After Napster, Before AI

From disrupted record labels to dominant global royalty machines.

In my previous article, I shared “The Privileged Position,” the opening section of April’s issue of VMF’s Security Selection.

That section laid out the framework: why we admire the royalty model so much, and why we keep hunting for it in places most investors are not trained to look.

This next excerpt picks up exactly where that one left off. Because once you accept that music can be a royalty asset, the question is no longer theoretical.

It becomes investable:

What kind of asset are we really dealing with here?

That is where “After Napster, Before AI” comes in.

It sits at the center of the issue, right after the framework and right before the part that matters most to paying subscribers: the actual recommendation, the full investment thesis, and the valuation work that turns an interesting idea into a position.

And that sequence matters.

Because good investing is not about falling in love with a clever narrative. It is about moving, step by step, from the model... to the asset... to the cash flows... to the mispricing.

In this section, we do exactly that.

We take the old bear case against music, the one born in the Napster era, and ask whether investors are still looking at this business through a lens that is now badly out of date. Then we push one step further and ask what happens when the current technological disruption wave, AI, collides with a royalty stream that may be far more resilient, and far more adaptable, than the market appreciates.

That is the work you are about to read.

The actionable conclusion remains where it belongs.

But the framework, and the logic that leads to it, begin here.

Here is “After Napster, Before AI.”

At first glance, music does not look like the kind of asset conservative investors are supposed to admire.

It is intangible. It cannot be touched, stored, or inventoried in the way copper, oil, or gold can. It does not sit behind a fence. It does not require a reserve report. And because it lives so close to culture, many investors instinctively file it away in the mental category reserved for fashion, celebrity, taste, and unpredictability.

That is a mistake.

Because once you strip away the surface noise, music has many of the traits that make for a remarkable royalty asset. It is consumed repeatedly. It crosses borders

effortlessly. It travels through new technologies rather than being confined by them. And, unlike a mine or a well, a great song does not deplete when it is used. It can be replayed, re-licensed, re-packaged, re-discovered, and re-monetized for decades.

The asset is intangible. The cash flows do not have to be.

