The China AI Reset

How cheaper Chinese models shift the next wave of AI profits downstream.

The next AI shock may arrive as a price war.

Artificial intelligence is still framed as a contest for supremacy: who owns the largest compute cluster, trains the smartest model and raises the most capital. That contest has already created extraordinary fortunes.

It may now be obscuring the more consequential shift.

China is collapsing the cost of capable intelligence.

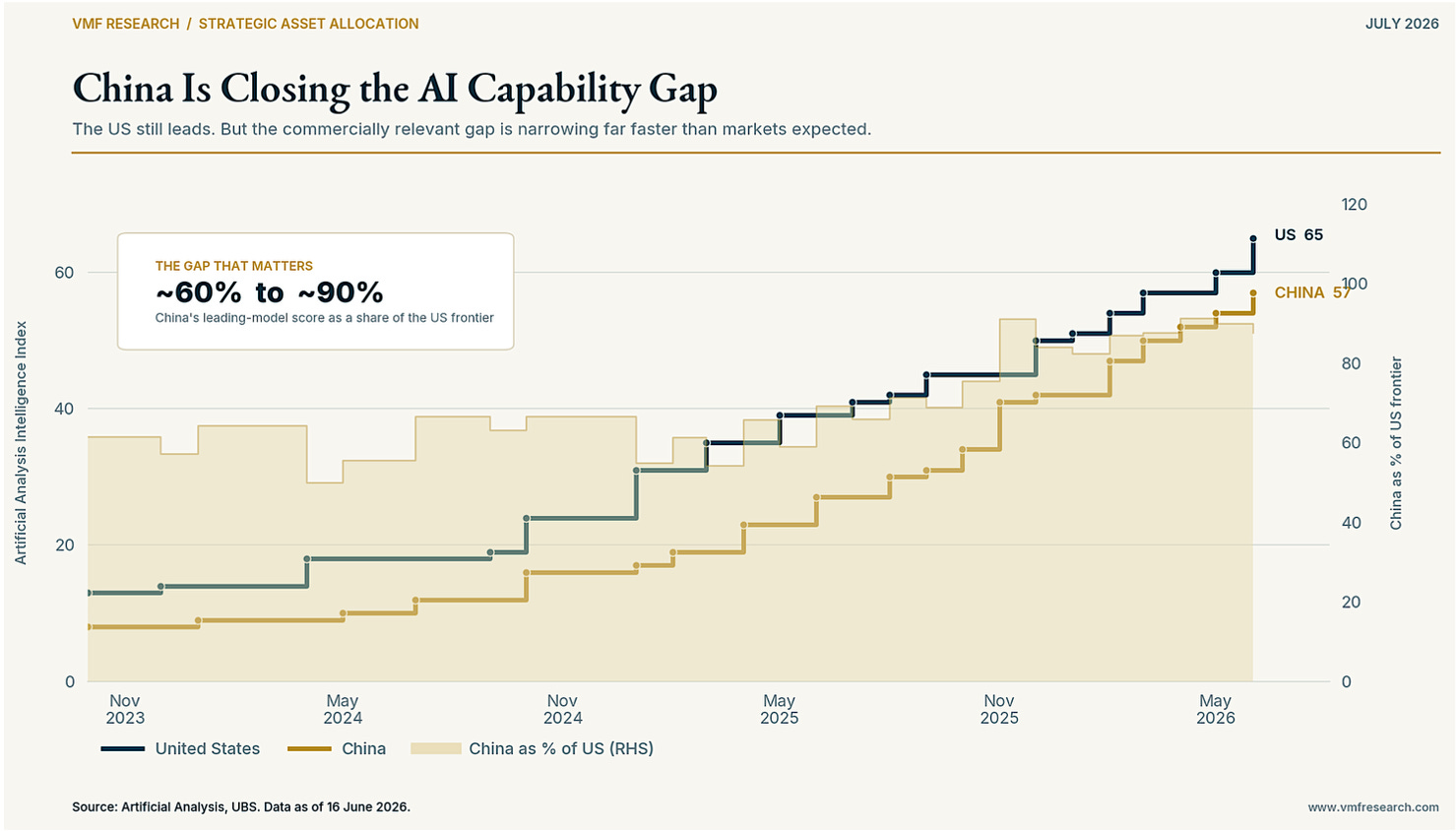

Its leading models are approaching the performance of the strongest American systems while charging a fraction of the price. UBS estimates that the capability gap has narrowed from roughly 40 percentage points in 2023 to around 10 today, while Chinese frontier-model prices can average less than one-fifth of those charged for comparable Western alternatives.

The numbers will change. The economics already have.

Most businesses do not need the best model ever built. They need one that completes the work reliably, securely and cheaply enough to produce an economic return.

A retailer does not need frontier-level reasoning to improve product search. A logistics company does not need the world’s smartest model to optimise routes. Thousands of routine coding, translation, customer-service and document-processing tasks can be handled by systems that are simply good enough at the right price.

