AI Losers... or Mispriced Survivors?

Software is getting easier to code, but trust is getting harder to clone. Here’s why we’re watching the support zone while the herd runs for the exit.

On December 20, 2025, I published here on Substack a free excerpt from VMF’s Security Selection: our investment thesis on Adobe. The core claim was simple, and deliberately non-consensus. Adobe was being priced like an “AI loser,” while the business was still compounding.

Since then, a lot has happened. Not just in Adobe’s stock, but in the market’s psychology around what AI will commoditize. And because we take accountability seriously, we owed readers an update.

So today I’m going to show you what we just did behind the paywall in February’s issue of VMF’s Security Selection, titled “Stress Test.” In that issue, we went back to first principles and did the work most investors skip in an AI panic: we stress-tested the value proposition. Not the chart. Not the multiple. The value proposition.

That distinction matters because we believe the market is making a category error. It is treating “software” as if it were the moat. In the AI era, code becomes abundant. The marginal cost of producing “good enough” software trends toward zero. If your moat is code, you’re in trouble.

But Adobe’s moat was never code.

Adobe’s value proposition is embeddedness. It sits inside professional workflows, file standards, collaboration, agencies, procurement, and delivery pipelines. It is the default layer where creative work gets produced, refined, approved, and shipped. And in commercial environments, the real switching cost is not the subscription fee. It’s the operational and reputational risk of breaking the workflow. That’s where trust becomes a moat. That’s where FOMU shows up: fear of messing up when the output is client-facing, regulated, or brand-sensitive.

In short, the market is debating whether AI can generate outputs. Enterprises are deciding who they can safely deploy in production.

In the excerpt below, we update the Adobe thesis through that lens.

One final note: in our February “Stress Test,” Adobe was only one case study. We also covered a broader and more numerous stable of AI winners than perceived AI losers. For now, the actionable positioning and the rest of that work remain behind the paywall.

Here is the excerpt.

This next section is where the difficult work begins.

These are the companies in our Model Portfolios that the market is already pricing as AI losers... as if AI is about to turn their products into commodities, crush their margins, and make their business models obsolete… the way streaming did to Blockbuster.

And there’s no better place to start than Adobe ADBE 0.00%↑ . Why? Because our entire investment thesis in the November 2025 issue was built on one simple observation: Adobe was being treated like a casualty of the “SaaSpocalypse”... and we didn’t buy it.

Since then, that disconnect (between the value we believe Adobe is building and the price the market is willing to pay for it) has only widened.

So, this is exactly where we do what we said we would do all along in this issue: we stress-test the value proposition. Not the stock chart. Not the multiple. The value proposition.

And when you apply the SaaSpocalypse logic properly, Adobe starts to look less like a victim... and more like a beneficiary.

Because the market panic is built on a category mistake: it confuses “software” with “moat.” It assumes that if software becomes easier to create, then software companies become easier to replace.

But Adobe’s moat was never “code.”

Adobe’s moat is embeddedness.

It’s the fact that creative work doesn’t live in a vacuum. It lives in professional workflows... file standards, team collaboration, agencies, and enterprise procurement.

It lives in careers built around specific tools, in deadlines, in reputations, and in brand risk. And it lives in something AI still can’t “commoditize” on command: taste: the ability to curate, refine, and choose the right output from a universe of possibilities.

That’s exactly why tools like Firefly1 matter: they don’t just generate more options... they accelerate the messy, iterative process of exploring, narrowing, and polishing, so the professional gets to the right visual answer faster.

You can clone an interface.

But you can’t clone the ecosystem that makes the interface the default.

And in Adobe’s world, the switching costs aren’t the subscription fee.

The switching costs are the risk of breaking a pipeline, corrupting assets, losing brand consistency, missing a deliverable, or producing something that looks right but isn’t commercially usable.

That’s where FOMU comes in (fear of messing up). For commercial buyers, “good enough” isn’t good enough when the output is client facing, regulated, or reputation-sensitive.

That’s why trust becomes a moat... not in the abstract, but in the real-world sense that professionals and procurement departments need a vendor they can defend when something goes wrong.

And Adobe has another edge that matters more in the AI era than investors want to admit: commercial safety. If generative AI becomes a production tool inside enterprises, the question isn’t “can it generate an image?” The question is: “can we use it without legal and brand blowback?” Adobe has leaned hard into commercially safe models and enterprise-grade workflows, exactly the kind of positioning that becomes more valuable as AI moves from experimentation into scale.

