Liquidity Bites Back

Powell cools December cut odds, QT nears the finish, and a fatter TGA tightens screens. Our base case still points to a year end turn as we trim an AI Korea winner.

Today’s Weekly Update (Tier One) dropped on November 8th for subscribers. Head out to VMF research and subscribe to get it first.

Risk-off is taking hold across Wall Street and global markets. You can feel it in credit, in factor spreads, and in the way rallies are failing faster. This isn’t a blip... it’s a proper de-risking wave.

The culprits?

Two familiar forces we’ve been tracking for a long time. No surprises here... just the same drivers turning the screws again. First, Liquidity. Last week, Chair Powell reminded investors that a December rate cut isn’t a done deal (as the odds in the tableabove make plain). At the same time, he flagged the end of QT in early December (exactly what we forecasted in the last issue of Alpha Tier).

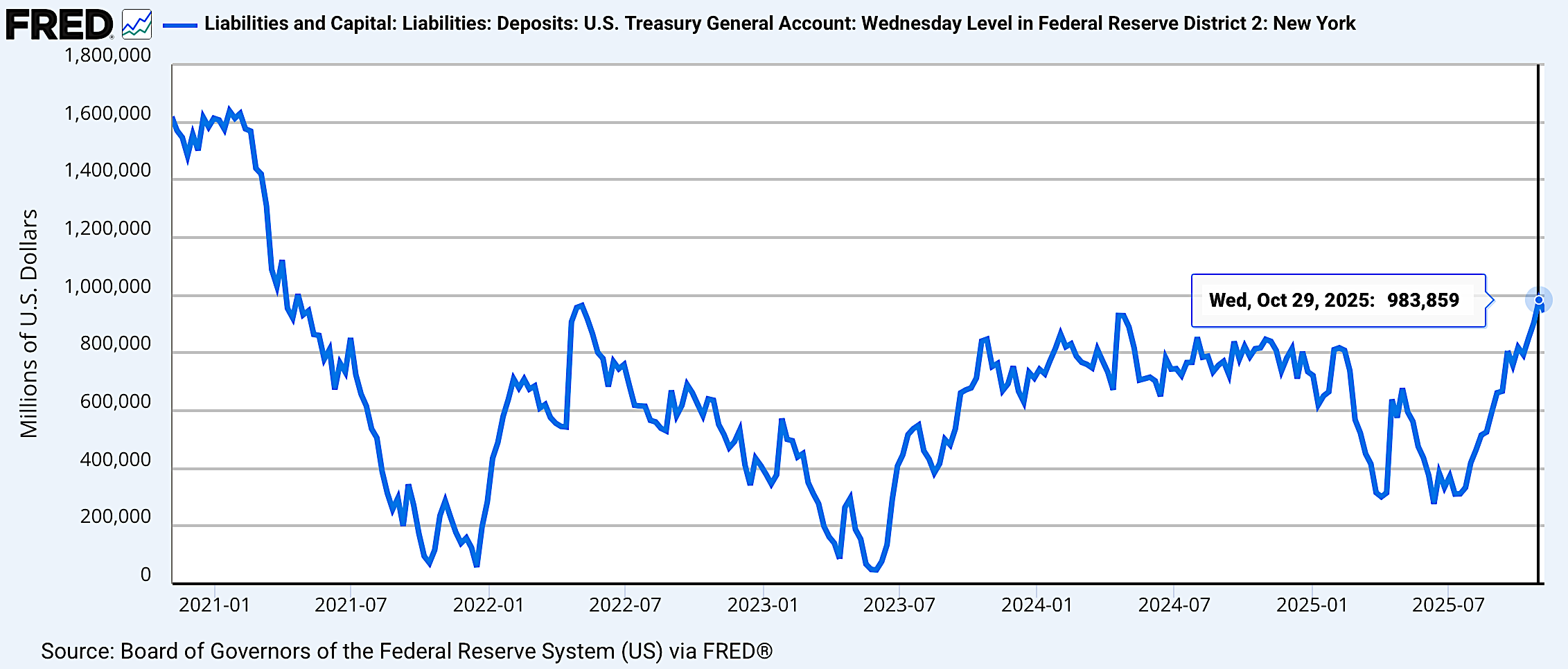

Layered on top, the ongoing U.S. shutdown is tightening the liquidity backdrop. The government keeps collecting revenues while delaying a chunk of spending, pushing the Treasury General Account higher. Remember: the TGA is a Fed liability. When it rises, market liquidity thins. That’s the mechanical drain you’re feeling on screens.

Our base case: both headwinds resolve favourably in the short term. QT’s end and a shutdown resolution should refill the liquidity pool just as positioning gets cleaner. When liquidity turns, it tends to turn abruptly... setting the stage for a year-end rally!

The second risk driver is the sustainability of the AI capex boom (some call it a boom, others a bubble).

We dissected this in the last Alpha Tier, and it will be the main event in next week’s monthly issue of VMF’s Strategic Asset Allocation.

Stay tuned!

The AI Capex Boom: Amazing for GDP, Dangerous for Investors (Ask 1929, 2000)

We’re on track for ~$400B of AI capex in 2025. The 2000 telecom peak was $113B… about $213B in today’s money. Meanwhile, consumer AI spend may at best reach ~$25B this year. The gap is enormous and requires a lot of heavy lifting to close, especially when you recognize that, unlike prior transformational buildouts, today’s GPU-heavy capex carries shorte…

We’ll separate signal from noise and map the second-order effects for our Model Portfolio.

One housekeeping note on positioning: our AI related South Korea trade briefly touched our 100% return threshold this week. We’re following our risk management protocol: let’s close half the position here, locking in a 71.5% total return on that tranche, and let the remainder run.

Good investing!

If you want the full analyst pack, charts, positioning, model portfolio changes, and the signals I’m using, subscribe to one of our tiers at VMF Research.

We publish independent, evidence-based work.

No hype, just process. (And yes, we eat our own cooking.)