A model does not need to win every benchmark.

It needs to win the workflow.

That is where China is becoming dangerous.

Restricted access to advanced chips, smaller research budgets and less abundant capital forced Chinese laboratories to solve a different problem from their American counterparts. They had to extract more capability from every unit of compute, every dollar of investment and every watt of electricity.

Constraint became an advantage.

Focused training, efficient architectures, open-weight collaboration and aggressive optimisation are allowing Chinese developers to compete near the frontier with a radically different cost structure. Early usage data suggest that customers are beginning to notice.

Chinese models are gaining traction on platforms where developers compare real systems for real work. Capability is converging. Prices are disruptive. Usage is following.

That combination can reset the economics of the entire industry.

Model providers face greater pricing pressure. Infrastructure companies may eventually need to defend scarcity premiums the market currently treats as permanent. Capital spending will face more scrutiny as customers focus less on token consumption and more on the return generated by each task completed.

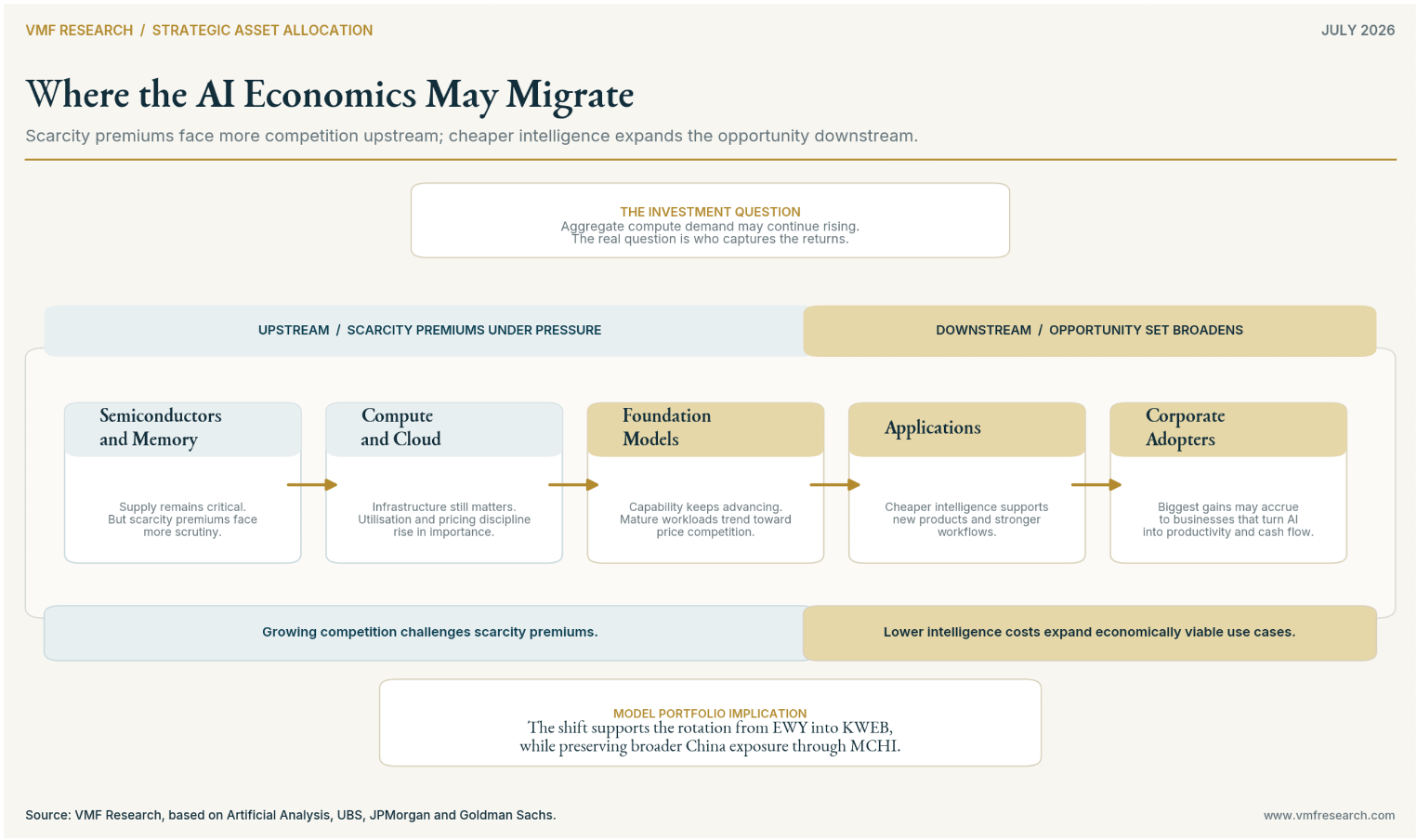

The most obvious beneficiaries may sit further downstream.

Cheaper intelligence gives businesses with customers, proprietary data, distribution and specialised workflows access to a more powerful input at a lower cost. It can improve advertising conversion, product discovery, logistics, software development, customer service and operating margins.