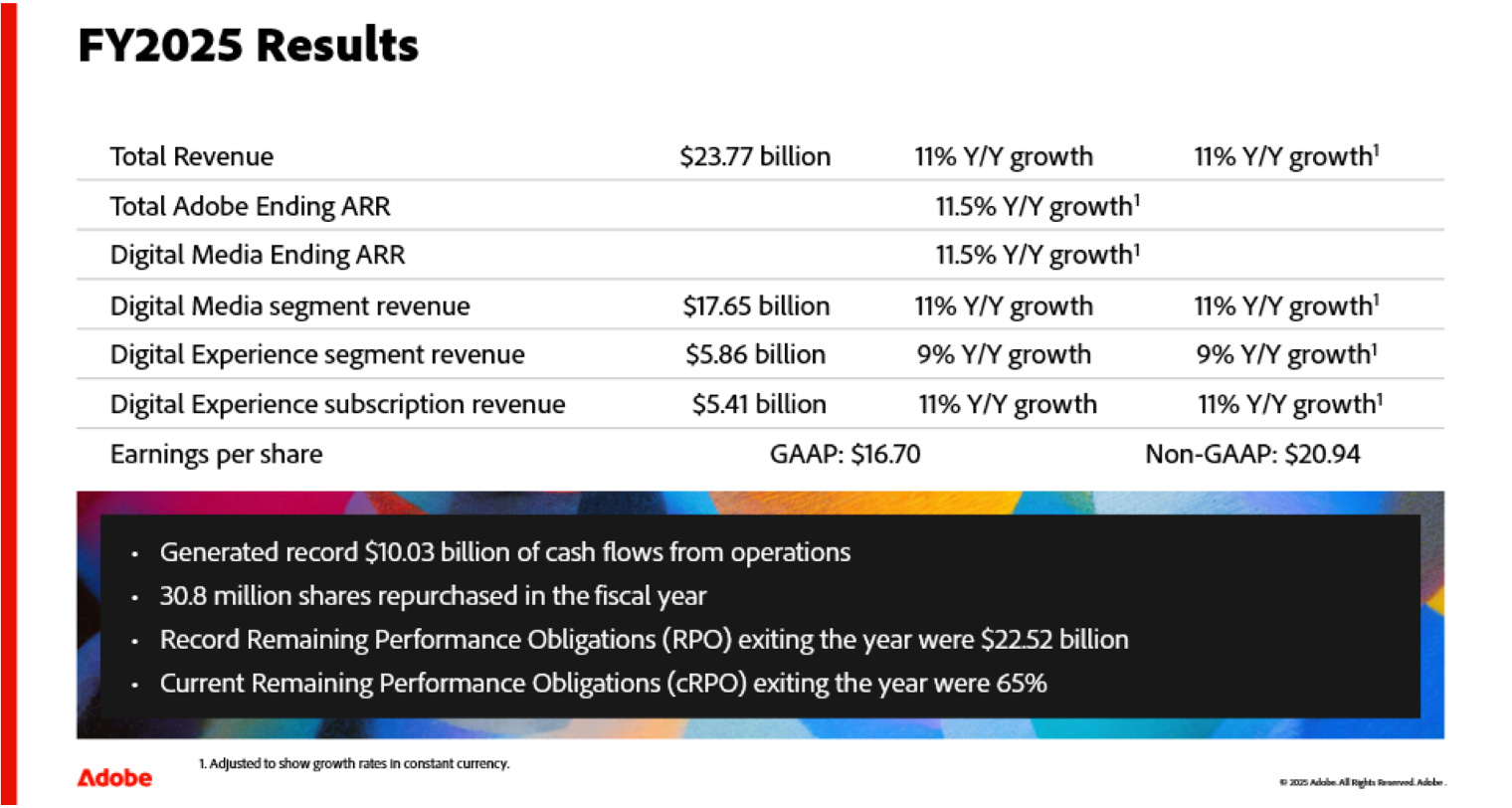

Most importantly: this isn’t just theory. We can see it in the results.

Since we published our original thesis, Adobe has done the opposite of what an AI loser story would predict. The company just printed record revenue, record operating cash flow, and continued to lean hard into shareholder returns, repurchasing enough stock in 2025 to shrink the share count by more than 6%.

And yet the market has continued to reprice Adobe as if its future is being erased, especially the long-dated terminal value investors used to pay up for. The result is a valuation that has been compressed to levels we simply don’t associate with a franchise of this quality: roughly ~11x forward earnings, ~11x EV/EBITDA, and a price-to-sales ratio below 5x... near historic lows.

