework that helped low-value direct-from-China e-commerce packages enter the country at favorable economics.

Reuters reported that Temu’s daily U.S. users fell sharply after the end of that loophole, a reminder of how sensitive parts of the model may be to policy changes.

Europe is moving in the same direction. EU finance ministers agreed to accelerate customs duties on low-value parcels, a change expected to hit Chinese online retailers such as Shein and Temu.

More recently, the EU also agreed to overhaul its customs system, with tougher enforcement and potential fines for platforms selling illegal or unsafe products into the bloc.

That is a real risk.

Temu may need more local warehousing, more compliance spending, more merchant support, more customer-service infrastructure, and more regulatory adaptation than early bulls expected. The international business may still be valuable, but it is unlikely to be frictionless.

The second concern is profitability.

PDD is highly profitable at the group level, but investors still struggle to understand how durable those profits really are.

How much comes from the core China platform?

How much is being reinvested into Temu?

How much margin pressure should we expect as the company supports merchants, localizes operations, and defends its international model?

That uncertainty is part of the discount. A low multiple is less useful if the “E” in the P/E ratio becomes difficult to trust.

The third risk is competition.

In China, PDD competes with Alibaba, JD.com, Douyin, Kuaishou, and other platforms fighting for consumers, merchants, advertising budgets, and transaction volume. The market is enormous, but it is also ruthless.

Promotional intensity can rise. Merchant subsidies can increase. Delivery expectations can tighten. Consumer weakness can push platforms into more aggressive price competition.

Internationally, Temu competes not only with Shein, Amazon, AliExpress, and local retailers, but also with governments, regulators, and increasingly hostile political narratives around Chinese imports.

Beat the old playbook.

Get institutional-grade research delivered to your inbox.

This is not a clean battlefield.

The fourth risk is legal and regulatory scrutiny.

Temu’s rise has attracted attention everywhere. Reuters recently reported that Shein accused Temu of “industrial scale” copyright infringement in a U.K. legal battle, while Temu denied the allegations and accused Shein of trying to suppress competition.

The details of that dispute are less important than the broader message: as Temu scales globally, it will be scrutinized like a major platform business.

That means more legal costs.

More compliance costs.

More product-safety obligations.

More platform policing.

More headline risk.

The fifth risk is disclosure and capital allocation.

PDD does not communicate like a Western blue-chip compounder. It provides less granular segment disclosure than many investors would like, especially around Temu. It does not yet return capital in the way global shareholders might prefer, despite its enormous cash pile. And because the company is exposed to China, investors apply an additional discount to almost everything on the balance sheet.

Again, this is not irrational.

When a company holds tens of billions of dollars in cash but shareholders are unsure how much of that cash will ultimately be returned or reinvested well, the market will not value it like cash in a U.S. large-cap compounder.

So, let’s be clear.

The bear case is real.

That is why PDD trades where it does.

But the existence of risk does not automatically mean the absence of opportunity.

In fact, the best investments often begin where the market has identified real risks, then priced the business as if those risks are the only facts that matter.

Which brings us to the other side of the question.

What exactly is the market missing?

And above all, what are elite growth and value investors seeing that the broader market still refuses to recognize?

In our view, the answer begins with a simple distinction:

PDD is not a retailer.

Not really...

A retailer buys inventory, marks it up, manages stores or warehouses, carries working-capital risk, and hopes the customer shows up. That is not the right mental model here.

PDD is closer to a marketplace intelligence engine.

Its real asset is not inventory. It is the system sitting between consumers, merchants, products, prices, advertising, demand signals, logistics partners, and transaction flows. The company’s own description points in that direction.

Pinduoduo pioneered a team-purchase model, uses social sharing to aggregate demand, connects merchants and buyers, and helps merchants offer more competitive prices and customized products.

Temu follows the same broad operational logic internationally, bringing together buyers, merchants, manufacturers, brands, logistics vendors, and fulfillment partners.

That is why the application-layer framing matters so much. PDD does not need to build the world’s best frontier model to benefit from AI. It only needs to keep deploying intelligence into commerce more effectively than its competitors.

Better product discovery.

Better pricing.

Better ad targeting.

Better merchant ranking.

Better demand forecasting.

Better logistics coordination.

Better fraud detection.

Better software development.

Better matching between what consumers want and what merchants can supply.

That is not AI as a press release.

That is AI as operating leverage.

And this is where we think the market is being too narrow. It sees a controversial Chinese discount-commerce company. We see a cash-rich, asset-light platform that has already proven it can change consumer behavior in China, and that now owns a global option through Temu.

The core of the thesis, however, is not Temu alone.

That point is important.

