The Privileged Position

Own the Right Claim, Let Others do the Heavy Lifting: Tracking the World's Best Seat in the House

One of the things I find most satisfying about serious research is this: When you do the work properly, top down and bottom up often end up shaking hands.

In VMF’s Strategic Asset Allocation, we start with the regime, the macro backdrop, the big shifts in liquidity, power, scarcity, and innovation. In VMF’s Security Selection, we do the opposite. We build from the bottom up. We study the asset, the economics, the claim, the incentives. And yet, again and again, the work keeps leading us to the same places.

That is exactly what happened in April’s issue of VMF’s Security Selection.

The excerpt below is the first section of that issue, and it offers a glimpse into one of the business models we admire most in all of capitalism: the royalty model.

Why? Because when the underlying asset is right, royalties create the kind of economics investors dream about. You own the superior claim. Someone else does the hard work. You participate in the stream without carrying the full burden of operating risk, capital intensity, or execution strain.

That is the theory.

But the real fun starts when you go looking for that model outside the obvious places.

Most investors can spot a royalty business in mining or energy. Far fewer are trained to recognize the same architecture when it appears in stranger corners of the market. We look for it tirelessly, across sectors, because some of the best seats in the house are hidden in plain sight.

In this first excerpt, you’ll see exactly that. We revisit two royalty businesses already sitting in our Model Portfolios and explain why they continue to prove just how powerful this model can be when attached to the right asset.

The more actionable conclusions, as always, remain where they belong.

But the thinking begins here.

Here is “The Privileged Position.”

Long before royalties were paid to songwriters, they were paid to kings.

That is not a metaphor. It is the literal origin of the word. Royalty first referred to royal power, royal rights, and the prerogatives of the sovereign.

Only later did the meaning broaden into the commercial sense investors know today: a recurring payment made to the owner of a valuable right by someone else who is permitted to exploit it. Britannica’s legal definition is about as clean as it gets: a royalty is a payment made to the owners of certain rights by those allowed to exercise them, whether the underlying right concerns mineral deposits, patents, or copyright.

The asset changes. The logic does not.

And that is precisely why the model has proven so durable.

At its core, a royalty is one of the cleanest economic arrangements ever created. One party owns the right. Another party brings the labor, the capital, the machinery, the distribution, and the day-to-day operating burden required to exploit that right. The owner does not need to run the mine, drill the well, print the book, or perform the song. The owner only needs to hold the superior claim. That is what makes the model so elegant. It separates ownership from operation.

And when that ownership is attached to the right kind of asset, the result can be extraordinary: long-duration cash flows, upside to rising output and rising prices, embedded inflation protection, and exposure to future expansions the royalty holder did not have to finance.

Of course, that last point is everything.

Because a royalty on the wrong asset is just a legal claim with a nice name. The magic appears only when the underlying asset is scarce, valuable, and tied to demand that endures through time.

That is why the model became so powerful first in the natural-resource world...