The value does not disappear when intelligence becomes cheaper.

It migrates towards those best positioned to use it.

That is the thread connecting much of our recent work at VMF Research. The Abundance Shock began with the idea that falling intelligence costs would rearrange scarcity and profitability across the economy. We then followed the AI trade from physical bottlenecks towards the application layer.

July reveals the force accelerating that migration.

China does not need to overtake the United States across every dimension of artificial intelligence. It does not need to dominate the American market or win the final increment of capability. It can transform the global profit pool by becoming the preferred cost-performance supplier for the enormous number of tasks where the absolute frontier adds little economic value.

That is a far more useful investment question than another argument about which country is “winning AI”.

The excerpt below examines China’s narrowing capability gap, the architecture behind its cost advantage and the evidence that users are already directing real workloads towards Chinese models.

It also raises the question at the heart of July’s research:

What happens when the next generation of AI winners are the companies buying intelligence rather than selling it?

The full issue translates that reset into the Tier One Model Portfolio’s exposure across Chinese equities, China’s internet and application layer, and US software.

The first phase of the boom rewarded control of scarce intelligence infrastructure.

The next may reward access to intelligence at commodity prices.

Good reading.

The most important AI release of June did not come from Silicon Valley.

It came from Beijing.

GLM-5.2, the latest open-weight model from Z.ai, is forcing investors to confront an uncomfortable possibility. China may not need to build the world’s most capable model to change the economics of artificial intelligence. It may only need to build one that is capable enough, dramatically cheaper and improving faster than the market expects.

That threshold is beginning to look much closer.