Temu is the upside option. It is also where much of the controversy lives. But our base case does not require it to become the “next Amazon,” or even close. We do not need every regulatory, tariff, logistics, and profitability question around the international business to resolve perfectly.

The domestic Chinese operation already gives us enough to work with.

That is the foundation.3

PDD has a scaled marketplace in one of the largest consumer markets in the world. It generates substantial free cash flow. It has a fortress balance sheet. And as we noted earlier, even after a more difficult year, revenue still grew 10% in 2025 to RMB431.8 billion, or roughly $61.8 billion. We also highlighted the balance-sheet strength: at year-end, the company held RMB422.3 billion in cash, cash equivalents, and short-term investments, equivalent to roughly $60.4 billion.

We should not value that cash the same way we would value cash sitting inside a U.S. blue-chip.

That deserves to be said clearly.

There is less visibility around how it will be reinvested, whether it will eventually be returned to shareholders, and how much of it should be discounted because of China, the VIE structure, currency controls, and capital-allocation uncertainty.

So, we do not give it full credit.

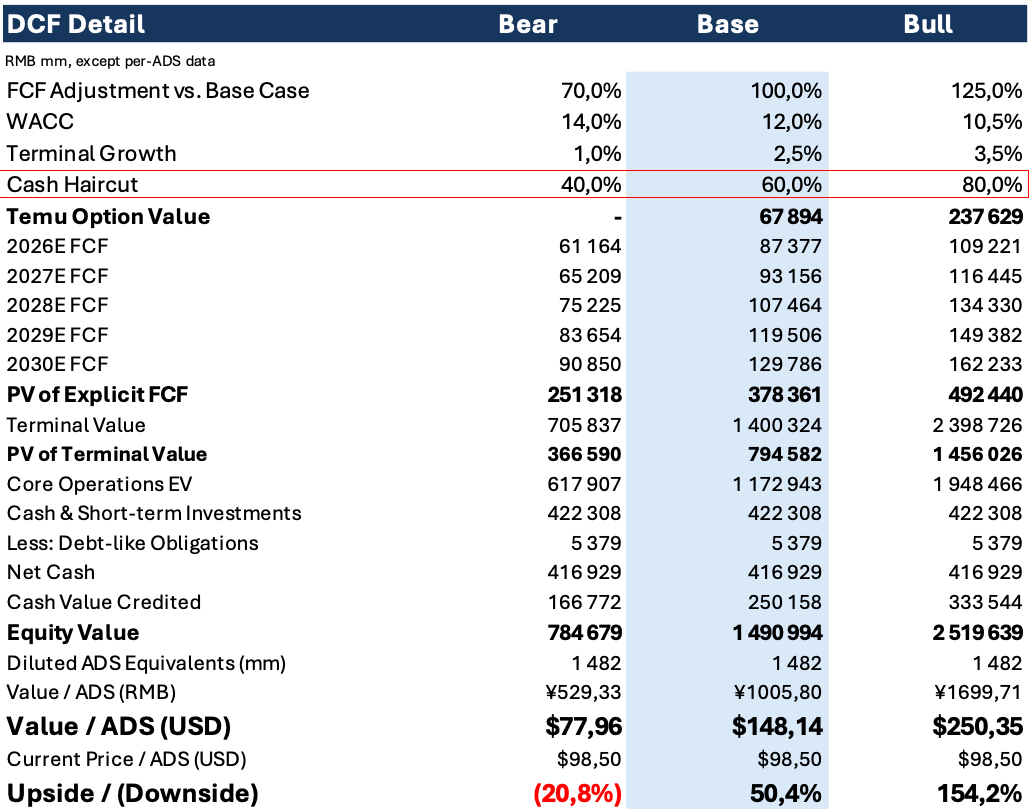

In our valuation model, we apply a significant haircut to the cash balance. Even then, it remains a major source of margin of safety.

That is the beauty of the setup...

As the valuation work on these pages shows, the investment case does not depend on a perfect story or heroic assumptions.

We are paying a discounted price for a strong domestic profit engine, receiving only partial credit for a very large cash balance, and getting Temu as a valuable option rather than as the entire thesis.

Our base case is intentionally conservative.

We assume revenue growth in the mid-single to high-single-digit range over the next five years, far below the explosive growth PDD delivered earlier in its life. We also assume only gradual margin improvement, despite the company’s asset-light structure and the operating leverage that could emerge if Temu’s losses moderate or the domestic business continues to scale efficiently.