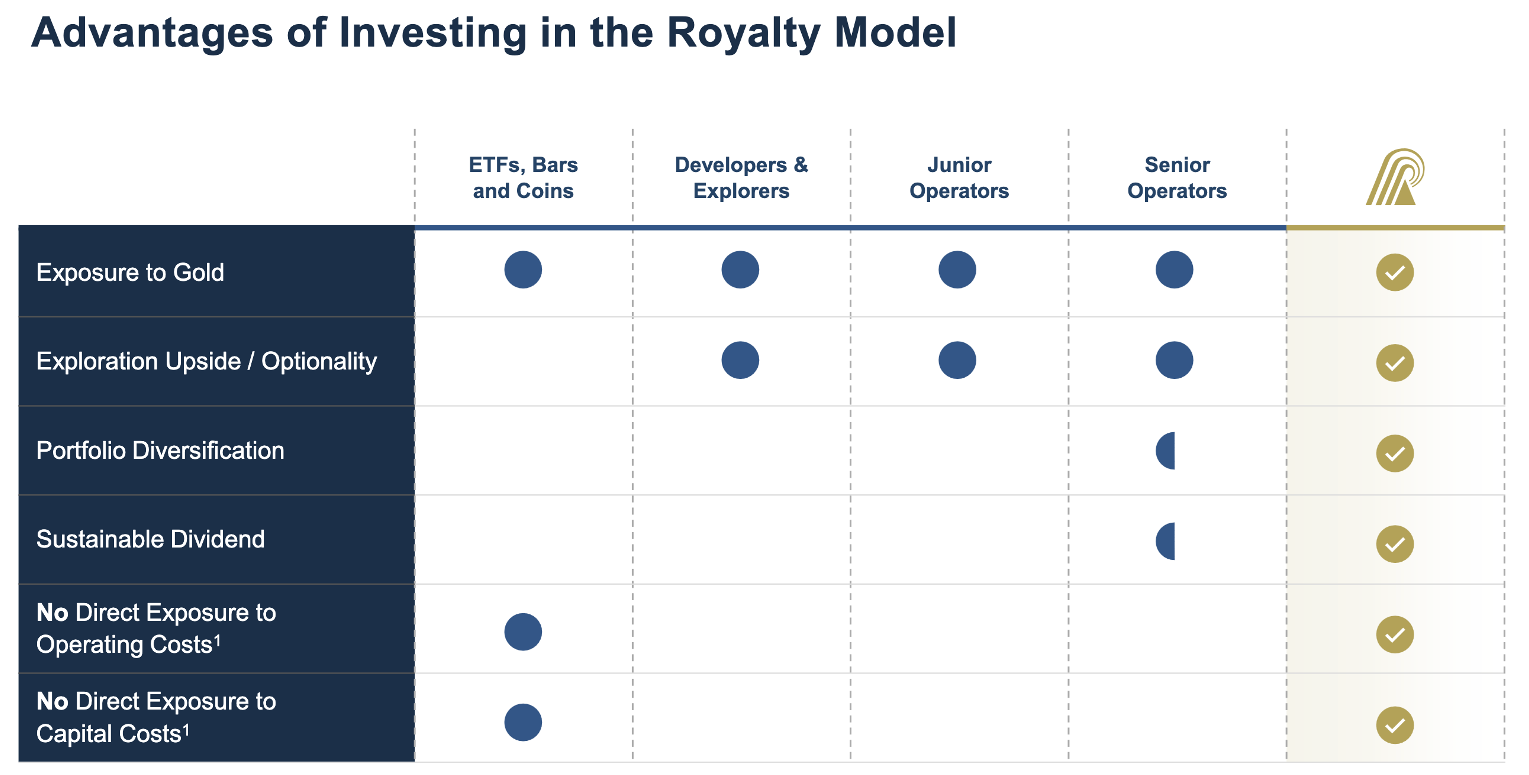

This chart comes from Royal Gold, one of the most prominent precious metals royalty and streaming companies in the world. It is a useful visual illustration of why many investors are drawn to this model: compared with direct operators, royalty companies often retain exposure to rising commodity prices and exploration upside while avoiding much of the cost inflation, capital intensity, and operational risk that burden traditional miners.

The landowner or sovereign did not need to assume geological risk, operating risk, labor risk, or capital-allocation risk.

If the operator succeeded... the royalty holder participated.

If the ore body expanded... the royalty holder participated again.

If inflation lifted the value of what came out of the ground... the royalty holder was paid once more.

The operator did the hard work. The royalty owner held the superior economic seat.