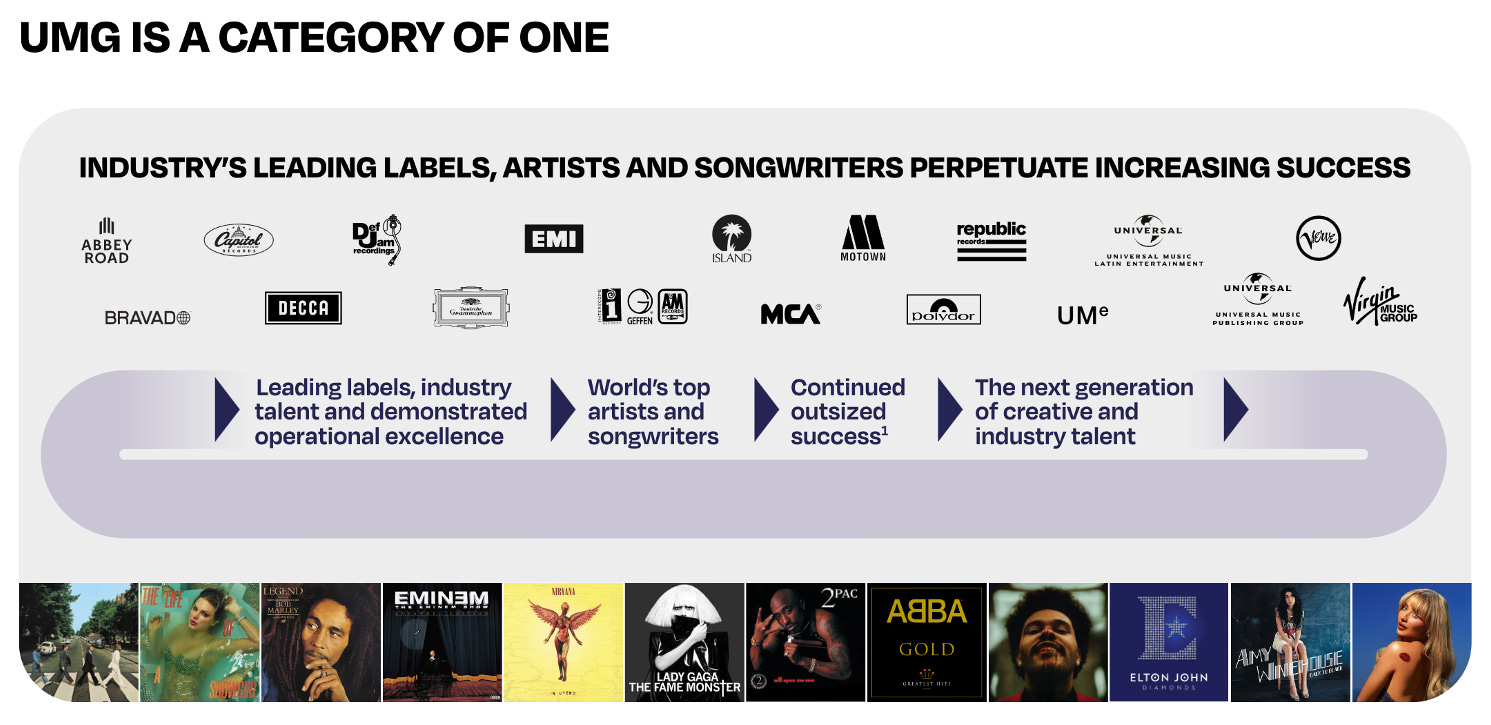

And that is precisely why we have been studying Universal Music Group ($UMG.AS ) so closely. At bottom, UMG is not merely a record label. It is a global rights platform sitting on top of one of the most productive catalogs in the cultural economy.

But that is easier to say now than it was twenty-five years ago.

Because there was a period when the entire industry looked broken...