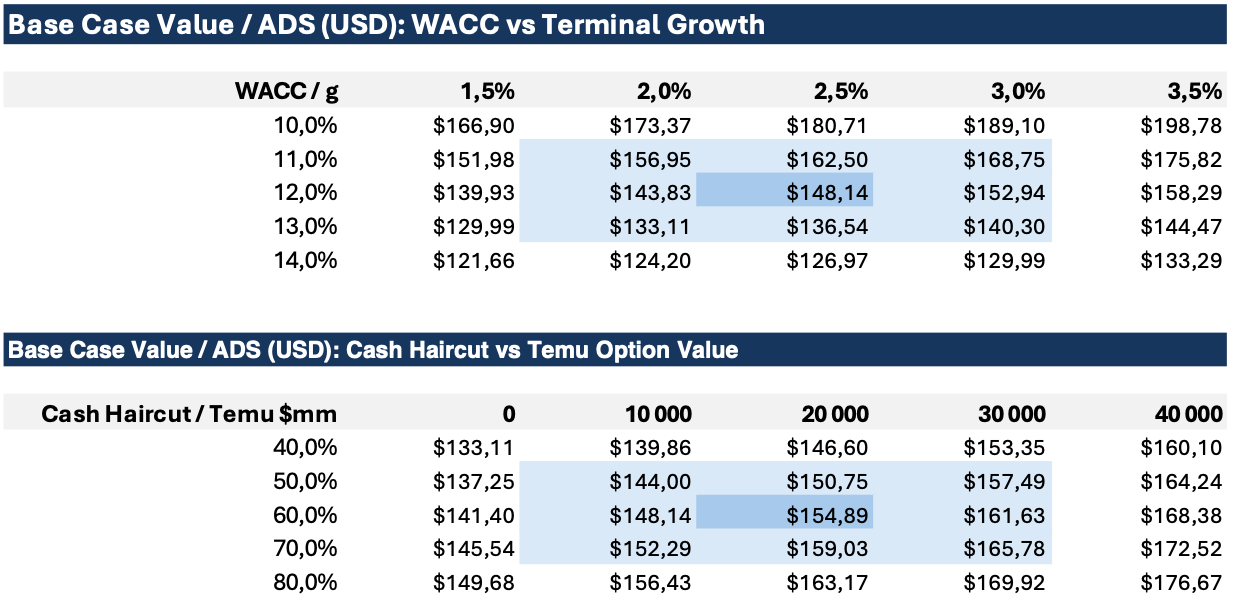

We also use a demanding cost of capital. Our base case applies a 12% WACC, which is much higher than what we would use for a comparable U.S. platform business.

That is deliberate. PDD deserves a China discount. It deserves a governance discount. It deserves a Temu uncertainty discount. We are not trying to make the valuation work by pretending those risks do not exist.

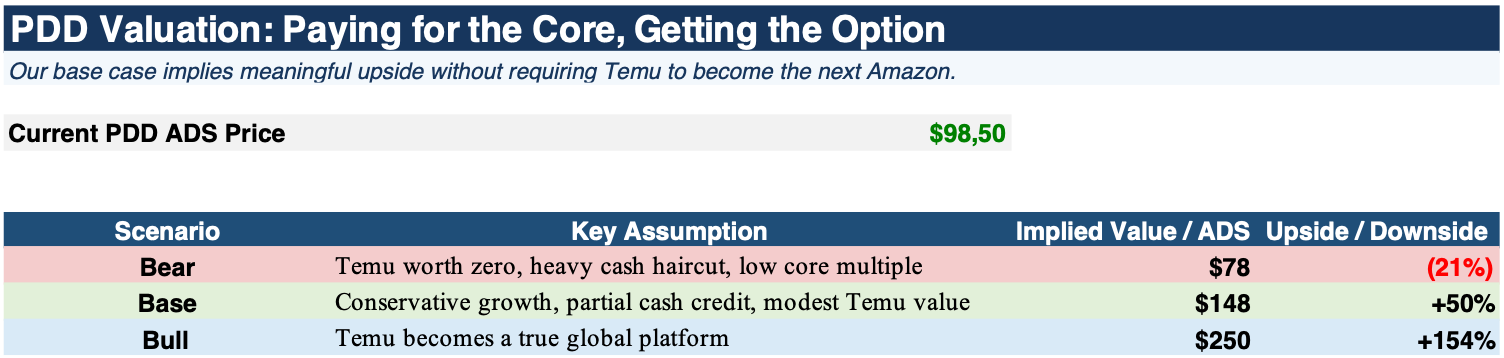

Even with those assumptions, our base case reaches roughly $148 per ADS, implying just over 50% upside from our reference price of $98.50.

That is the central point. The stock does not need everything to go right...

It just needs the market to stop treating every risk as if it will resolve in the worst possible direction.

Our bear case is also useful. There, we give Temu no value, haircut the cash muchmore aggressively, and penalize the free-cash-flow forecast. Under that scenario,

we arrive at roughly $78 per ADS, or around 20% downside from today’s price.