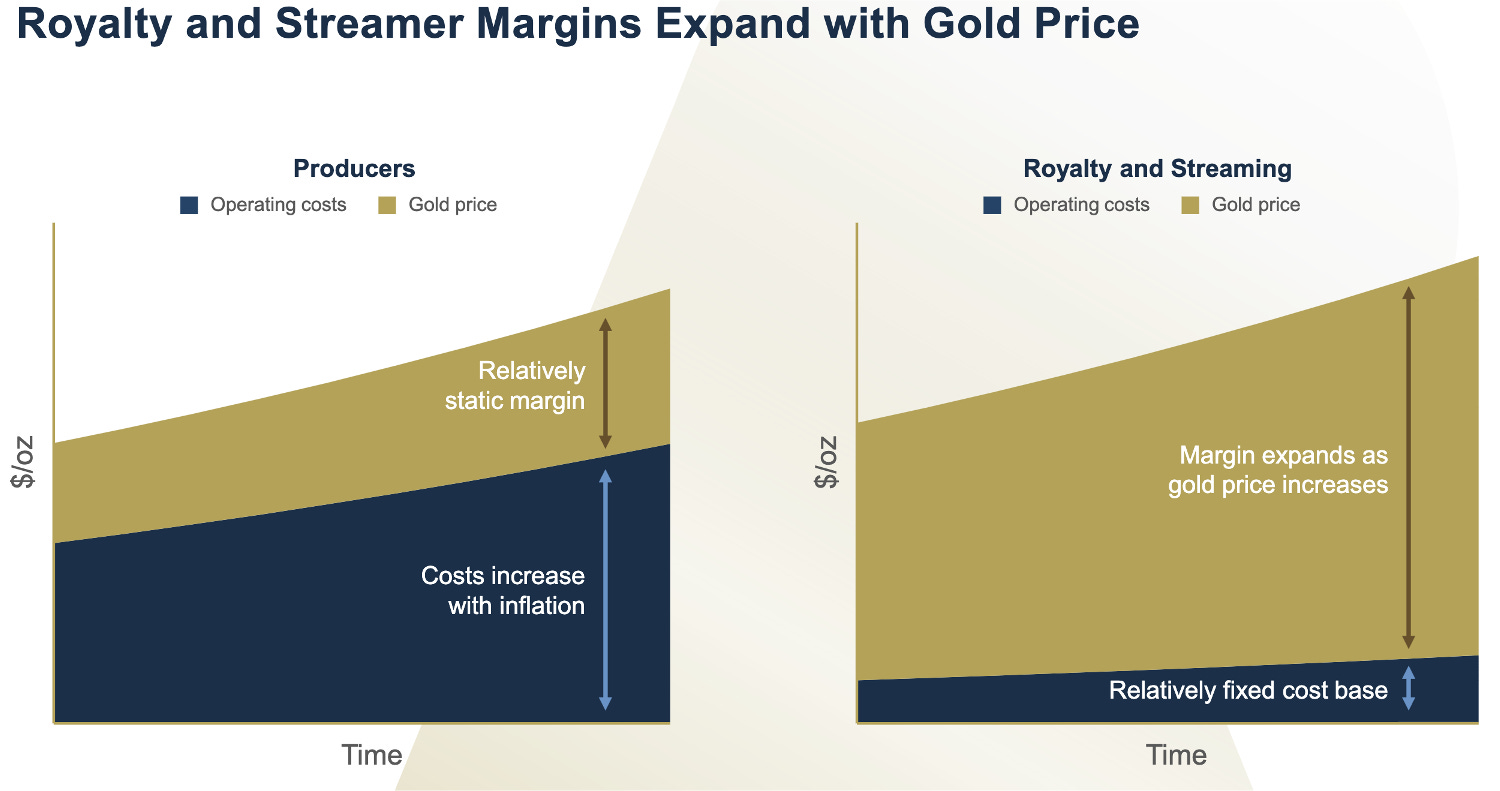

This chart, also taken from Royal Gold’s investor presentation, illustrates one of the most attractive features of the royalty model: margin expansion as the gold price rises. For a traditional miner, higher gold prices often come with higher operating costs as inflation pushes up labor, energy, reagents, transport, and other on-site expenses. The result is that part of the benefit from a stronger gold price is often absorbed by a rising cost base. A royalty company is structurally different.

Because it does not operate the mine itself, its cost base is far more stable and much less exposed to the inflationary pressures that burden producers.

Then, over time, the model made one of the most interesting migrations in economic history: from the physical world into the world of ideas.