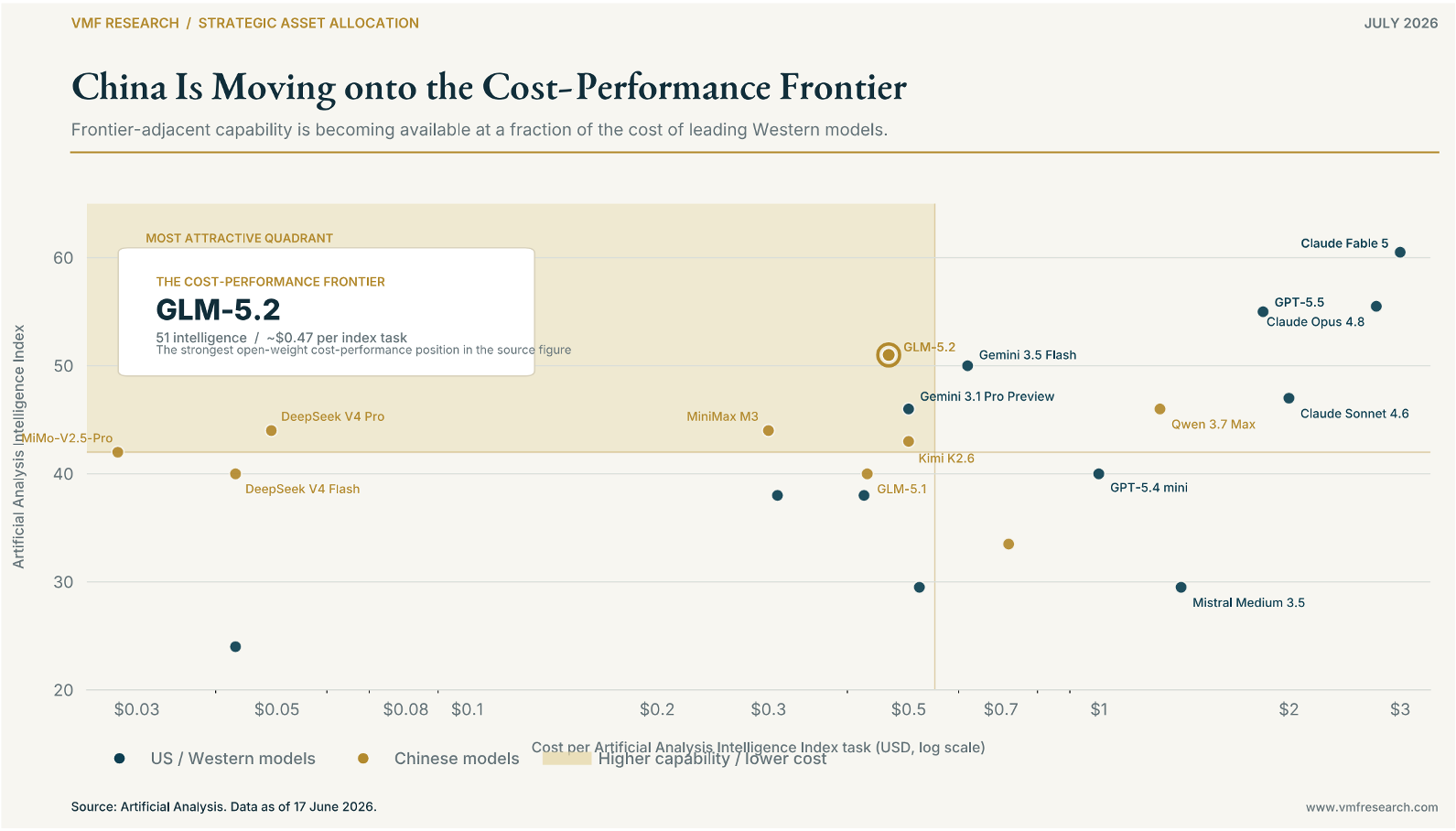

On selected coding and long-horizon knowledge-work benchmarks, GLM-5.2 is competing near the leading proprietary systems. Its weights can be downloaded, adapted and deployed beyond infrastructure controlled by its developer. And its listed price is a fraction of what users pay for the most advanced Western alternatives.

None of this establishes that China has overtaken the United States. The leading American laboratories continue to define the overall frontier, benchmarks measure specific capabilities rather than universal intelligence, and newly released models have not yet been tested across the full range of commercial workloads.

But the direction matters more than the ranking on any particular day.

Chinese laboratories are no longer competing merely by offering yesterday’s intelligence at a discount. They are approaching the frontier while preserving a radically different cost structure.

The chart above reframes the investment question while adding further support to our overweight in Chinese technology equities.

The conventional debate focuses on which country owns the smartest model. That matters for scientific leadership, national security and the small number of tasks requiring the absolute frontier.

It matters less for much of the commercial economy. Most businesses do not need the most intelligent model ever created. They need one capable of completing a particular task reliably, securely and at a price that leaves room for an economic return.

A retailer improving product search does not require the same system as a laboratory conducting advanced scientific research. A company processing documents, translating communications or writing routine code may gain little from paying several times more for the final increment of capability.

UBS estimates that the leading Chinese models now deliver around 90% of the intelligence of the best US systems, compared with approximately 60% in 2023.

Several Chinese models are already competitive in coding, video generation and other multimodal applications. Four of the five highest-ranked video-generation models in the analysis included in our research deck were developed in China.

The exact percentage will change as laboratories release new systems. But the investment conclusion is more durable.

A growing share of economically useful intelligence is no longer confined to the most expensive American models.

And China is offering it at a fraction of the price.

China is not becoming more competitive simply because its models are cheap.

After all, cheap intelligence with poor outcomes has limited value.