One thing we’d love to see is insider buying, not because we need reassurance, but because at these prices the market is betting on a rapid evaporation of the business that the current fundamentals simply don’t support.

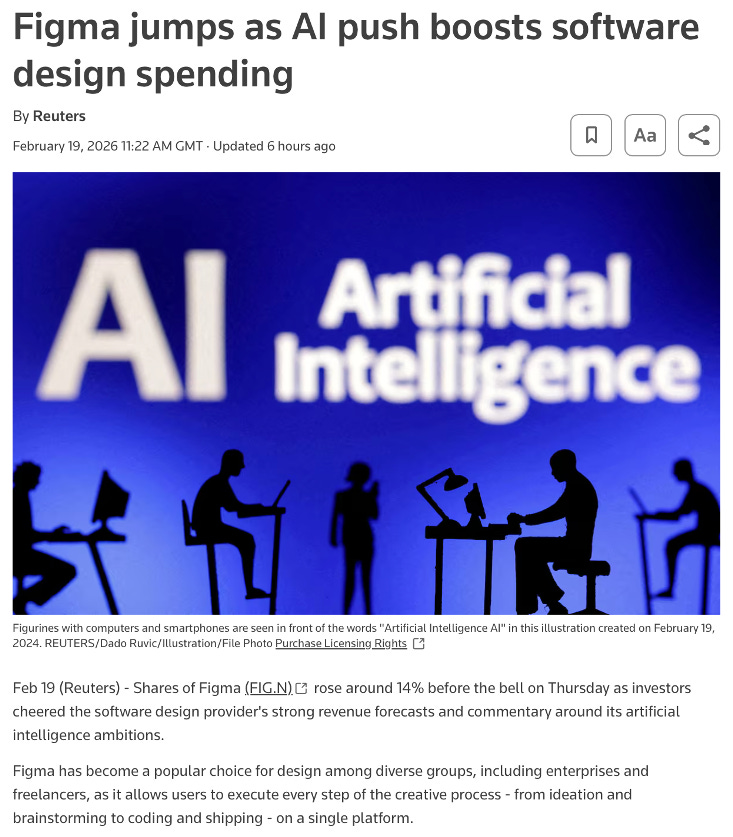

And if you want an even more up-to-date glimpse of what this business environment really looks like in real time, look at Figma (FIG):

Note that Figma’s market capitalization today sits around roughly $13 billion, materially below the approximately $20 billion valuation Adobe once offered to acquire it.

Remember, we featured Figma extensively in our original Adobe thesis, not just because it’s an excellent product, but because its attempted acquisition became the perfect case study in how strategically important modern creative workflows have become.

Adobe was willing to pay roughly $20 billion for that strategic position... until regulators forced the company to walk away.

Well, Figma is now giving us a live window into the same SaaSpocalypse tape that’s been punishing Adobe.

In its latest results and conference call, Figma guided to 2026 revenue around $1.36–$1.37 billion, well ahead of expectations... an upbeat message about demand and pricing power in the exact kind of workflow software the market claims

is about to be “vibe-coded into oblivion.”

And yet... the stock tells you what investors feel.

Figma is still sitting in a brutal drawdown, roughly 85% below the euphoric post-IPO peak it hit almost immediately after going public in late July 2025.

That price action is the market’s verdict on this entire category: not “your numbers are bad,” but “your future is suspect.”

Now zoom back out and look at Adobe through that same lens.

Adobe’s own chart is beginning to look like a historical stress test.

Shares are trading near the lower end of their yearly range (hovering just above the 52-week low), and the drawdown from the November 2021 all-time high is now in the same zip code as prior structural bear markets (2000 and 2008).

In fact, one dimension of this bear market already tops the last two: time. This drawdown has been grinding on for years... long enough to change psychology, long enough to scare off the weak hands, long enough to make even great businesses feel almost “uninvestable.”

So yes, this is an historic bear market for Adobe’s stock. Which is precisely why we’re treating the next major long-term support zone as a decision point. If we reach it, and the price action confirms it’s being defended, we will seriously consider increasing our allocation. Until then, we’ll keep this position on a tight leash.

You might also like reading:

Check our Leaderboard updates - Top 10 Positions - February 18th, 2026

Looking for where to start?

Adobe Firefly is Adobe’s family of generative AI models designed specifically for creative professionals. It enables users to generate and edit images, graphics, video, and design elements through text prompts and conversational tools integrated directly into applications like Photoshop, Illustrator, and Premiere. A key differentiator of Firefly is that it is trained on commercially safe data, including licensed content and Adobe Stock assets, making it suitable for professional and enterprise use where copyright and brand safety are critical.