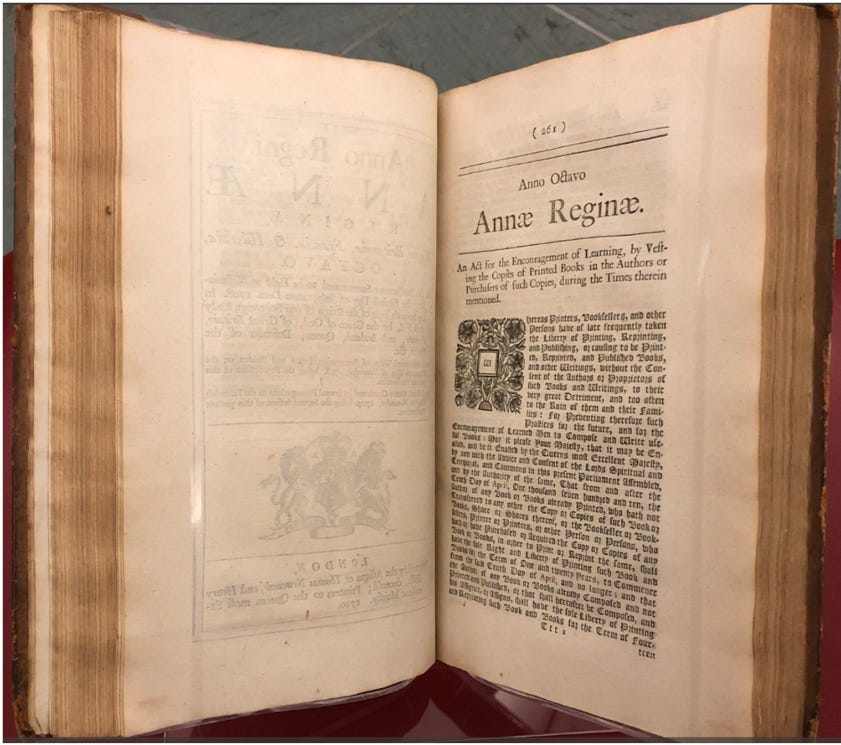

The key legal hinge was the Statute of Anne in 1710, which marked a milestone in copyright law by recognizing that authors, rather than only printers or distributors, should be the primary beneficiaries of copyright protection.

Once that door opened, the royalty model no longer needed a mine, a field, or a well. It could attach itself to books, inventions, songs, designs, and every other form of intellectual property that could be owned separately from the effort required to commercialize it.

The extractive logic survived. Only the asset changed.

And that is exactly why investors should think about royalties in broader terms than they usually do.

In fact, one of the most famous royalty-like businesses in the modern world is not a miner, an oil company, or a music publisher.

It is McDonald’s.

Most people think of McDonald’s as a restaurant company.

That is understandable... but economically, it is incomplete.

