Michael Burry vs. the AI Capex Frenzy

What His Short Book Is Really Signaling. The quick story, and why it matters.

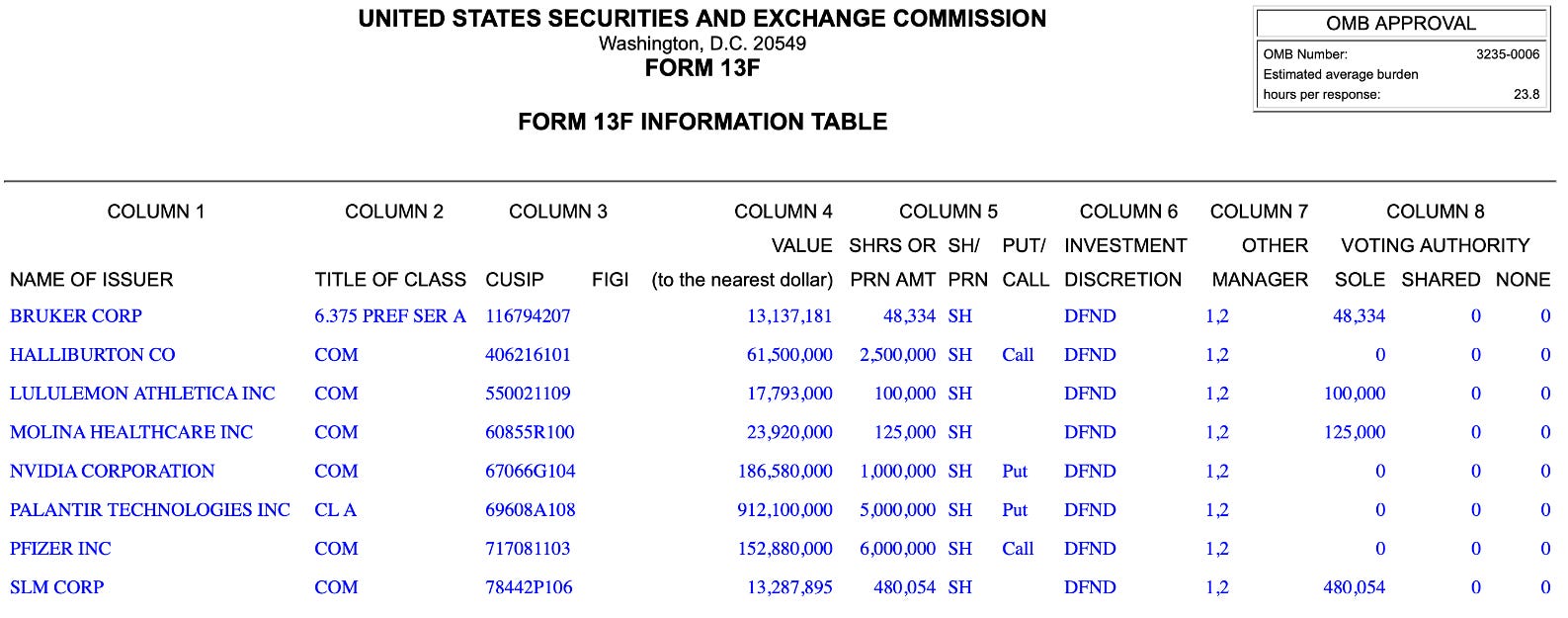

When the investor who turned subprime into a career-defining win plants two big flags on NVIDIA and Palantir, you don’t shrug. You ask: what’s he seeing in the plumbing of the AI trade that others are skipping over? In our November Strategic Asset Allocation (SAA in short), we showed why Burry’s current stance rhymes with our own view on both sides of the book: cautious on the AI infrastructure melt-up, constructive on defensives like healthcare.

Yes, the capex cycle is massive. Hyperscalers are laying concrete, power, and silicon at a breathtaking pace. But here’s the thing: capex is a cost today; revenue arrives later, if it arrives at all.

Our Alpha Tier work has been blunt about the “cash-flow gap” between GPU spending and end-user monetization, and we have already published here on substack a dedicated piece on the matter (read below)

Burry appears to be targeting that gap directly via puts on the emblematic infrastructure leader (NVIDIA) and a marquee applications layer name (Palantir).

What Burry values, and why he’s comfortable being early

Burry’s process is old-school: price, balance sheet, cash flow, time. He built Scion on lockups, low fixed fees, and “ick investing” (look where others refuse to look). The consistency is the point—he makes his living betting against narratives that demand perfection to justify today’s prices. That temperament is unchanged. As we noted, he’s again “targeting a major bubble” and, crucially, he still communicates through filings rather than press tours.

The positions speak for him.

“If you’re going to be a great investor, you have to fit the style to who you are.” Michael Burry

This isn’t about idol worship; it’s about alignment.

Our November Strategic Asset Allocation, explicitly chose not to chase the most crowded AI-infra exposures because the unit economics aren’t proven at scale. In fact, we’ve added a tactical healthcare sleeve—cash-generative, less cycle-sensitive, innovation-rich—to sit alongside our biotech exposure, improving resilience without neutering upside. Burry’s long book (Molina, Pfizer, Bruker) echoes that bias toward durable cash flows.