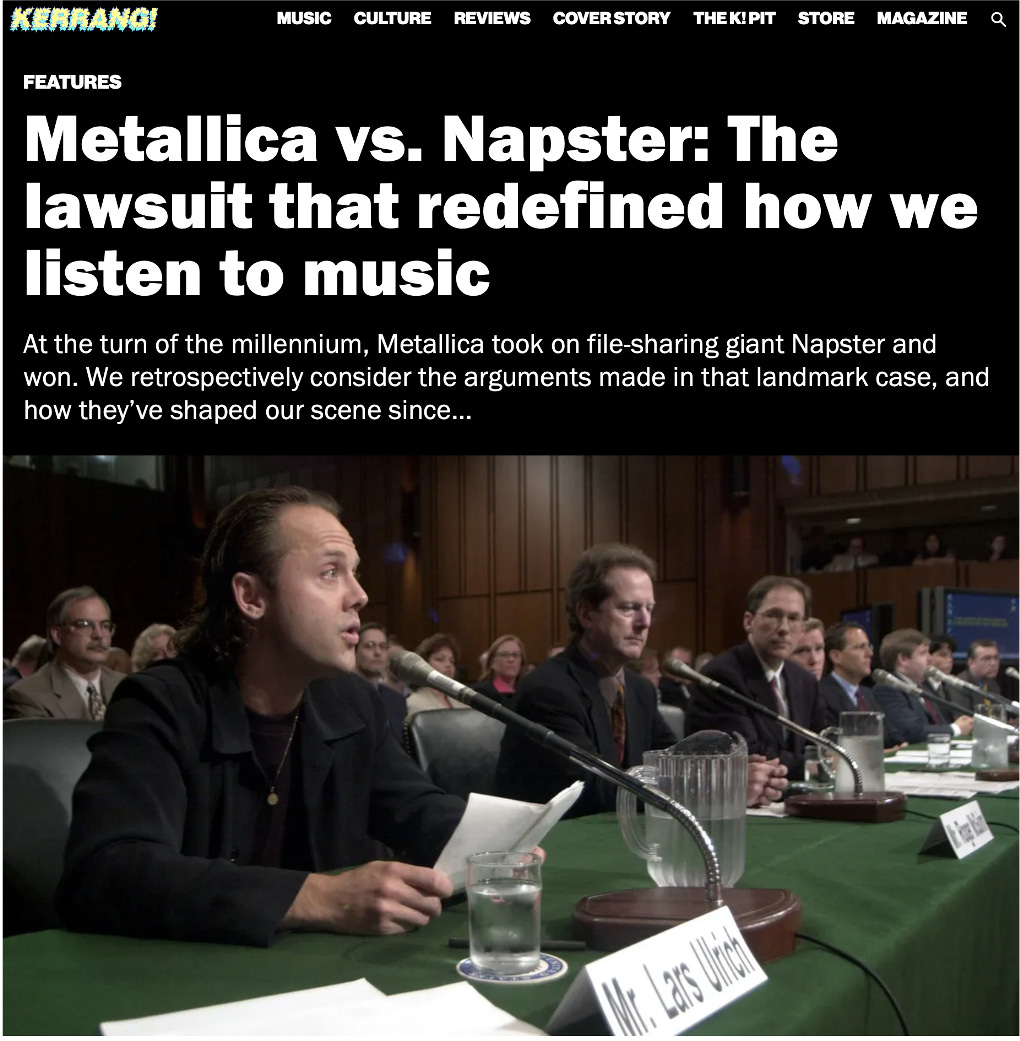

Napster arrived in 1999 and made peer-to-peer music sharing feel not just possible, but normal. Digital piracy spread rapidly. The old model, built around selling physical units at attractive economics, suddenly looked fragile in a world where one legal copy of a song could be reproduced and distributed endlessly at virtually zero cost.

Napster triggered a full-blown legal and economic crisis around digital rights, and the broader lesson was brutal for incumbents: they had not lost the value of music, but control over the channel through which that value had been monetized.

Metallica’s fight with Napster was really a fight over control of monetization in the digital age. Napster showed that a new distribution technology could scale rapidly by routing around copyright, forcing the courts to decide whether innovation gave tech platforms the right to build on protected works without permission.

Today’s AI lawsuits raise a strikingly similar question: can model developers train and commercialize powerful systems using copyrighted books, lyrics, art, and journalism without licensing them first? As with Napster, the technology is new, but the core economic issue is not... who owns the asset, and who has the right to get paid when it is used?

That was the bear case.

And, to be fair, it was a serious one.

If music could be copied infinitely and distributed for free, then what exactly was left to own? If technology had turned the product into a commodity, then perhaps the royalty claim sitting on top of it had become structurally impaired. For a time, that looked plausible. The industry was not merely cyclical. It appeared wounded at the root.

That is why music, for years, did not look like a beautiful royalty asset. It looked like a cautionary tale about what technology can do to legacy profit pools.

But that is not where the story ended.

Because the industry did something investors often underestimate: it adapted.

UMG’s 2025 annual report makes the point with unusual clarity. Management writes that trying to smother emerging technology is futile and often counterproductive, and it frames the relationship between music and technology as a century-long pattern of adaptation and growth.

That is a very important admission. It means the winners in this industry were never going to be the companies that tried to freeze the world in place. The winners were going to be the ones that learned how to make new rails work for them.

And that adaptation is now visible in the numbers.

According to IFPI, global recorded-music revenue grew 6.4% in 2025 to $31.7 billion, marking the eleventh consecutive year of growth. Total streaming revenue surpassed $22 billion and accounted for 69.6% of global recorded-music income, while paid subscription streaming alone represented 52.4% of the total. There are now 837 million paid streaming subscription accounts globally. In other words, the product did not die. The revenue model changed. And once the model changed, the industry began to look far healthier than the old panic ever imagined.

But even that understates what is happening.

Because the real opportunity is no longer just streaming.

It is the widening of the royalty surface.

UMG’s annual report shows a business that is being monetized across far more outlets than the old CD-era model ever allowed.

The company now generates revenue not only through global streaming platforms such as Spotify, Apple, YouTube, Amazon, Deezer, Tencent Music, and NetEase, but also through social media and short-form video, through digital-fitness partners, through gaming environments, and through licensing across film, television, advertising, and video games.

This is the key shift. Technology did not simply rescue the industry. It multiplied the number of places where music can earn a toll.

Then there is the direct relationship with the fan. That may prove even more important over time. UMG is now explicitly leaning into what it calls the superfan opportunity. In its 2025 annual report, the company says superfandom has been at the heart of its growth strategy for years and highlights new products and experiences designed to unlock spending beyond the traditional streaming subscription.