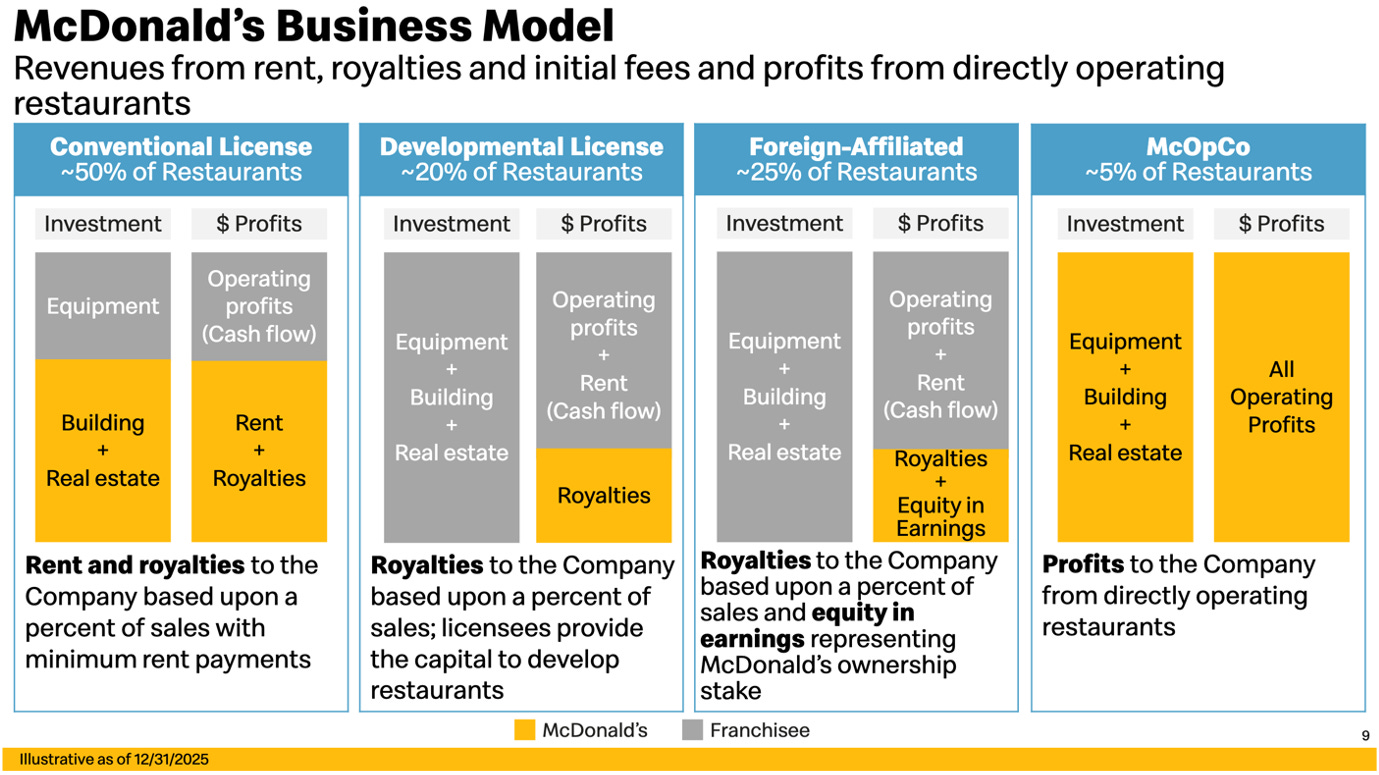

McDonald’s own investor materials describe a business model built around revenues from rent, royalties, and initial fees, alongside the smaller profit contribution from directly operated restaurants.

The company also says that roughly 95% of its restaurants are locally owned and operated, while its annual report explains that conventional franchisees contribute primarily through rent and royalties based upon a percent of sales. In other words, the golden arches may be what the customer sees, but underneath them sits a structure that behaves far more like a royalty-and-rent machine than a pure restaurant operator.

That distinction matters because it reveals the model’s true elegance.

The franchisee takes on much of the operational grind: labor, local execution, staffing, and day-to-day management. McDonald’s, by contrast, occupies the superior economic position. It controls the brand, controls the system, often controls the real estate, and collects a recurring share of the stream. It is not a pure royalty company in the way a mineral owner is. But the family resemblance is unmistakable.

Once again, the model separates ownership from operation... and that separation is where so much of the beauty lies. Because that broader lesson is the one we want you to keep in mind before we go any further:

The royalty model is not confined to one sector, one legal structure, or one corner of the market. It appears wherever a valuable right can be owned separately from the effort required to exploit it.

Sometimes that right sits under the ground.

Sometimes it hangs above a storefront.

And sometimes it lives inside a catalog.

What matters is not the wrapper...

What matters is the quality of the underlying asset and the quality of the claim.

That is also why this framework is already familiar to our long-term subscribers.