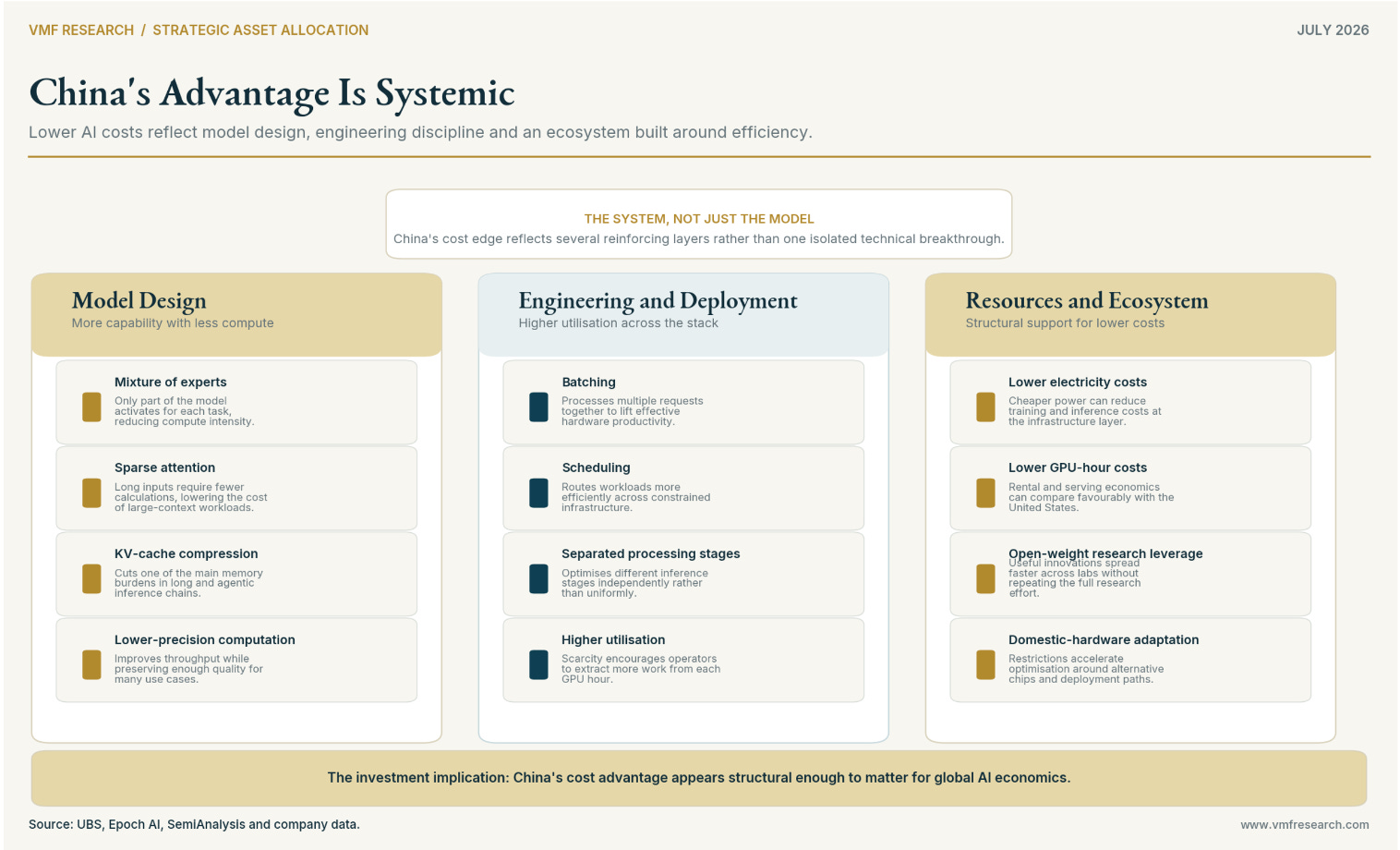

The quality available for each dollar spent is improving at an extraordinary pace. That advantage appears to be the product of an ecosystem rather than one exceptional release.

The US AI industry has developed in an environment of abundant capital, advanced semiconductors and investors willing to fund increasingly expensive attempts to move the frontier. China has faced smaller research budgets, restricted access to the most advanced chips and less capable domestic hardware.

Those constraints have not prevented progress. They have shaped it.

Chinese laboratories appear to concentrate more resources on focused training, post-training optimisation and architectures designed to reduce the amount of compute and memory required for each request. Mixture-of-experts systems activate only part of a model for a particular task. Sparse attention reduces the computational burden of long inputs. Cache compression lowers one of the largest costs in agentic workloads. Lower-precision computation improves throughput, while better batching and scheduling allow more requests to pass through the same infrastructure.

The open-weight ecosystem compounds those advantages.

Once one laboratory validates a useful technique, other developers can adapt it without repeating the full research process independently.

UBS also identifies lower electricity and GPU-hour costs as part of the advantage. Its analysis suggests that comparable infrastructure costs in China can be materially lower than in the United States, reinforcing the gains produced by better model architecture and deployment efficiency.

The spending comparisons are equally striking.

UBS estimates that Zhipu and MiniMax spent approximately $500 million and $300 million respectively on research and development during 2025, only a fraction of the amounts attributed to the largest US frontier laboratories. The same analysis estimates that Chinese frontier-model API prices average below 20% of comparable Western systems, while gross margins for major Chinese model providers may still fall broadly between 20% and 40%.

These comparisons are imperfect. The companies use different accounting methods, infrastructure arrangements and business models. Some may subsidise adoption for strategic reasons, and the disclosure surrounding private AI laboratories remains limited.

Even with those caveats, the signal is difficult to dismiss.

China may be converting each dollar of capital and each unit of compute into more commercially useful intelligence.

The market’s first response has been to declare the model layer a commodity.

That conclusion is directionally correct and analytically incomplete.