That is not trivial.

But it is acceptable for a 2% position when the base and bull cases offer substantially better upside. In the bull case, the numbers become much more interesting. There, the domestic business compounds better, the market gives more credit to the cash balance, and Temu proves it is more than a temporary play on tax, shipping, and regulatory “arbitrage.” It becomes a durable global commerce platform.

Under that scenario, our valuation reaches roughly $250 per ADS, or more than 150% upside.

Beat the old playbook.

Get institutional-grade research delivered to your inbox.

But again, that is not our base case.

The bull case requires Temu to matter.

The base case does not require Temu to become a global winner. It only assumes that Temu has some option value, while the domestic platform and the balance sheet carry most of the valuation.

That is exactly how we want to underwrite this kind of position.

Core business first.

Cash with a haircut.

Temu as an option.

No fantasy.

No blind faith.

No assumption that China risk suddenly disappears.

The sensitivity tables reinforce the same conclusion.

Even when we flex the key variables (discount rate, terminal growth, cash haircut, and Temu option value) the valuation work still points to a wide range of outcomes above today’s share price.

That is important because it tells us the thesis is not dependent on one fragile assumption. The stock does not need a perfect WACC. It does not need full credit for the cash. And it does not need Temu to be valued like a proven global winner.

Across reasonable scenarios, the current price appears to discount a great deal of failure already.

What the market may be missing is that PDD does not need to become a clean, Western-style compounder to be mispriced. It only needs to remain a highly profitable, cash-generative, asset-light marketplace while proving that Temu is not a permanent value destroyer.

That is a much lower bar than the market seems to be setting...

And it explains why sophisticated investors from very different schools can end up in the same place.

A growth investor can look at PDD and see a platform with enormous application layer optionality.

A value investor can look at PDD and see a cheap, cash-rich marketplace with a strong domestic profit engine.

We look at it and see both.

That does not make the investment easy.

But it does make it interesting.

And at this price, it makes it investable.

You might also like reading: - why the index can be expensive while the opportunity set remains attractive.

A quick note on accountability.

We don’t publish these theses to be right on paper. We publish them to express edge in the real economy. Our Leaderboard shows the exact scorecard since inception, tracking every position, our compounding outperformance against the market, and the triple-digit winners we’ve captured along the way.

Disclaimer

The information provided herein is for general informational purposes only and does not constitute financial advice or a recommendation to buy, sell, or hold any investment. It is not tailored to any specific individual or investor profile. All investments involve risks, and past performance is not indicative of future results. Before making any investment decisions, it is important to consider your own financial situation and risk tolerance. We do not guarantee the accuracy, completeness, or reliability of any information provided, and we disclaim any liability for any loss or damage arising from reliance on the information herein. Readers are advised to consult with an authorized financial intermediary before making any investment decisions.

Li Lu’s investment philosophy is built around a simple but demanding idea: buy a small number of exceptional businesses only when the margin of safety is large enough. His approach is not based on frequent trading or broad diversification. Himalaya Capital is known for running a concentrated portfolio, which means each major position has to carry real conviction. That is why his presence in PDD is interesting. It suggests the stock may not merely be “cheap” on screen. It may offer the kind of asymmetric setup value investors look for: a strong business, a large discount, and enough uncertainty to keep most investors away

Duan Yongping is one of China’s most successful entrepreneurs and investors. He founded BBK Electronics and is closely associated with the business ecosystem behind consumer-electronics brands such as Oppo and Vivo. Over time, he also became known as a disciplined, long-term value investor, often compared with Warren Buffett in Chinese investment circles. His relevance to PDD is unusually direct. Duan was an early investor and mentor figure to Colin Huang, PDD’s founder, and his disclosed U.S. portfolio has included a meaningful PDD position alongside companies such as Apple, Berkshire Hathaway, Alphabet, Alibaba, and Microsoft.

In the Financial Model, the figures in blue come directly from PDD’s annual reports. Everything from 2026 onward represents our own estimates. Those estimates are deliberately conservative. We are not assuming a return to PDD’s historical hypergrowth. We are not assuming aggressive margin expansion. And we are not giving full credit to the company’s cash balance. Most importantly, we are not building the base case around what Temu could become. Temu may prove to be a highly valuable global platform, but visibility is still limited. That is why we treat it as an option rather than the foundation of the valuation. The point is simple: if the domestic business, a discounted cash balance, and modest assumptions already support meaningful upside, then Temu becomes additional optionality rather than something we need to believe in blindly.

Very comprehensive. Not my expertise, but thank you.

$PDD got so cheap that in 5-years the stock would be trading at 1x cash. Insanely cheap and if mgmt wakes up to buybacks this stock will really start to move and fast.