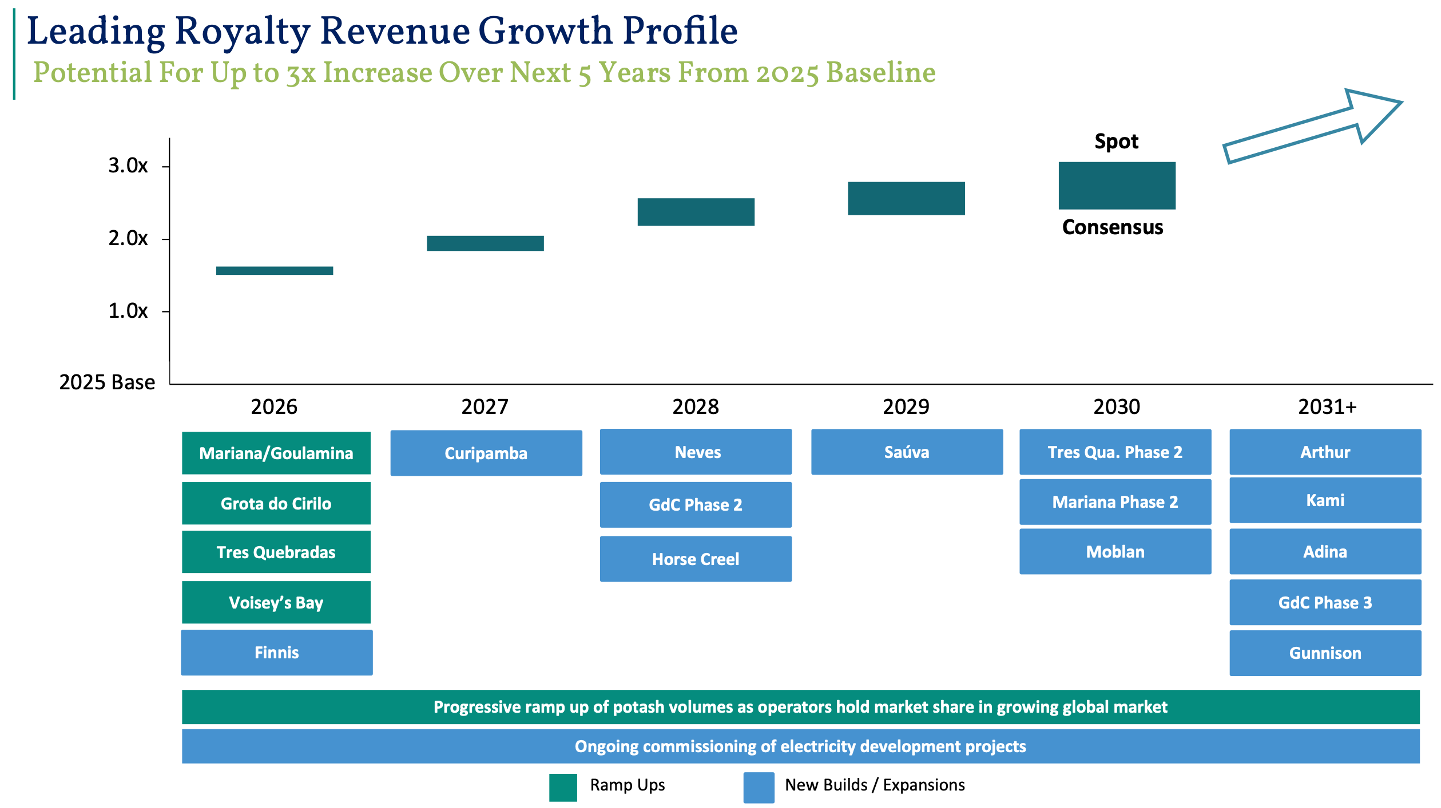

We have already seen what a truly exceptional royalty business can do inside our own Model Portfolios, and no holding illustrates that better than Altius Minerals ($ALS.TO).

As of today, our original May 2024 recommendation already shows a 140%total return, and in March we explicitly reminded readers that we still saw meaningful upside ahead.

But the return, impressive as it is, is only half the story.

The more important point is why Altius has performed so well. From the very beginning, we did not treat it as just another royalty company. We treated it as something more unusual... and more valuable.

That is because Altius does something most royalty businesses do not.

It does not merely collect royalties.

It creates them.