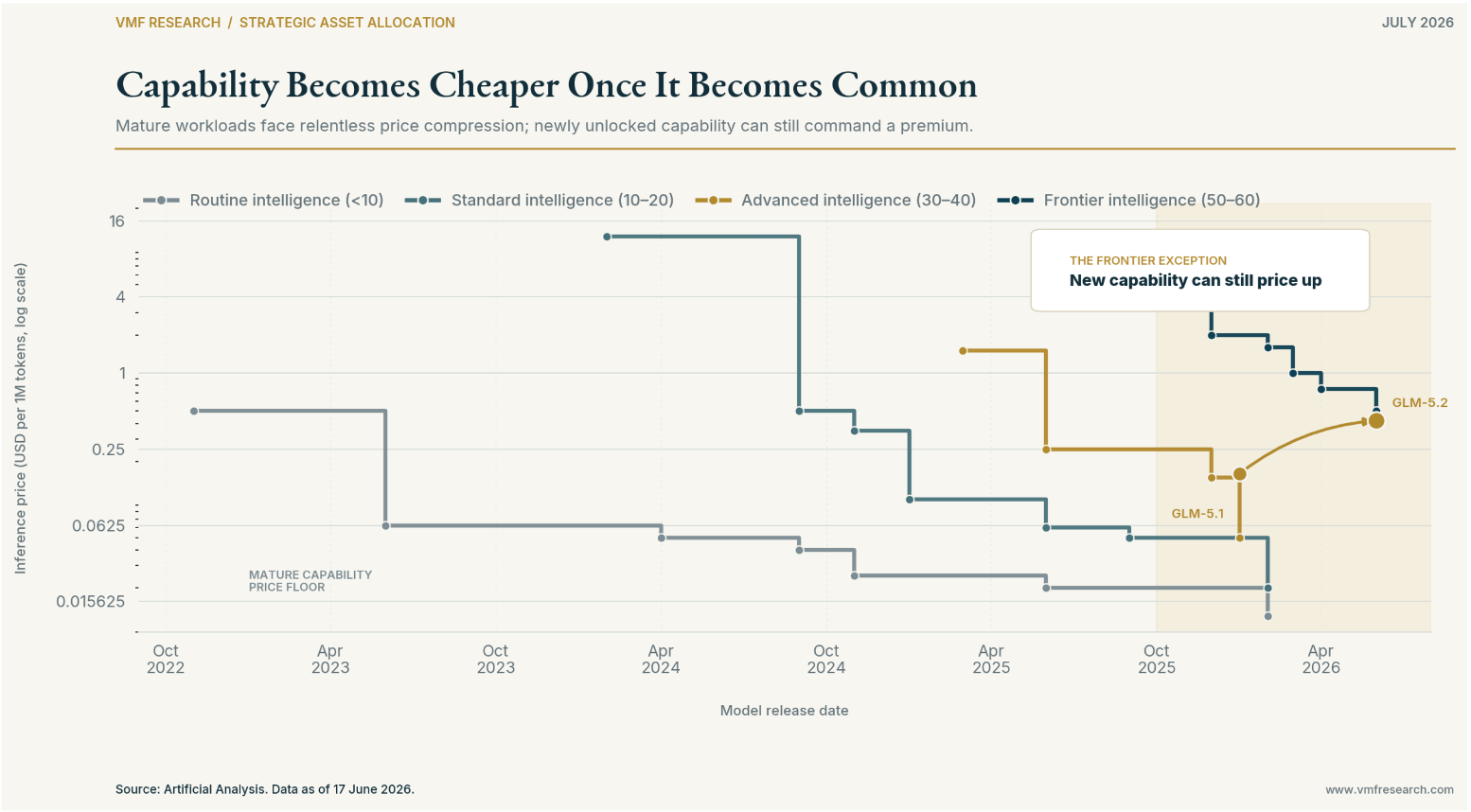

Once several models can perform a routine task adequately, customers compare price, speed and reliability. Basic chat, translation, summarisation, conventional content generation and standard coding assistance should continue to become cheaper.

But intelligence is not one uniform product.

A business may use a low-cost system for thousands of routine interactions while reserving a more capable model for the smaller number of tasks where reliability, reasoning depth or successful completion carries much greater economic value.

Mature capabilities deflate as they become widely available. Newly unlocked capabilities can still command a premium when they reduce errors, complete harder work or replace expensive human effort.

GLM-5.2 illustrates both sides of that market. It remains dramatically cheaper than leading Western frontier models, yet Z.ai appears to have raised its realised pricing relative to the previous GLM generation because the new system can perform more valuable work.

The relevant question is therefore no longer simply how much a token costs.

It is how much it costs to complete the task.

A cheaper model that repeatedly fails can prove expensive. A more capable one that completes a high-value workflow may produce an exceptional return. Providers that stop improving will face commoditization. Those that continue to unlock harder tasks may preserve pricing power even as the cost of established intelligence keeps falling.

This increasingly tiered market also makes it less likely that one model will dominate every workload.

Businesses can route tasks between different providers according to capability, price, latency, reliability, security and privacy. A frontier system may handle advanced research or difficult software architecture. A cheaper model may process documents, write routine code or answer a large volume of customer enquiries. An open-weight system may be deployed internally when sensitive data cannot leave the organisation.

That should favour model-routing platforms and cloud ecosystems capable of matching each task with the most efficient provider. It also allows a Chinese system to capture meaningful demand without becoming the principal model for every customer.

The shift from maximizing token usage towards measuring return on that expenditure should make cost-performance more important.

As enterprises become less impressed by AI consumption itself and more demanding about the productivity it produces, Chinese models appear well positioned for high-volume workloads where the absolute frontier is unnecessary.

That opportunity extends well beyond the United States.

Europe, the Middle East, Latin America and much of Asia lack a local foundation-model ecosystem with comparable breadth. Some governments and businesses will continue to favour American providers because of trust, security or geopolitical alignment. Others will prioritise price, local deployment and the freedom to adapt the model.

China does not need to displace the leading US systems in their home market to become a major global supplier. It can gain substantial share by becoming the preferred cost-performance option across the rest of the world.

The implications stretch across the AI value chain.

Model providers face more competition. Hardware companies face greater scrutiny over how long their scarcity premiums can endure. Data-centre economics become more sensitive to utilisation and rental prices.

At the same time, cheaper intelligence should stimulate far more consumption.

Lower computing costs did not reduce the use of computers. Lower bandwidth costs did not reduce internet traffic. Falling storage prices did not persuade companies to store less data. Each decline in cost made new applications viable.