The AI capex math (and the market’s blind spot)

Markets love a clean story: more GPUs > more AI > more profit.

Reality is messier. Infrastructure spending is being pulled forward at a multi-year clip, while downstream revenue (enterprise adoption, pricing power, margin capture) is still lumpy and uneven. Again, our Alpha Tier deep dive laid out the timing mismatch and why policy, physics, and cash-flow constraints eventually bite.

Burry’s puts are a high-conviction way to express that timing risk; they monetize any wobble in unit volumes, pricing, or supply chain cadence.

For most investors, though, single-name shorts are a bad idea.

You’re fighting sentiment and execution risk. In this edition of Strategic Asset Allocation (SAA), we take a cleaner route: we use the Simplify US Equity Plus Downside Convexity (SPD) ETF to keep equity beta while layering tail protection.

That let us participate in broad market upside, especially if year-end liquidity (QT ending1 + TGA draw) keeps the risk party going—without being the last one out of the door.

How to translate this into a practical playbook

No drama, no heroics. A simple, professional sequence:

Define your core: Keep a diversified base of low-cost ETFs across equities, bonds, and real assets. That’s the Strategic Asset Allocation Tier.. (We publish the full model and benchmark monthly.)

Add a resilient equity sleeve: Tilt toward healthcare and quality cash generators while the market prices perfection into AI infrastructure. Our Strategic Asset Allocation just introduced a healthcare sleeve to pair with biotech—defense without going to cash.

Overlay convex protection: If you’re equity-heavy, consider a pre-positioned hedge like SPD rather than single-name puts. It’s cleaner, repeatable, and it respects your sleep.

Respect liquidity regimes: The Fed’s QT end + Treasury’s TGA draw can keep the tape buoyant into year-end, but don’t confuse liquidity tailwinds with infinite fundamental runway. Keep the hedge on; size the hot-story exposure modestly.

Steal Burry’s temperament: Write more, trade less. Measure first, decide second. If the smartest room is ignoring the math, step aside. (He did it in 2007—and he’s sticking to that script now.)

Why this is showing up in my book (and how you can follow along)

In our November SAA, we’ve already reflected this view: no chase on AI-infra at nosebleed multiples, a fresh healthcare tilt, and a standing layer of convexity. The goal isn’t to “call tops.” It’s to keep compounding when narratives wobble.

Burry’s latest 13F just adds another datapoint that the risk/reward around the AI capex boom is skewed. We’re in good company—and we’re prepared.

Bottom line (and a fast next step)

You don’t need to mirror Burry to benefit from the signal. Keep your core, add resilience where cash flows are real, and install a modest hedge so you’re not negotiating with the market at 3 a.m.

And then the news broke…

As we wrapped this issue, news broke: Michael Burry is stepping away from managing outside money again. Through an SEC filing, Scion Asset Management deregistered—so no more 13Fs, no public look into his book, and likely a family-office setup managing only his own capital.

In a note, Burry said his “estimation of value in securities is not now, and has not been for some time, in sync with the markets.” Translation: his lens hasn’t been rewarded lately. Some positions in his last 13F—especially high-profile AI shorts—have struggled as the AI-leadership trade keeps stretching. Maybe that’s the driver. Or maybe he simply doesn’t want to field quarterly questions while markets ignore valuation. Either way, a prominent skeptic just chose to stop playing in a structure that forces trade disclosure.

From a contrarian angle: is this capitulation? Is Burry the last big AI bear to quit managing external capital? History will decide. What we can say: nothing here invalidates our arguments; if anything, it reinforces them.

Turning to our Model Portfolio (gated), this was a risk-off week. After a powerful run, some cooling was due. The pullback hit our newer Solana and Ethereum positions hardest. Unpleasant near term, yes—but we view it as more likely a bear trap than the start of a lasting bear market in crypto or risk assets.

Why?

Liquidity is still the key. The Fed is set to halt QT in coming weeks. The government shutdown is resolving, opening the door to a meaningful TGA drawdown. Together, these point to a material improvement in dollar liquidity into year-end. In that backdrop, sharp corrections in high-beta assets often prove shakeouts, not trend changes.

This is the juncture where staying close to the work matters. It’s a moment to stay engaged, not drift.

If you want the exact tickers, weights, and our month-by-month changes, that’s what we publish for members.

So if you’re ready to see the full SAA model, the healthcare sleeve, and our current hedging weights? Join us at VMF Research (Strategic Asset Allocation tier starts at €300/year):

*QT Ending: When the Fed ends Quantitative Tightening (QT), it stops shrinking its balance sheet and no longer lets bonds roll off without reinvestment, which means it stops draining bank reserves from the system and becomes neutral or slightly supportive for liquidity. At the same time, when the U.S. Treasury draws down the TGA after a shutdown, it is effectively spending more than it is issuing in net new debt for a period, so cash flows out of its account at the Fed and into the private sector as payments to households, companies and investors. That raises bank reserves and puts more cash in circulation. In combination, an end to QT and a TGA drawdown both push liquidity into markets instead of pulling it out.