That distinction is everything.

We expect Altius Minerals’ royalty portfolio to expand materially over the next few years, and the most important feature of that growth is asset longevity. Much of the expected expansion comes from exceptionally long-life assets that can pay royalties for decades, not just years. That gives Altius exposure not only to higher production volumes as those assets ramp and expand, but also to higher commodity prices over time... all without bearing the capital burden of operating them.

In our last issue, we put it as clearly as we ever have: Altius is not merely a passive owner of royalty interests. It is an active creator of them.

Through its Project Generation arm, it identifies geological opportunities early, advances them intelligently, retains royalties and equity where appropriate, and monetizes selectively when timing and price are right. In other words, it is not just collecting optionality. It is constantly manufacturing more of it.

That is why we have always labeled Altius as “Special.”

The existing royalty portfolio is only part of the story. Behind it sits a continuously renewing pipeline of internally generated opportunities, built by a team with an unusual ability to surface value long before the market is prepared to recognize it.

We also own Viper Energy VNOM 0.00%↑ , which sits in a different industry but follows the same essential economic logic.

Viper is not a driller. It does not need to guess which operator will execute best quarter to quarter, nor does it need to fund the endless treadmill of rigs, crews, completions, and service costs.

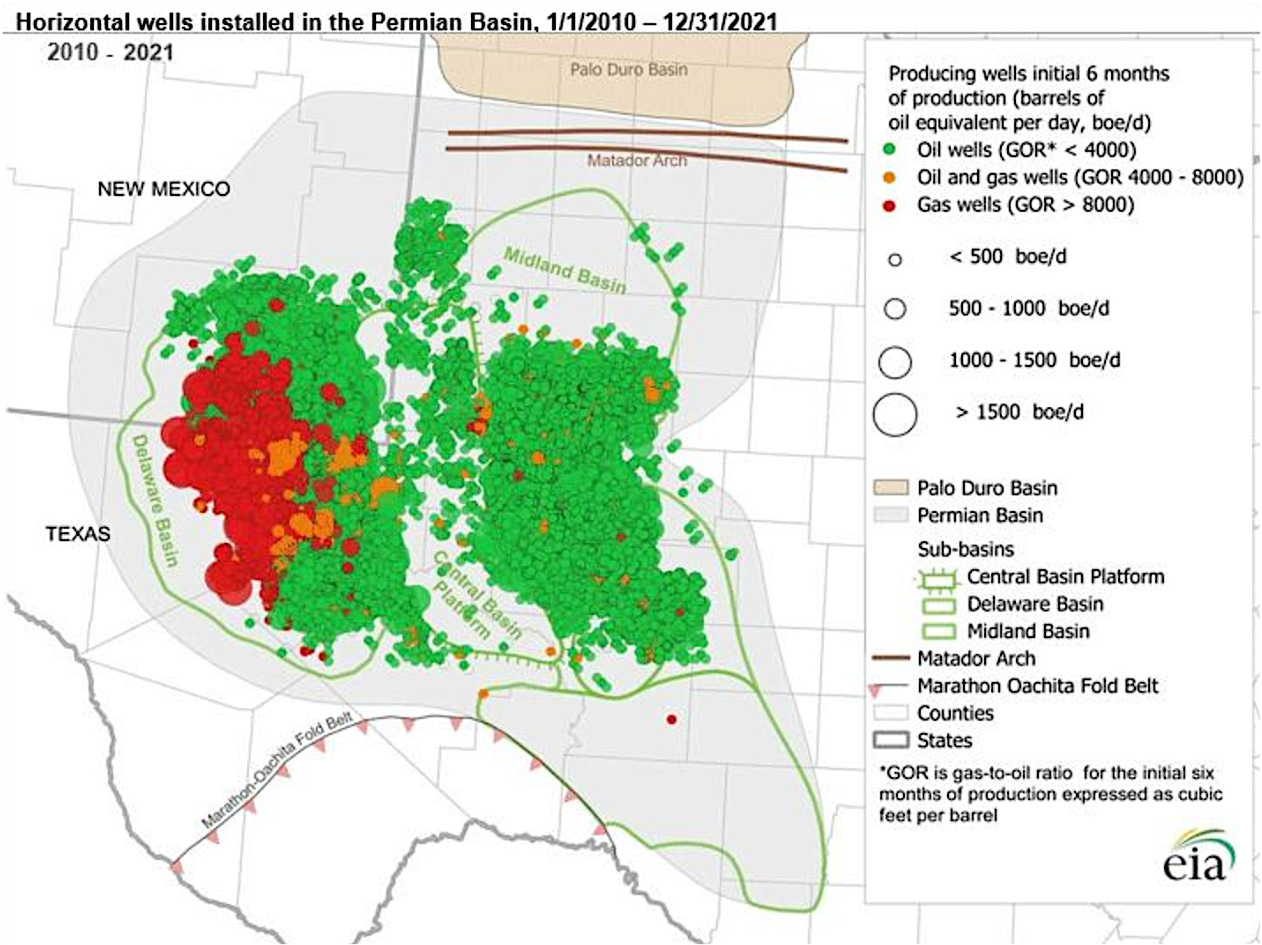

It owns mineral and royalty interests in the Permian Basin... and that is precisely where you want to hold them.

Why? Because not all barrels are created equal.

If you are going to own a royalty on oil and gas, you want it attached to the rock that serious operators come back to again and again... the basin with the deepest inventory, the strongest economics, the richest infrastructure, and the greatest strategic importance to U.S. production.

You want the place where capital naturally gravitates, even when the industry turns cautious. You want the basin that keeps getting drilled because, in a capital intensive business, the best acreage is the last acreage management teams want to abandon.

That is the Permian.

The Permian is not just another oil basin. It is the center of gravity in U.S. crude production. In 2025, it pumped 6.6 million barrels per day and accounted for 48% of total U.S. crude output, with most of the year’s production growth coming from the basin. Stretching across West Texas and Southeast New Mexico, its Delaware and Midland sub-basins form one of the most prolific hydrocarbon systems in the world.