Artificial intelligence may follow the same path. Efficiency can reduce the resources required for each task while causing the number of tasks to expand much faster.

For semiconductor and infrastructure companies, the crucial question is whether that expansion is sufficient to preserve aggregate demand. For model laboratories, it is whether higher volumes compensate for declining unit prices.

For the applications and companies using AI, however, cheaper intelligence is more clearly an opportunity.

Businesses with customers, proprietary data and specialised workflows acquire a more powerful input at a lower cost. The benefit may appear through faster product development, lower customer-service expenses, better advertising conversion, more efficient logistics or stronger operating margins.

That is how the boom moves downstream.

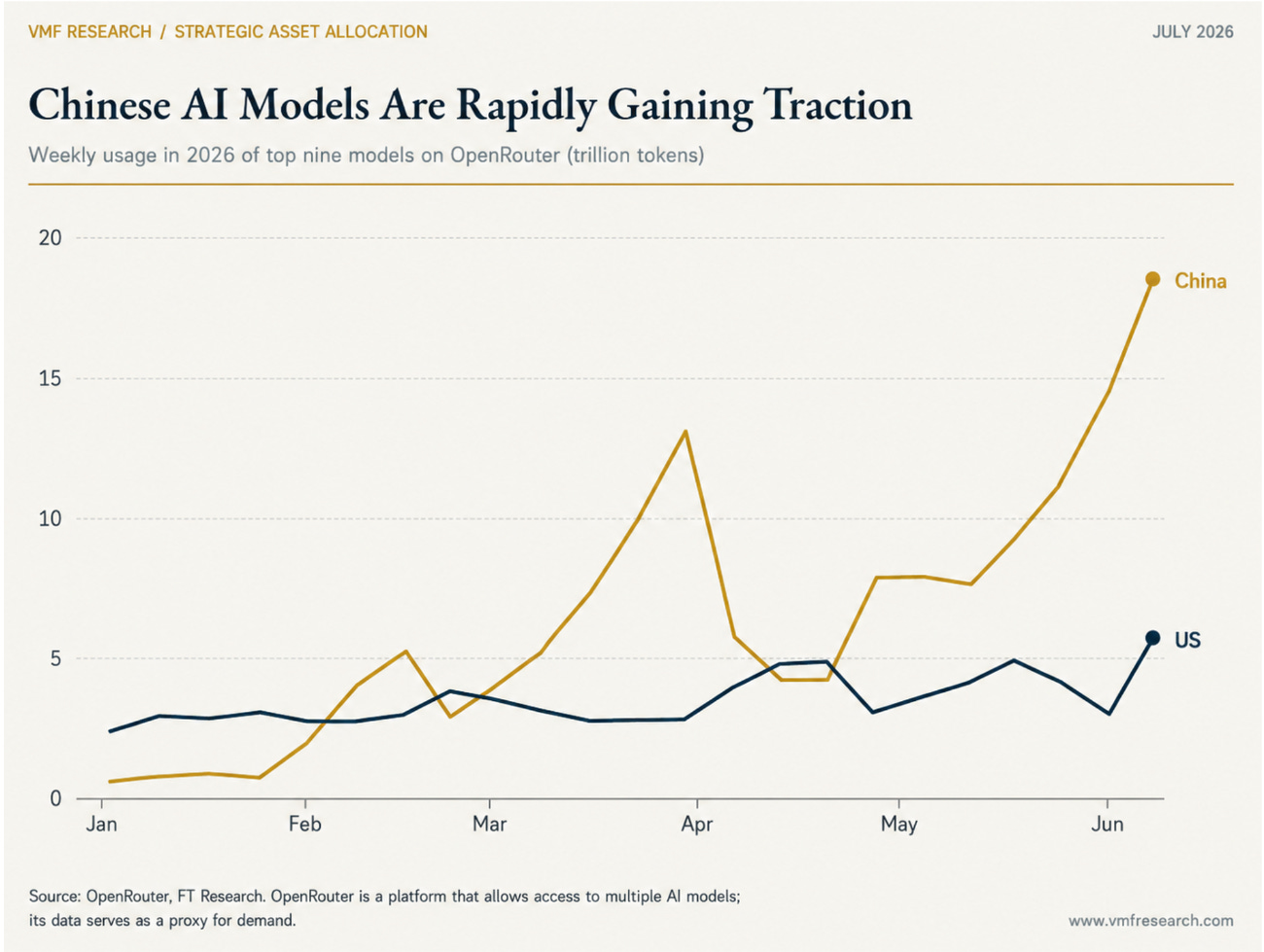

The next question is whether this downstream shift is already visible in usage data.

That is why the chart below matters.

OpenRouter is not the entire AI economy. It does not capture every enterprise contract, every internal model call, or every private deployment inside the largest technology companies. Its data should therefore be treated as a proxy for marginal demand rather than a complete map of AI usage.