It also notes that its global e-commerce infrastructure now supports more than 1,600 owned and operated artist and branded online stores. That is a very different business from the one investors used to dismiss as a label living at the mercy of radio play and retail shelf space. It is a rights platform that is steadily deepening its direct economic relationship with the most passionate end users.

And now the industry is facing another technological wave.

This time, it is AI.

That threat is real. But it is also familiar. The panic sounds new... the underlying question is not. Once again, the issue is whether new technology destroys the economics or broadens them for the owners of the strongest rights.

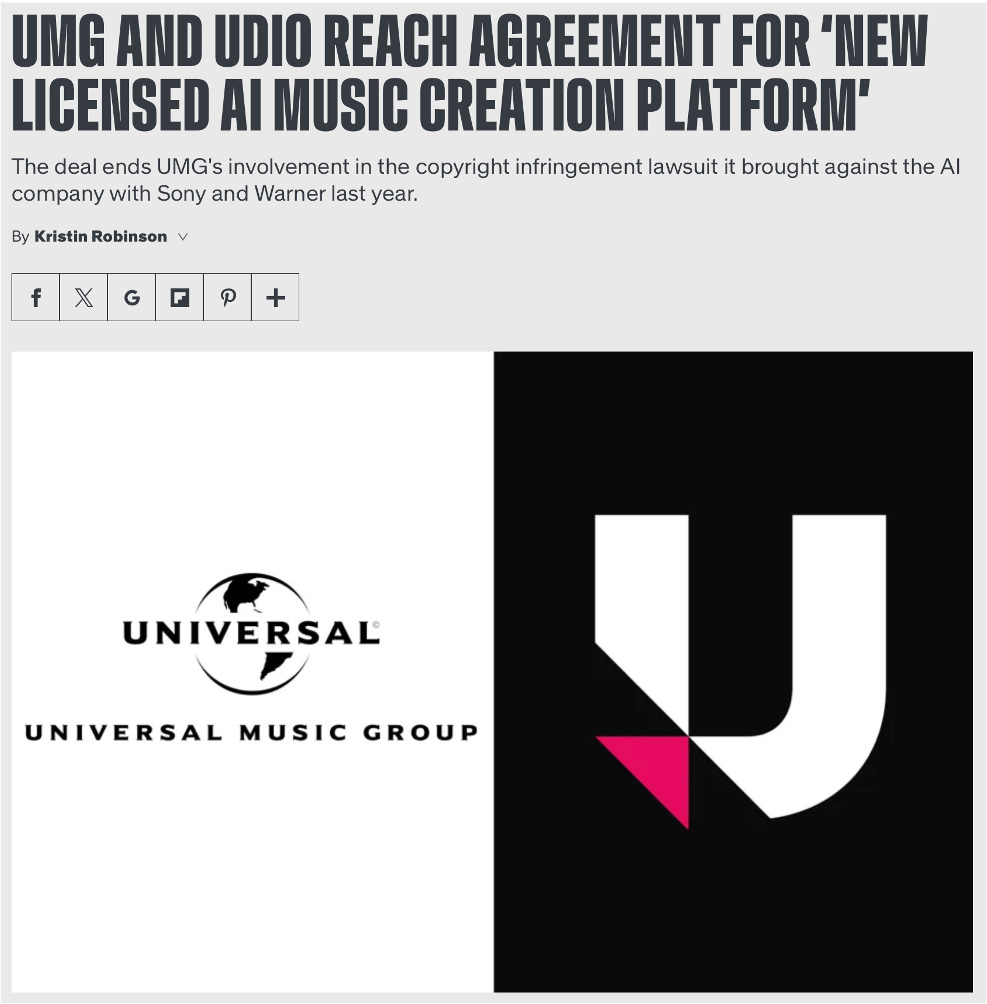

UMG’s deal with Udio (the AI music startup backed by Marc Andreessen’s firm) matters because it suggests the industry is trying to turn a legal threat into a licensed revenue stream. UMG says its agreement with Udio is part of its “Responsible AI” strategy, while Reuters reported that the partnership followed a settlement and is aimed at building AI music tools trained on licensed music rather than simply scraping copyrighted works.