It is not merely another oil patch.

It is the crown jewel of American shale... the place where geology, scale, infrastructure, and operator attention all converge. Pipelines are there. Processing is there. Service capacity is there. The majors are there. The independents are there. And because the rock is so attractive, the basin keeps pulling capital toward itself.

Viper’s royalty interests are not sitting on marginal acreage that needs heroic assumptions to work. They sit in the part of the oil market where activity tends to be the most durable and where the best operators keep doing the hard work for you.

That is the beauty of the model.

The operators spend the capital. They drill the wells. They bear the execution

burden. They manage the decline curves, the service costs, the logistics, and the headaches that come with extracting hydrocarbons from the ground.

Viper collects a slice of the stream.

Different asset. Different industry. Same superior architecture: own the right claim, let others do the heavy lifting, and participate in the output. So, when we say that the royalty model deserves to be taken seriously, we are not speaking in the abstract.

We have already seen its power in minerals.

We have already seen it in energy.

And we have already seen how extraordinary the economics can become when the underlying asset is truly world-class and the claim sitting on top of it is structurally superior.

But now we want to take that same idea one step further. Because the next royalty business we are about to present does not sit on a metal deposit or an oil basin. It does not depend on drilling schedules or reserve reports.

Its assets are no less real for being intangible... and in some ways, they may be even more remarkable. They live in the culture. And they get consumed every day.

This month, we are going to argue that one of the most compelling royalty assets in the modern world is not buried underground at all.

It gets played.

Continuing in part 2:

The framework is now complete.

I’ve just released Part 2: “After Napster, Before AI.”

If Part 1 was about the architectural beauty of the "Privileged Position," Part 2 is about the stress test.

I take the royalty model and apply it to the most disrupted industry in history: Music.

We look at how the "monetization surface" is widening again, and why the market is mispricing the impact of AI on the strongest rights holders.

You can read the continuation here:

https://marketview.vmfresearch.com/p/after-napster-before-ai

Good investing.

Vasco