But that is precisely why it is useful.

Model-routing platforms sit close to the economic decision. They are where users, developers and applications compare models not in theory, but in practice: which system is good enough, fast enough, reliable enough and cheap enough to complete the task?

On that measure, Chinese models are no longer just improving on paper. They are gaining traction in the market. OpenRouter data compiled by FT Research show weekly usage of leading Chinese models rising sharply through 2026, while comparable usage of leading US models has grown far more modestly.

That does not prove China has won the AI race.

It proves something more relevant for investors.

Beat the old playbook. Get institutional-grade research delivered to your inbox.

China is beginning to compete for the workflow.

That is the bridge from capability to demand. Benchmark convergence tells us that Chinese models are becoming good enough. Price convergence tells us that they are becoming disruptive. Usage growth tells us that some users are already acting on both.

At that point, this stops being a laboratory story.

It becomes an investment story.

And it helps explain why the Model Portfolio has been changing its exposure inside the AI trade. EWY ( EWI 0.00%↑ ) was our first-phase expression. The hidden bottleneck was memory. The market eventually discovered it. The position worked, and we harvested it.

KWEB ( KWEB 0.00%↑ ) is a very different setup.

It is not an obvious winner. It is not crowded.

It does not carry the comfort of recent outperformance. In fact, its chart still reflects years of disappointment, policy risk and macro distrust. But that is also why the asymmetry is more interesting...

While EWY now appears to be losing relative strength after an exceptional advance, KWEB may be starting to stabilize after a long period of underperformance.

That is the kind of rotation we want to study before it becomes obvious.

Our broader China overweight expresses the same view at two levels. MCHI gives the Model Portfolio diversified exposure to Chinese equities. KWEB gives it a more concentrated exposure to the Chinese internet and application layer, where cheaper intelligence can become better advertising, better search, better commerce, better logistics, better customer service and stronger operating leverage.

IGV ( IGV 0.00%↑ ) is the US expression of the same rotation.

Software was treated too simplistically as an AI victim. Some companies will be disrupted. But others may become more valuable as AI lowers development costs, improves functionality, automates workflows and turns static software into intelligent systems.

That is why our application-layer thesis is not only a China thesis. It is a broader view that the next AI winners may be the companies that deploy intelligence well, not only the companies that manufacture or host it.

China, however, remains the higher-convexity expression.

The valuation starting point is lower. The scepticism is higher. The scars from the last cycle are still visible. Policy and geopolitical risks remain real. And the US still commands a much larger pool of private AI investment, an important constraint on any overly simplistic China-bullish narrative.

But the market already knows the US advantage.

It does not yet fully price the China option.

That is why the Model Portfolio maintains its China overweight and its exposure to the application layer through KWEB, MCHI and IGV.

So...

We are not abandoning AI. We are moving further downstream. We are not chasing the most visible winners after the crowd has arrived. We are looking for the next place where cheaper intelligence can change the economics before the market has fully adjusted.

The first AI trade was about scarcity.

The next may be about adoption.

And if usage is now beginning to follow cost and capability, the most interesting opportunities may not be in the companies everyone already recognizes as AI winners. They may be in the places where intelligence is becoming cheap enough to change the economics, but where the market still refuses to pay for it.

That brings us to the next question.

If cheaper intelligence is moving downstream, which sectors combine some of the most expensive workflows in the economy, deep pools of proprietary data, high failure rates from discovery to commercialization, and the greatest economic upside from better decisions?

Healthcare sits near the top of that list.

Biotech may sit at the very centre of it.

That is where we go next.

You might also like reading:

Important Disclosure

This article contains general investment research produced by Vasco Marques de Freitas, CFA, CMT, Founder and CEO of VMF Research, Lda. It reproduces an excerpt from the July 2026 issue of VMF’s Strategic Asset Allocation. The analysis and Tier One Model Portfolio information are stated as of 10 July 2026, 4:00 p.m. Eastern Time.

The publication contains information recommending or suggesting an investment strategy. It is not personalised investment advice and does not consider any reader’s individual objectives, financial circumstances, knowledge, experience or tolerance for risk. The Tier One Model Portfolio is an illustrative research portfolio and does not represent client assets or transactions executed by VMF Research.

The analysis combines thematic, fundamental and market research within a medium- to long-term investment framework. Sources are identified throughout the article. Views are reviewed through VMF Research’s monthly publications and may be updated through weekly or ad hoc publications as evidence and market conditions evolve. Investments in China, emerging markets, technology companies and AI-related financial instruments involve substantial market, regulatory, geopolitical, governance, currency, liquidity and valuation risks. Investors may incur material losses.

Disclosure of interests: as of the research cut-off, neither VMF Research, Lda. nor the author personally held any financial instrument included in the Tier One Model Portfolio. A legal entity controlled by the author held a long position in the KraneShares CSI China Internet ETF (KWEB). This interest may create a potential conflict and should be considered when evaluating the analysis.

Past performance is not indicative of future results.