The strategic message is simple: instead of fighting a losing battle against every AI music tool, UMG is trying to shape the next model of monetization, one in which owners of the catalog get paid when their intellectual property becomes the foundation for new creative products.

The bear case is easy to understand. AI can generate music-like content at enormous scale. It can flood platforms with cheap, low-friction output. It can make supply feel infinite. And when supply appears infinite, investors understandably worry that value itself will collapse.

But that conclusion is far too simplistic.

Because abundance does not eliminate the value of scarcity. In many cases, it sharpens it.

When low-value content becomes effectively infinite, what becomes more precious is what cannot be industrially faked so easily: genuine talent, cultural relevance, emotional resonance, fan attachment, and the accumulated intellectual property of artists people already care about. In other words, the more the internet fills with generic output, the more valuable authentic signal may become.

We have seen this movie before in other markets.

When quantity explodes, quality does not disappear. It often becomes easier to identify and more important to own.

That is why we think the right analogy is not “AI will make music worthless.” The better analogy is: AI will force the industry to separate authorized value from unauthorized noise.

And UMG appears to be moving in exactly that direction.

Its 2025 annual report says the company became the first media company to enter AI-related agreements with established platforms such as YouTube, Meta, TikTok, and KDDI, as well as with emerging AI companies. UMG also says those agreements were designed both to protect artists and songwriters and to develop new revenue streams and commercial opportunities.

Just as importantly, management says its artist-centric platform agreements include provisions that prevent AI “slop” from being counted in the same royalty pools as music from real artists and songwriters. That is a crucial point. It suggests the company is not merely defending against dilution. It is trying to shape the rules of the next royalty system.

This is also where the parallel with Adobe ( ADBE 0.00%↑ ) becomes especially interesting.

Adobe’s Firefly models were trained on licensed content such as Adobe Stock and public-domain material where copyright has expired, and Adobe also offers Custom Models that allow users to generate content based on their own assets, styles, and brand language.

That is a very important template. It shows how generative AI can be commercialized in a way that respects ownership, provenance, and licensing rather than simply scraping the open web and hoping the legal system catches up later.

Our view is that music is likely to move in a similar direction over time: not toward open-season expropriation of valuable catalogs, but toward licensed training, authenticated provenance, and monetization frameworks built around the actual owners of the rights.

And if that is the direction of travel, then the conclusion becomes far more interesting than the panic suggests.

AI-generated content may indeed make music supply feel endless. But endless supply is not the same thing as endless value.

The songs that matter will still matter.

The voices that move people will still move people.

The catalogs that already sit at the center of global culture will still occupy privileged positions.

And if those catalogs become the training ground, reference layer, or licensed substrate for new creative tools and new distribution formats, then the owners of those rights may discover that this new technological wave expands the royalty surface rather than destroying it.

That, at least, is our working view.

It is also entirely consistent with what the industry did after Napster and peer-to-peer piracy. It adapted. It changed the rails. It rebuilt the economics. And then it grew again.

Today, UMG is trying to do something similar through what it calls Streaming 2.0, with agreements covering Amazon, Spotify, and YouTube that it says encourage smarter customer segmentation, greater consumer value, ARPU growth, new paid tiers, richer content bundles, and better protections against fraud and irrelevant uploads.

That does not eliminate the risk.

But it does show a company trying to architect the next phase of monetization rather than merely defend the last one.

This is why we think investors should stop looking at music through the old lens. The old lens says the business was disrupted. The better lens says the business was forced to evolve from a narrow distribution model into a much broader royalty machine.

In our view, that distinction is everything. Because once music is understood that way, Universal Music Group starts to look less like a media stock and more like what it really is: one of the most important public claims on a global catalog of premium intellectual property whose monetization surface is still widening.

The most pressing question now is obvious: how should we value it?

You will also like reading:

The Privileged Position

One of the things I find most satisfying about serious research is this: When you do the work properly, top down and bottom up often end up shaking hands.

By the way, have you check our latest leaderboard?

It tells the story better than any intro, showing our total returns since publication, including multiple triple-digit winners and a consistent record of beating the market while managing risk.